{kind=link}

In today’s ever-fluctuating economic landscape, the importance of saving cannot be overstated. Whether you’re building an emergency fund, saving for a significant purchase, or simply ensuring a stable financial future, the role of a savings account is pivotal. But why is a savings account considered a cornerstone of personal finance? This comprehensive guide aims to unpack the essentials of savings accounts, offering you the insights needed to understand how they can play a crucial role in your financial strategy.

What Is a Savings Account?

A savings account is a type of bank account where you can deposit money you don’t plan to spend immediately but want to keep safe and accessible while earning interest. Here are the key features of a savings account:

Interest Earnings: Savings accounts pay interest on the money you deposit. The interest rate is usually modest but incentivizes saving money instead of spending it.

- Safety: Money in a savings account is safe because it is typically insured by a government agency such as the Federal Deposit Insurance Corporation (FDIC) in the United States or a similar institution in other countries. If the bank fails, this insurance protects your money up to a specific limit.

- Liquidity: Funds in a savings account are relatively liquid, meaning you can quickly and easily access your money when needed. However, there may be limits on the number of withdrawals you can make each month.

- Low Risk: Savings accounts are considered low-risk compared to other forms of investment, like stocks or bonds because their return is stable and does not fluctuate with market conditions.

- Minimal or No Fees: Many savings accounts have low or no monthly fees, especially if you maintain a minimum balance or link your account with other banking services.

- Convenience: Savings accounts can be linked to other bank accounts, such as checking accounts, making it easy to transfer money manually or automatically between accounts.

Savings accounts are ideal for storing emergency funds or saving for short-term goals because they balance earning interest with high security and easy access to funds.

Choosing the Right Savings Account

Balancing interest rates with low fees is crucial when choosing the correct savings account. L is necessary for accounts that offer high-yield returns with minimal or no maintenance fee. Check for any minimum balance requirements that might limit your ability to earn interest. Convenience is also key, so consider whether the account can be easily managed online or via a mobile app and if there are sufficient deposit and withdrawal options. Finally, ensure your account is FDIC or NCUA insured to protect your funds up to the allowable limits. Evaluating these factors will help you find a savings account that maximizes your earnings while fitting seamlessly into your financial lifestyle.

Explore Alternatives to Savings Accounts

Exploring alternatives to traditional savings accounts can be wise if you’re looking for different ways to grow your savings or need more flexibility or higher returns on your investments. Here are some viable alternatives:

- High-Yield Checking Accounts: Some checking accounts offer interest rates comparable to or even higher than savings accounts, often without the typical withdrawal restrictions. These accounts might require specific actions, like a minimum number of debit card transactions per month.

- Money Market Accounts (MMAs): These accounts often provide higher interest rates than traditional savings accounts, with added flexibility to write checks or debit cards. However, they usually require higher minimum balances to maintain and earn the advertised interest rate.

- Certificates of Deposit (CDs): CDs offer fixed interest rates for a specified term, ranging from a few months to several years. The rate is usually higher than in savings accounts, but the money must stay in the CD for the term to avoid early withdrawal penalties.

- Treasury Securities: Another safe alternative is to invest in U.S. Treasury securities, such as bills, notes, and bonds. These government-backed securities offer fixed interest rates and are considered virtually risk-free.

- Bond funds invest in various bonds issued by corporations, municipalities, and governments. They can offer higher returns than savings accounts, but depending on the types of bonds in the fund’s portfolio, they come with higher risks.

- Peer-to-peer lending Platforms allow you to lend money directly to individuals or small businesses online, bypassing traditional banking systems. Returns can be higher than savings accounts, but so is the risk, as these loans are not insured.

- Real Estate Investment Trusts (REITs): For those interested in real estate, REITs offer a way to invest in property without having to buy, manage, or finance properties directly. REITs typically distribute a high percentage of their profits as dividends, which can provide a steady income stream.

- Robo-Advisors: These automated investing services manage your investments using algorithms. With low minimum investment requirements and low fees, robo-advisors can provide a hands-off way to grow your savings based on your risk tolerance and goals.

- Online Investment Platforms: These platforms offer various investment options, from stocks and bonds to ETFs and mutual funds, often with lower fees than traditional brokerages. They provide the tools and resources to manage your investments actively or passively.

Each of these alternatives has its own set of benefits and risks, and the best choice depends on your financial goals, risk tolerance, and liquidity needs. It’s essential to research each option thoroughly or consult a financial advisor to make an informed decision that aligns with your economic strategy.

Is a Savings Account Right for You?

Deciding whether a savings account is the right choice depends on several factors, including your financial goals, need for liquidity, risk tolerance, and how you plan to use the account. Here are some considerations to help determine if a savings account fits your financial situation:

Financial Goals

A savings account is a good option if you want to keep funds safe while earning some interest. It’s beneficial for short-term savings goals, such as saving for a vacation, an emergency fund, or a significant purchase. The accessibility and safety of a savings account make it ideal for these purposes.

Need for Liquidity

Savings accounts offer high liquidity, meaning you can easily and quickly access your money. This makes them suitable if you want immediate access to your funds in case of emergencies or unexpected expenses.

