{kind=link}

Are you confused about how your Private student loans with deferred payments will be disbursed? You’re not alone. Many students and parents navigating the world of Student loans for private schools have questions about where their funds go and how they can access them.

Private student loans are an essential financial resource for many students, supplementing federal aid and scholarships. However, understanding how these loans are disbursed—whether the money goes directly to your school or lands in your account—is crucial for proper financial planning and avoiding unexpected complications.

In this guide, we’ll break down everything you need to know about Uncertified student loan disbursement, ensuring you understand the process, timeline, and key considerations clearly.

Private Loan Disbursement: Who Gets the Money?

One of the primary concerns for borrowers is whether the funds from their private student loan go directly to their school or them. The answer depends on the specific loan agreement and lender policies. There are two primary methods of disbursement:

Direct to School

- When a private student loan is disbursed directly to the school, the lender transfers the approved loan amount to the educational institution. This method ensures that tuition, fees, and institutional costs are covered first, minimizing the risk of misallocating funds. Once the school receives the funds, they apply them toward the student’s outstanding tuition balance and other mandatory fees.

- The school may refund the student if there is any remaining balance after paying the tuition and fees. This excess can be used for other education-related expenses such as books, housing, transportation, and personal expenses. However, students should be mindful that this refund is still borrowed money, and using it wisely can help reduce the overall debt burden.

- By opting for a direct-to-school disbursement, students can ensure their educational costs are covered before receiving additional funds, prevent late payment penalties, and provide financial stability throughout the semester.

Process of Direct-to-School Disbursement

| Step | Description |

| Loan Approval | The lender approves the loan application based on eligibility criteria. |

| Fund Transfer to School | The lender sends the approved loan amount directly to the institution. |

| Application to Tuition & Fees | The school applies the funds to cover tuition, mandatory fees, and institutional charges. |

| Excess Funds Issued to Student | If any funds remain, the school refunds them to the student for additional education-related expenses. |

| Student Manages Remaining Funds | The borrower is responsible for budgeting any refunded amount for necessary expenses. |

Direct to Consumer (Borrower)

When a loan is disbursed to the borrower, the lender transfers the approved amount into the student’s account. This method provides greater flexibility, as the borrower gains complete control over the funds and decides how to allocate them for educational expenses. However, it also requires careful financial planning to ensure that tuition, fees, and other necessary costs are paid on time.

Once the borrower receives the funds, they are responsible for making timely payments to their school to cover tuition and institutional fees. Any mismanagement of these funds can lead to late payments, penalties, or even a risk of enrollment issues. Additionally, borrowers should prioritize using the funds for educational needs, avoiding unnecessary spending that could increase their debt burden.

A significant advantage of direct-to-consumer disbursement is that students can manage their budget and use it for various expenses, including rent, books, transportation, and personal costs related to their education. However, this flexibility comes with a responsibility to ensure that the primary academic expenses are covered first.

Process of Direct-to-Consumer Disbursement

| Step | Description |

| Loan Approval | The lender approves the loan application based on eligibility criteria. |

| Fund Transfer to Borrower | The lender deposits the approved loan amount into the borrower’s bank account. |

| Student Allocates Funds | The borrower must prioritize tuition, fees, and other educational expenses. |

| Payment to School | The borrower is responsible for making tuition and fee payments on time. |

| Managing Remaining Funds | Any excess funds can be used for books, housing, and transportation but should be managed wisely. |

By opting for a direct-to-consumer disbursement, students must exercise strong financial discipline to ensure their academic expenses are covered before using the funds for other purposes. Properly allocating funds can lead to economic hardship, delayed tuition payments, and potential enrollment issues.

Comparison of Disbursement Methods

| Disbursement Method | Pros | Cons |

| Direct to School | Ensures funds are used for tuition and fees | Limited access to excess funds |

| Direct to Consumer | Greater flexibility in fund usage | Requires strong financial management |

Understanding the implications of each option can help you make informed financial decisions.

The Private Loan Disbursement Process: A Step-by-Step Breakdown

Regardless of the disbursement method, the process follows a structured series of steps:

- Loan Application and Approval

- The borrower applies for a private student loan and undergoes a credit check.

- The lender evaluates creditworthiness and determines loan eligibility.

- School Certification

- The school verifies the student’s enrollment and confirms the loan amount needed.

- Certification helps ensure that the borrowed amount aligns with educational expenses.

- Fund Disbursement

- Once the loan is approved and certified, the lender disburses funds directly to the school or the borrower, depending on the loan terms.

- Confirmation and Communication

- The borrower receives notification of the disbursement.

- The school and lender confirm receipt of funds, ensuring that tuition and fees are covered.

Understanding this process is essential to prevent delays and ensure your funds are available when needed.

How Long Does Disbursement Take?

The timeline for disbursement varies based on several factors:

- Lender Processing Time: Some lenders process loans within days, while others may take weeks.

- School Certification: The school must confirm enrollment and cost of attendance, which can take additional time.

- Bank Processing Delays: Fund transfers may be subject to bank processing times, especially for direct-to-consumer loans.

What If There Are Delays?

If your loan disbursement is delayed:

- Contact both your lender and school to identify the issue.

- Ensure all required documents are submitted promptly.

- Check if your school offers short-term emergency funding.

