{kind=link}

How much money should I have in my checking account?

The money you should keep in your checking account typically depends on your monthly expenses and personal financial habits. As a general rule of thumb, it’s advisable to maintain enough funds to cover one to two months’ worth of expenses. This ensures you can comfortably handle regular payments, such as bills, groceries, and unexpected costs, without risking an overdraft. Additionally, considering the frequency of your income and potential unforeseen expenses can help you determine a more personalized buffer. Keeping this amount in your checking account allows for smooth financial management while reducing the risk of running low on funds.

Understanding the Basics of Cash Management

What are Cash Reserves?

Cash reserves are the funds you have readily available in your checking and savings accounts. These are your go-to funds for daily transactions and unexpected needs.

Why Optimize Cash Reserves?

Optimizing your cash reserves is essential for two reasons: ensuring you have enough liquid cash for immediate needs and investing excess to outpace inflation. It’s crucial to avoid the pitfall of leaving too much money in low-interest accounts, which does little for your financial growth.

The Role of Checking Accounts

Checking accounts should be your financial hub for everyday transactions and bill payments. They offer convenience but typically little to no interest earnings, making them ideal for short-term needs rather than long-term growth.

The Role of Savings Accounts

In contrast, savings accounts are your financial cushions for short-term goals and emergencies. They generally offer better interest rates than checking accounts, making them suitable for growing your reserves while keeping them accessible.

| Account Type | Recommended Balance | Purpose |

| Checking Account | 1-2 months’ expenses | Daily transactions, bill payments |

| Savings Account | 3-6 months’ months(emergency fund) | Emergency buffer, short-term savings goals |

| Investments | Excess funds beyond emergency and savings | Long-term growth, retirement planning |

How Much Should You Keep in Your Savings Account?

The Emergency Fund

An emergency fund is crucial for covering unexpected financial setbacks, and based on income stability and lifestyle, the guideline is typically 3-6 months of living expenses.

Savings Goals

Consider your short-term goals, such as saving for a down payment or a vacation. Each goal should influence how much you allocate to savings.

High-Yield Savings Accounts

To maximize your savings, high-yield savings accounts are a preferable alternative to standard ones. They offer higher interest rates and better growth potential.

When managing your finances, it’s essential to consider several key aspects: how much money you should keep in your checking account should generally be enough to cover a month or two of expenses for easy access and payment flexibility. Regarding how much you should keep in savings, it’s wise to have about three to six months of living expenses in case of emergencies. The maximum amount you should keep in a savings account depends on your financial goals and the return rates of potential investments. For the portion of your funds that is more growth-oriented, determining what percentage from your checking account should be invested can depend on your risk tolerance and long-term financial objectives. Still, a balanced approach can help ensure both security and growth.

How Much Money Should You Keep in Your Checking Account?

The Core Question

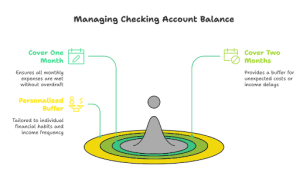

Determining the right amount of money to keep in your checking account is a common financial concern. The key is to strike a balance—having enough to manage your daily needs without holding excessive funds that could otherwise be growing elsewhere.

Rule of Thumb

A practical guideline is to maintain one to two months’ worth of expenses in your checking account. This ensures you have sufficient funds to cover your regular outgoings as well as any unexpected costs that may arise.

Calculating Your Monthly Expenses

Track both your fixed and variable expenses to gauge how much money you need in your checking account. Analyzing how much you spend each month will clarify the amount you need readily available. This calculation helps manage your monthly budget and secures you against being caught off-guard by unforeseen expenses.

Specific Considerations

When deciding how much to keep in your checking account, consider the frequency of your income and expenses. For instance, if you’re paiyou’re frequently, you might manage with a smaller buffer. Additionally, tailor your account balance to include a cushion for unexpected costs, ensuring you’re ready for any financial surprises. Budgeting apps or spreadsheets can be extremely helpful in tracking and adjusting your expenditures to suit your financial lifestyle and needs.

Checking vs. Savings: Which Should Have More?

Comparing Account Balances

When managing your financial portfolio, it’s generally advisable that your savings hold a larger balance than your checking account. This approach ensures that your funds are secure and accruing more substantial growth in accounts with higher interest rates or investment opportunities.

Liquidity vs. Growth

Navigating the balance between liquidity and growth is a fundamental aspect of personal finance. Funds in your checking account are highly liquid, meaning they can be accessed quickly and without penalties. However, this liquidity comes at the cost of lower growth potential. Conversely, money in savings accounts, while slightly less accessible, typically earns a higher return, making it a wiser choice for funds that you do not need immediate access to.

Personal Circumstances

The ideal allocation between your checking and savings accounts will vary based on your unique financial situation. Factors such as your spending habits, financial goals, and risk tolerance are critical in determining how to distribute your funds. As these factors change, so should your approach to managing your account balances. Regularly revisiting and adjusting your financial strategy can help ensure that it aligns with your current needs and future ambitions, allowing you to optimize your financial health effectively.

When and How to Start Investing

Investing from Bank Accounts

When managing your finances, determining the right portion of your bank accounts to invest is vital for long-term wealth building. This decision should closely align with your financial goals and risk tolerance to ensure that your investment strategy complements your overall financial plan.

The Importance of Investing

Investing is crucial in accumulating wealth and ensuring a financially stable future. Wise investment can outpace inflation and grow assets over time, which is essential for long-term financial security and achieving one’s financial aspirations.

Determining Your Investment Percentage

To decide how much of your savings to invest, consider your financial goals and the level of risk you are comfortable taking. This will help guide the proportion of your liquid savings that should be transitioned into investments. Whether saving your retirement, making a significant purchase, or building generational wealth, allocating funds between savings and investments can significantly impact your financial success.

Understanding Risk Tolerance

Your risk tolerance is a key determinant in shaping your investment strategy. Investment decisions should reflect how comfortable you are with the possibility of losing money in exchange for the potential of higher returns. Higher-risk investments, while offering greater return potential, require caution and an understanding of the market dynamics.

Basic Investment Options

For those new to investing, it’s important to start with a basic understanding of the different types of investment vehicles available, such as stocks, bonds, and mutual funds. Each option comes with varying levels of risk and potential return. Consulting with a financial advisor can be invaluable for personalized investment advice that fits your specific financial situation and goals. They can provide tailored advice and strategies, helping you to navigate complex investment decisions and optimize your financial portfolio for sustained growth.

Practical Tips and Best Practices

Regularly Review Your Finances

Regularly review and adjust your finances to optimize your cash management strategy effectively.

Utilize Online Tools and Calculators

Use budgeting apps and online calculators to refine your saving and investment strategies and ensure you meet your financial objectives.

Consider Tax Implications

Be aware of the tax implications of your investments, which can affect your overall financial planning.

Seek Professional Advice

Consider consulting with a financial advisor who can provide expertise tailored to your specific circumstances for personalized guidance.

Conclusion

Understanding your finances and finding the right balance between liquidity and growth is essential. Take steps today to optimize your cash reserves and empower yourself with the knowledge you need to achieve financial independence. Start this journey towards optimizing your cash management for a more secure and prosperous future.