Risk Tolerance

Savings accounts are among the safest investment options because they are typically insured by institutions like the FDIC or NCUA in the U.S., which protects your money up to certain limits. A savings account is appropriate if you have a low-risk tolerance and prefer a guaranteed return without the possibility of losing your principal.

Interest Rates

While savings accounts are safe and liquid, they generally offer lower interest rates than other investment vehicles like stocks, bonds, or mutual funds. If you want to grow your wealth over the long term or seek higher returns, you might consider other investment options that align better with these goals.

Alternative Options

If you’re dissatisfied with the interest rates provided by traditional savings accounts, consider alternatives. High-yield savings accounts, money market accounts, or certificates of deposit might offer better rates. Each comes with its own set of rules regarding access to funds and interest rates, so they might still meet your needs for safety and slightly higher returns.

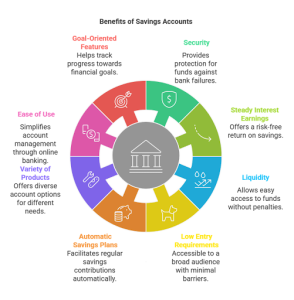

Advantages of Savings Accounts

- Security: Savings accounts offer a high level of protection for your money. Deposits in savings accounts are insured by government agencies like the FDIC in the U.S., protecting funds up to $250,000, which provides peace of mind to savers against bank failures.

- Steady Interest Earnings: Although not the highest yielding, savings accounts provide a constant, risk-free return through interest on your balance. This can help grow your funds slowly without the risk of other investment vehicles like stocks or mutual funds.

- Liquidity: One key advantage of savings accounts is their liquidity. You can access your funds almost anytime without penalties, which is not always true with investments like fixed deposits or retirement accounts.

- Low Entry Requirements: Most savings accounts have very low or no minimum balance requirements, making them accessible to a broader audience. This inclusivity allows individuals from various economic backgrounds to begin saving.

- Automatic Savings Plans: Many banks offer the option to set up automatic savings plans. This feature helps users establish a habit of saving without making manual transfers, thus facilitating regular savings contributions.

- Variety of Products: Financial institutions often provide various savings account products tailored to different needs, including high-interest accounts, accounts for children, and accounts integrated with budgeting tools, allowing customers to choose one best suited to their financial goals.

- Ease of Use: With the advent of online banking, managing a savings account has become more straightforward. Users can easily monitor their balances, transfer funds, and pay bills online, enhancing the user experience.

- Goal-Oriented Features: Some savings accounts offer sub-accounts or savings goals that help customers track their progress toward specific financial goals, such as saving for a holiday, an education fund, or a new home.

- Promotes Financial Discipline: Regularly contributing to a savings account can foster financial discipline, a crucial aspect of effective financial planning and budget management.

- Educational Benefits: Banks often provide financial education resources that help account holders understand better how to manage their money effectively, plan for the future, and achieve their financial goals.

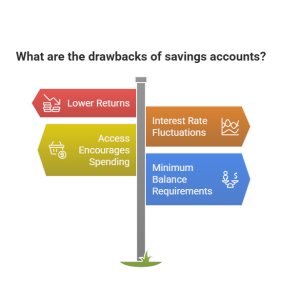

Disadvantages of Savings Accounts

- Lower Returns: Compared to other investment vehicles, savings accounts typically offer lower interest rates. These rates might not always keep pace with inflation, potentially eroding the purchasing power of savings over time.

- Interest Rate Fluctuations: The interest rates on savings accounts are subject to change based on economic policies and market conditions, which can affect the amount of interest earned.

- Access Encourages Spending: While convenient, easy access to funds can also be a downside, as it may encourage impulsive spending, making it harder to save for long-term goals.

- Minimum Balance Requirements: Some savings accounts require a minimum balance to avoid fees or to earn a higher interest rate, which could be a hurdle for those unable to maintain such balances.

- Opportunity Cost: Money in savings accounts could be used in other investments with potentially higher returns, leading to an opportunity cost.

- Fees and Charges: Certain savings accounts charge monthly maintenance fees, transaction fees, or penalties for not maintaining a minimum balance, which can reduce earnings.

- Overdraft Risks: Some savings accounts linked to checking accounts might have overdraft facilities that, if not carefully managed, could lead to fees and penalties.

- Inflation Risk: In a high-inflation environment, the modest interest earned on savings accounts might not preserve the actual value of money, leading to a decrease in purchasing power.

- Regulatory Restrictions: The number of withdrawals or transfers you can make each month is restricted, limiting flexibility.

- Lack of Investment Growth: While savings accounts are excellent for short-term savings and emergencies, they do not provide the growth needed for long-term financial goals like retirement.

Understanding these advantages and disadvantages can help you decide how best to use savings accounts in your financial strategy, balancing safety and accessibility against the need for higher returns and investment growth. A savings account promotes disciplined saving habits and helps develop a strategic financial approach. Additionally, many institutions offer workshops and seminars to help customers navigate complex financial landscapes, empowering them to build and manage their wealth effectively. These six benefits underscore the importance of savings accounts in personal finance, showcasing their role in fostering security, growth, and financial savvy.

Conclusion

Understanding the different facets of savings accounts—from their essential function to more complex features—is crucial in personal finance. We encourage you to assess your financial goals and compare different savings accounts to find the one that best suits your needs. Take the next step towards financial security by exploring your options and saving today.