{kind=link}

Introduction

Student loan consolidation in the United States can seem like a maze of different programs, varying interest rate considerations, and strategic timing. Although most references explain the fundamentals—merging multiple loans into a single payment—borrowers may not always see the lesser-known nuances that can significantly influence their long-term outcomes. Understanding these nuances can help ensure each decision aligns with the borrower’s financial goals.

What Is Student Loan Consolidation?

Student loan consolidation typically means combining multiple loans into one loan, thus making a single monthly payment instead of several. However, there are two distinct ways to consolidate:

- Federal Consolidation (Direct Consolidation Loan):

- Offered by the U.S. Department of Education for federal loans.

- The interest rate becomes a weighted average of all existing federal loan rates, rounded to the nearest one-eighth of a percent.

- It doesn’t lower your overall rate but simplifies the repayment process.

- Private Student Loan Consolidation (Refinancing):

- It involves getting a brand-new private loan—often with a new interest rate—to pay off your existing student loans (either federal or private).

- It could lower your interest rate if you qualify.

- This causes you to lose federal loan benefits if you refinance federal loans.

Who Should Refinance (Private Loan Consolidation) and Who Shouldn’t?

When Refinancing Makes Sense: If you currently hold high-interest private student loans and have a strong credit profile, refinancing can help reduce your interest rate and potentially save you thousands of dollars over the life of your loan. This approach is especially beneficial if you do not expect to utilize federal programs such as income-driven repayment (IDR) or Public Service Loan Forgiveness (PSLF). Moreover, stable employment and consistent income can offer enough security that you won’t feel the absence of federal deferment or forbearance options.

When You Might Want to Pause: If most of your debt is in federal student loans and you’re relying on PSLF or have chosen an IDR plan to keep payments affordable, refinancing could eliminate these benefits and limit flexibility. Similarly, federal protections like extended deferment or forbearance can be crucial safety nets if your job security is questionable or your income fluctuates.

Credit Score Considerations: Even if you decide refinancing is a good idea, a strong credit score or a creditworthy co-signer is typically essential to access the best student loan consolidation rates. If your credit score isn’t high enough to secure a favorable rate, you may want to hold off on refinancing and work on improving your credit profile first.

Federal Student Loan Consolidation vs. Private Student Loan Consolidation

When deciding on the best student loan refinance or consolidation method, weighing the differences between federal and private consolidation is crucial. Below is a comparison table outlining the primary features:

| Feature | Federal Student Loan Consolidation | Private Student Loan Consolidation (Refinancing) |

| Purpose | Combine federal loans into one and keep federal benefits. | Potentially lower interest rates or reduce monthly payments. |

| Eligible Loan Types | Only federal loans (Direct, FFEL, Perkins, etc.). | Federal and/or private loans. |

| Interest Rate | The weighted average of your existing federal rates is rounded up. | Determined by credit score, income, and market conditions. Potentially lower. |

| Impact on Federal Benefits (e.g., PSLF, IDR) | Preserves eligibility for PSLF, income-driven repayment, etc. | Federal benefits are lost upon refinancing. |

| Cost/Fees | There are no fees for consolidation through the Department of Education. | Typically, there are no direct fees, but the final APR depends on credit factors. |

| Repayment Terms | 10-30 years, depending on the consolidation terms. | Varies by lender; can range from 5-20 years. |

| Credit Requirements | None; all federal borrowers can consolidate. | Requires good to excellent credit or a creditworthy co-signer. |

| Best For | Maintaining federal benefits, simplifying repayment. | Lowering rates on private loans, reducing monthly payments, or repaying faster. |

How to Consolidate Your Student Loans

Your next steps depend on whether you opt for federal consolidation or private refinancing. Let’s break it down:

Step A: Federal Student Loan Consolidation

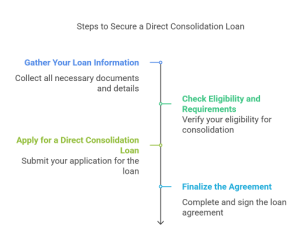

Step 1: Gather Your Loan Information

List all your federal student loans and their loan servicers.

You can find this information on studentaid.gov.

Step 2: Check Eligibility and Requirements

You must have federal student loans (Direct or FFEL) in good standing or default (with rehabilitation options available).

You can consolidate:

A federal loan is available with at least one additional FFEL or Direct Loan.

A loan in default to get a Direct Consolidation Loan to exit default.

Step 3: Apply for a Direct Consolidation Loan

Visit studentaid.gov to complete the Direct Consolidation Loan application.

Select a new loan servicer or stay with your current one if allowed.

Choose a repayment plan, such as:

Standard Repayment Plan

Graduated Repayment Plan

Income-Driven Repayment Plan

Step 4: Finalize the Agreement

Review the terms of your consolidated loan, including the new interest rate.

Sign and submit all required documents online to complete the consolidation process.

