{kind=link}

Imagine this: You’re finally ready to renovate your home, buy a new car, or cover an unexpected expense, but you don’t have enough savings. You start researching financing options and quickly find yourself confused between personal loans and lines of credit. Which one should you choose?

If you’re in the United States, you’re not alone in facing this dilemma. Many people struggle to understand the key differences between these two financial products and how they impact their borrowing experience. The purpose of this guide is to break down the differences between a personal loan vs. line of credit, helping you determine which option suits your specific needs best.

Understanding Personal Loans

What is a Personal Loan?

A personal loan or personal line of credit is a fixed amount of money borrowed from a lender, typically used for a specific purpose such as consolidating debt, covering medical expenses, or funding home improvements. When comparing a personal loan vs. personal line of credit, it’s important to note that personal loans come with fixed interest rates and a set repayment schedule, meaning you’ll pay the same amount every month for a predetermined term (e.g., 2, 5, or 7 years).

If you’re wondering, Is a personal loan a good idea, the answer depends on your financial situation and repayment ability. Working with direct personal loan lenders can help streamline the borrowing process and provide quick access to funds. Additionally, some lenders offer pre-approved personal loans, allowing borrowers to secure financing faster based on their creditworthiness.

For those who may not qualify for traditional bank loans, soft credit check loans can be an alternative, offering flexibility without impacting your credit score during the initial application process. A private lender loan can also be a viable option, often providing more lenient eligibility criteria and personalized lending solutions.

Since personal loans provide a lump sum, they are ideal for one-time expenses where you know exactly how much money you need. Understanding these options will help you make an informed financial decision based on your specific needs.

How Personal Loans Work

- The lenders evaluate your application based on your credit score, income, etc. Credit persons with adequate scores are usually granted the loan.

- If the loan is approved, you get a single lump-sum payment into your bank account.

- Upon repayment, you will make fixed monthly payments where both principal and interest will be discharged until it is paid off.

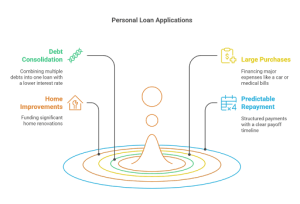

When to Use a Personal Loan

When to Use a Personal Loan

- Debt consolidation: Combine multiple high-interest debts into one manageable loan with a lower interest rate.

- Large purchases: Ideal for financing major expenses like a car or medical bills.

- Home improvements: Best for single, significant renovations (e.g., installing a new roof or remodeling a kitchen).

- Predictable repayment: Perfect if you prefer structured payments and a clear payoff timeline.

Personal loans have their perks

Personal loans have their perks

✔ It makes budgeting predictable regarding monthly payments.

✔ Fixed interest implies no surprises along the way.

✔ With a fixed repayment structure, you are sure to complete your repayment on time.

Cons of Personal Loans

✘ Less flexibility since you receive a lump sum and cannot access additional funds.

✘ Not ideal for ongoing expenses or uncertain costs.

Best Personal Loan Providers in the U.S.

SoFi

- Overview: SoFi offers personal loans with competitive interest rates and no fees. They provide loan amounts ranging from $5,000 to $100,000 with flexible repayment terms of up to 84 months.

- Key Features:

- No origination fees or prepayment penalties.

- Unemployment protection program.

- Access to member benefits, including career coaching and financial planning.

- Website: SoFi Personal Loans

LightStream

- Overview: On this occasion, let me inform you, the same goes here for Lightstream that is a division of Trui Life Bank, a secure and best-layered bank for good and excellent credit borrowers. You can borrow LightStream amounts anywhere between $5,000 to $100,000 for home improvement or debt consolidation.

- Facilitate Features:

- No charges, no charges for prepayment.

- Rate Beat Program: Beat a competitor’s rate by 0.10%.

- Two-day funding.

- Website: LightStream Personal Loans

LendingClub

- Overview: Lending Club is peer-to-peer and gives a host of personal loans for debt consolidation and other major purchases. Loan amounts available range from $1,000 to $40,000.

- Facilitate Features:

- Apply with a co-borrower.

- Money is paid directly to the creditors for debt consolidation loans.