The School’s Role in the Disbursement Process

Educational institutions are critical in ensuring that loan funds are appropriately allocated. Schools act as intermediaries between lenders and students, ensuring compliance with loan agreements and financial regulations. Below are the essential roles schools perform in the loan disbursement process:

Key Responsibilities of Schools in Loan Disbursement

| Responsibility | Description |

| Enrollment Verification | Schools confirm that the borrower is enrolled and eligible for the loan before issuing funds. |

| Loan Amount Certification | Schools ensure that the loan amount does not exceed the cost of attendance as determined by regulations. |

| Application of Funds | Schools allocate the funds towards tuition, fees, and institution-related costs before releasing any excess. |

| Handling Excess Funds | If the loan covers more than tuition and fees, schools refund the remaining balance to the student or return it to the lender. |

| Communication with Lender | Schools coordinate with lenders to finalize the disbursement process and confirm fund receipt. |

| Notifying Students | Students are informed about fund disbursement, remaining balances, and refund processes. |

By playing these roles, schools ensure that students receive their loan funds in a timely and organized manner while preventing excess borrowing beyond the actual cost of attendance. Understanding this process helps students stay informed and manage their educational finances effectively.

Consequences of Late or Failed Disbursements

Delays or failures in disbursement can lead to significant challenges:

- Missed Tuition Deadlines: Late payments may result in additional fees or inability to register for classes.

- Financial Strain: Students relying on excess funds for housing, books, or living expenses may face difficulties.

- Loan Cancellation Risks: Lenders may cancel the loan if disbursement issues persist, leaving students scrambling for alternatives.

What To Do If Disbursement Fails

- Contact your lender immediately to resolve the issue.

- Speak with your school’s financial aid office for guidance.

- Explore emergency funding options to cover short-term expenses.

Handling Excess Loan Funds: What You Need to Know

If your private loan exceeds your school’s cost of attendance, you may receive excess funds. Here’s what you should do:

- Understand Your Options: Some schools return excess funds to the lender, while others issue student refunds.

- Budget Responsibly: If you receive a refund, ensure you use it only for education-related expenses.

- Consider Prepayment: If you don’t need the excess funds, consider applying them to your loan balance to reduce interest costs.

Private Loans and Other Forms of Financial Aid

Private student loans interact with other forms of financial aid, including:

- Federal Student Aid: Unlike federal loans, private loans are not need-based and may require a cosigner.

- Grants and Scholarships: Private loans fill financial gaps after awarding grants and scholarships. Work-study programs: Earnings from work-study jobs can help reduce reliance on private loans.

Understanding how your private loan fits into your overall financial aid package ensures you maximize your funding options effectively.

How Loan Terms Can Affect Disbursement

Loan terms can significantly impact the disbursement process and affect how students manage their education-related finances. Understanding these terms is crucial for borrowers to avoid financial strain and ensure smooth fund allocation.

1. Repayment Plans

Some private student loans require borrowers to make payments while still in school, whereas others allow for deferred payments until after graduation. This can affect cash flow and financial planning:

- Immediate Repayment: Borrowers start making payments as soon as the loan is disbursed, reducing overall interest costs but increasing financial burden during school.

- Interest-Only Repayment: This option requires borrowers to pay only the interest while in school, keeping loan balances from growing but requiring monthly payments.

- Deferred Repayment: No payments are required until after graduation, allowing students to focus on their studies but increasing total loan costs due to accrued interest.

- Graduated Repayment: Payments start lower and gradually increase over time, helping ease initial financial strain but leading to higher long-term interest costs.

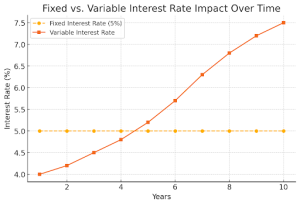

2. Variable vs. Fixed Interest Rates

The type of interest rate can also impact loan disbursement and future repayment obligations:

| Interest Rate Type | Description | Impact on Disbursement & Repayment |

| Fixed Rate | The interest rate remains constant throughout the loan term. | Predictable payments, making budgeting easier. No impact on the disbursement amount. |

| Variable Rate | Interest rates fluctuate based on market conditions. | Monthly payments may change, and disbursement amounts might be impacted if interest rates increase significantly. |

3. Lender-Specific Policies

Different private lenders have unique policies regarding disbursement schedules and eligibility criteria:

- Disbursement Frequency: Some lenders disburse funds in a lump sum, while others release funds in installments based on the school’s academic calendar.

- Enrollment Requirements: Many lenders require students to be enrolled at least half-time to qualify for disbursement.

- Cosignerner Release Policies: Some lenders recognize after a certain number of on-time payments, co-cosignersan approval, and terms.

- Loan Amount Adjustments: Lenders may adjust disbursement amounts based on the total cost of attendance certified by the school.

4. Grace Periods and Early Repayment

Some loans come with a grace period after graduation, allowing students time to find employment before making full payments. However, borrowers who make early payments can reduce total interest costs.

Understanding these loan terms ensures that students can plan accordingly, budget efficiently, and avoid unexpected financial hardships. By carefully evaluating repayment plans, interest rates, and lender policies, borrowers can make informed decisions that align with their financial goals.

Choosing Your Disbursement Path: Pros and Cons

When deciding between direct-to-school and direct-to-consumer disbursement, consider the following:

| Disbursement Method | Pros | Cons |

| Direct to School | Ensures funds are used for tuition and fees | Limited access to excess funds |

| Direct to Consumer | Greater flexibility in fund usage | Requires strong financial management |

Choosing the correct method depends on your financial habits and educational needs.

Your Role in Tracking Loan Disbursement

As a borrower, you ensure your loan is correctly disbursed. Best practices include:

- Regularly Checking Loan Status: Keep track of disbursement updates from your lender and school.

- Maintaining Accurate Records: Document all loan transactions, including disbursements and refunds.

- Monitoring Loan Balances: Regularly review your loan balance to stay on top of repayment obligations.

Conclusion

Understanding private student loan disbursement is essential for effective financial planning. Whether your funds are sent directly to your school or you, tracking and managing your loan can help you avoid financial pitfalls.

If you have questions about managing your Private student loans, contact your lender or school’s financial aid office for guidance. Stay informed and take charge of your financial future!