Step B: Private Student Loan Consolidation (Refinancing)

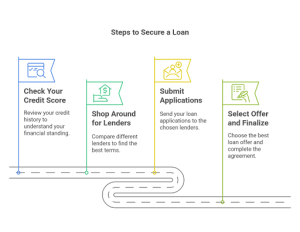

Step 1: Check Your Credit Score

Refinancing typically requires a credit score 650+, though many lenders prefer 700 or higher.

A strong credit profile and a good debt-to-income ratio help secure better refinance rates.

Step 2: Shop Around for Lenders

Compare multiple student loan refinance lenders to find the best deals.

Look for lenders offering flexible repayment terms, competitive interest rates, and borrower protections like temporary forbearance.

Choose lenders with transparent terms and solid reputations.

Step 3: Submit Applications

Many lenders allow you to prequalify using a soft credit check to see estimated rates without affecting your credit score.

Once you select a lender, complete a formal application.

Provide necessary documents like existing loan details, proof of income, and your credit history.

Step 4: Select Offer and Finalize

After approval, choose the best loan offer based on your financial goals—whether it’s the lowest interest rate or a manageable monthly payment.

Sign the loan agreement; the new lender will pay off your existing loans.

Start making payments to your new lender under the agreed terms.

Top 10 Lenders for Private Student Loan Consolidation: A Comprehensive Comparison

| Lender | Who It’s For | Key Calculated Insight | Unique Perks | Learn More |

| SoFi | U.S. borrowers with good credit seeking general refinancing or specialized residency programs (medical/dental). | – $50K at 3.50% APR (10 yrs) ≈ $495/month – Up to ~8.00% AP could push payments to $600/month | – Career coaching, networking – Unemployment protection – Member perks and discounts | Link |

| Laurel Road | Healthcare professionals (medical, dental, pharmacy) looking for in-residency payment options. | – APRs from ~3.70% – A $50K loan could be $500/month – Higher APRs (up to 8.20%) might exceed $600/month | – Tailored for healthcare grads – Reduced in-residency payments – Competitive rates for high-earning fields | Link |

| CommonBond | General graduate borrowers; especially appealing to MBA students; also covers medical, law, and pharmacy. | – Lowest rates ~3.40% – $50K at 3.40% APR (10 yrs) ≈ $494/month | – Social impact model (1-for-1) – Multiple repayment options (fixed, variable, hybrid) – MBA-focused products | Link |

| Earnest | Borrowers need flexible repayments, such as adjusting payment amounts, due dates, etc. | – APR range 3.60% to 8.00% – $50K loan might be $498 to $606/month | – Customizable payment schedule – No origination/prepayment fees – Bi-weekly or varied payment dates | Link |

| College Ave | Students/grads want a quick online process and multiple repayment structures (interest-only, flat). | – Approx. 3.75% APR – $50K at 3.75% over 10 yrs ≈ $502/month | – Fast online sign-up & approvals – Flexible term lengths – Tools to estimate monthly costs | Link |

| LendKey | Borrowers prefer community banks/credit unions for potentially competitive/localized rates. | – Rates from ~3.45% to 7.85% – $50K loan ≈ , $495 to $600/month | – Network of credit unions & community banks – More personalized customer service – No prepayment penalties | Link |

| Citizens Bank | Individuals with existing Citizens Bank relationships benefit from loyalty discounts. | – 3.70% APR on $50K (10 yrs) ≈ $500/month | – 0.25%–0.50% rate discount for existing customers – Consolidates federal & private loans – Simple process for current banking clients | Link |

| Prodigy Finance | International grad students at select U.S. universities (focus on new funding, not traditional refi). | – Based on future earning potential – Monthly payments depend on the academic program & underwriting | – No U.S. co-signer needed – Tailored for international master’s (MBA, STEM) – Flexible approach for those lacking U.S. credit history | Link |

| MPOWER | International & DACA grad students without a U.S. co-signer; more about initial funding vs. classic refi. | – Repayment terms vary by program – Underwriting focuses on career/earning trajectory | – Visa support, career guidance – No co-signer needed – Designed for global borrowers | Link |

| Discover | Borrowers with existing Discover loans or seeking a straightforward, no-fee private lender. | – 4.00% APR on $50K (10 yrs) ≈ $506/month – Up to ~8.25% APR could lead to $614/month | – No late fees (interest still accrues) – 1% cash reward for good grades (in-school) – Simplified structure for Discover customers | Link |

Conclusion

While the core concept of student loan consolidation often comes down to simplifying multiple payments, there are numerous subsidiary factors that American borrowers should keep on their radar. From credit report dynamics and interest capitalization to state-level forgiveness and the strategic timing of market-rate shifts, these details can have a lasting impact on personal finance. By exploring these angles, U.S. borrowers can make more nuanced decisions, ensuring that every aspect of consolidation—federal or private—supports their broader financial strategies and plans. In this way, the loan consolidation process becomes more than an administrative change; it becomes a thoughtful, potentially transformative step in a more significant financial journey.