- Flexible repayment plans.

- Website: LendingClub Personal Loans

Upgrade

- Overview: Upgrade personal loans serve fair to good credit borrowers. Loan amounts range from $1,000 to $50,000 with repayments scheduled in a range of 24 to 84 months.

- Features:

- Fixed-rate and predictable payments.

- Check rates without affecting credit score.

- Provides tools for credit health monitoring.

- Website: Upgrade Personal Loans

Upstart

- Overview: Upstart is responsible for taking into consideration education and employment history. This is in combination with assessing a loan application with several artificial intelligence applications. Loan amounts from $1,000 to $50,000.

- Features:

- Accepts limited credit history applicants.

- Fast funding takes as quick as tomorrow.

- No prepayment penalties.

- Website: Upstart Personal Loans

Best Egg

- Overview: Best Egg offers personal loans primarily for debt consolidation and major purchases. Loan amounts range from $2,000 to $50,000, with fixed APRs.

- Key Features:

- Quick online application process.

- Funds are available in as little as one business day.

- Offers secured loan options.

- Website: Best Egg Personal Loans

Discover Personal Loans

- Overview: Discover offers personal loans with flexible repayment terms and no origination fees. Loan amounts range from $2,500 to $35,000.

- Key Features:

- No fees as long as you pay on time.

- 30-day money-back guarantee if you change your mind.

- Direct payment to creditors for debt consolidation.

- Website: Discover Personal Loans

Company Overview

- SoFi: No fees, competitive interest rates, or unemployment protection.

- LightStream: Low interest rates, no fees, and same-day funding.

- LendingClub offers Peer-to-peer lending, a co-borrower option, and direct payments to creditors.

- Upgrade tailored for fair to good credit borrowers with credit monitoring tools.

- Upstart AI-driven approvals considering education and job history.

- Best Egg Fast approval, low rates for high credit scores, and secured loan options.

- Discover No fees, flexible terms, and a 30-day money-back guarantee.

Understanding Lines of Credit

What is a Line of Credit?

A line of credit (LOC) is a flexible borrowing option that allows you to withdraw money as needed, up to a predetermined credit limit. Unlike a personal loan, an LOC is revolving, meaning you can borrow, repay, and borrow again within the credit limit.

You only pay interest on the amount you withdraw, making it a convenient choice for unpredictable expenses.

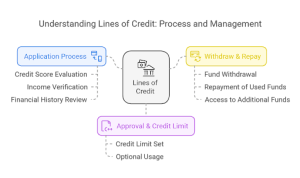

How Lines of Credit Work

- Application Process: Similar to a personal loan, lenders review your credit score, income, and financial history.

- Approval & Credit Limit: If approved, you receive a credit limit (e.g., $10,000), but you don’t have to use it all at once.

- Withdraw & Repay: Borrow funds as needed, repay what you use, and access more funds as necessary.

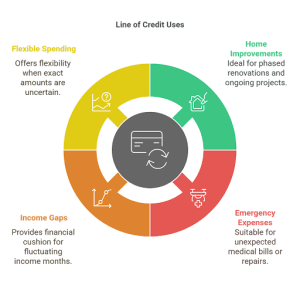

When to Use a Line of Credit

When to Use a Line of Credit

- Home improvements: Ideal for ongoing or phased renovations (e.g., remodeling one room at a time).

- Emergency expenses: Perfect for unexpected medical bills or car repairs.

- Business or freelance income gaps: If your income fluctuates, a line of credit provides a cushion for slow months.

- Flexible spending: Great when you don’t know exactly how much money you need.

Pros of Lines of Credit

✔ Flexible borrowing: Withdraw funds when needed.

✔ Only pay interest on what you use: Unlike personal loans, interest isn’t charged on the full amount unless borrowed.

✔ Reusability: Once you repay, you can borrow again.

Cons of Lines of Credit

✘ The temptation to overspend since funds are always available.

✘ Variable interest rates can increase costs unexpectedly.

✘ A less structured repayment schedule makes budgeting more challenging.

Alternatives to Personal Loans and Lines of Credit

If you’ve decided that neither a personal loan nor a line of credit seems to suit your needs, consider the following alternatives:

1. Credit Cards

- BEST FOR: Small, short-term expenditures

- Pros: They can be more convenient, and they usually come with introductory periods where zero APR is offered.

- Cons: Generally come with high interest rates that start to apply when the promotional period expires.

2. Home Equity Loans

- BEST FOR: Large expenses, such as home renovations.

- Pros: Serves much lower interest while they have fixed repayment terms.

- Cons: You have to apply collateral in the form of equity in your property.

3. Peer-to-Peer Lending (P2P)

- BEST FOR: Borrowers seeking an alternative lender.

- Pros: Flexible loan terms; potentially lower interest rates.

- Cons: Approval is subject to investor interest.

4. 401(k) Loans

- Best for: Borrowers with retirement savings willing to use them

- Pros: Low interest rates, no impact on credit score

- Cons: Risk of retirement savings depletion, penalties if unpaid

5. Payday Loans

- Best for: Emergency, short-term borrowing

- Pros: Quick approval, accessible to most borrowers

- Cons: Extremely high interest rates can lead to debt cycles

6. Borrowing from Friends & Family

- Best for: Flexible repayment terms with no formal lender

- Pros: No interest or minimal fees, customized repayment plans

- Cons: Can strain relationships if not repaid timely

7. Balance Transfer Credit Cards

- Best for: Consolidating high-interest credit card debt

- Pros: 0% APR promotional periods, helps save on interest

- Cons: Requires good credit, balance transfer fees may apply

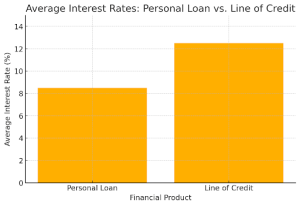

Personal Loan vs. Line of Credit: Key Differences

- Feature: Personal Loan Line of Credit

- Fund Disbursement Lump sum Borrow as needed

- Interest Rates Fixed Variable (in most cases)

- Repayment: Fixed monthly payments, Flexible repayments

- Best For One-time expense,s Ongoing or unpredictable expenses

- Access to Funds: One-time disbursemen,t Continuous access to funds

Choosing the Right Option for You

1. Assess Your Needs

- If you have a specific, one-time expense, a personal loan may be the best choice.

- If you have ongoing or uncertain expenses, a line of credit provides flexibility.

2. Evaluate Your Financial Situation

- A strong credit score improves approval chances for both options.

- Consider your ability to make fixed payments vs. needing flexible repayment terms.

3. Consider Interest Rates & Fees

- Personal loans typically have lower rates because they are structured.

- Lines of credit often have higher, variable interest rates but no origination fees.

4. Review Repayment Terms

- If you prefer a structured plan, a personal loan is better.

- If you need flexibility, a line of credit may work better.

5. Impact on Credit Score

- Both impact credit positively if managed well.

- Late payments on either can damage your credit score.

Expert Tips & Best Practices

When it involves borrowing money, a calculating mind is always a prerequisite. Always borrow sensibly by taking only what you seriously need and making sure that whatever you’re taking will be repaid within the specified arrangement. Don’t just dive head-first into any financial product or service without having read the small print. After reading the small print, you’ll know every fee and penalty included. It should avert unpleasant surprises in the first time. Failing to do that and spend wisely may land you in exorbitant and relentlessly accumulating debts. Before finally signing any papers, you should compare various offers from banks and credit-folding unions or online lenders and pick the one that best fits your requirements.

A budget guarantees that you will make your repayments without placing yourself in a financial squeeze. In the event you are unsure, always seek professional advice from financial consultants. They will address your concerns and advise you appropriately on decisions you should be making in the borrowing process to avoid landing in some financial dilemmas.

Conclusion

Both personal loans and lines of credit serve important financial needs, but choosing the right one depends on your situation. If you’re ready to take the next step, visit Wealthopedia to explore expert-reviewed financial tools, compare lenders, and make smarter borrowing decisions. Whether you need a lump sum for a large one-time purchase or flexible access to funds for ongoing expenses, Wealthopedia helps you choose the solution that fits your goals. Make informed financial choices today with Wealthopedia as your trusted guide.