{kind=link}

Private lenders offer a crucial financial alternative for U.S. borrowers struggling to secure funding through traditional banks. A 2023 Federal Reserve report found that nearly 30% of small business loan applications were denied due to stringent credit requirements, leading many entrepreneurs to seek private lending. The Consumer Financial Protection Bureau (CFPB) also states that over 40% of personal loan applicants face funding challenges due to low credit scores or unconventional income sources.

Unlike traditional bank loans, private lenders come from individuals, private companies, or peer-to-peer (P2P) platforms. These loans are popular among real estate investors, startups, and individuals needing quick financing. Private money lenders provide flexible terms, faster approvals, and fewer credit restrictions. Whether you’re seeking a private loan for business or funding from a direct personal loan lender, private lending offers accessible solutions.

However, private lender loans often carry higher interest rates, shorter repayment periods, and potential regulatory risks. With fintech advancements and alternative lending platforms expanding, borrowers now have more financing options outside traditional banking frameworks.

Who Can Benefit From This Guide?

This comprehensive guide is designed for borrowers looking for flexible financing options and lenders interested in private lending. Whether you’re a real estate investor, a small business owner, or an individual needing financial support, this guide will help you navigate private lender loans effectively.

What Are Private Lender Loans?

Defining Private Lender Loans

Private lender loans originate from non-bank sources. Unlike traditional loans from financial institutions, they can come from private individuals, investment groups, or alternative lending companies.

Who Are Private Lenders?

Private lenders can be categorized as:

- Individual Investors: Wealthy individuals offering loans for investment returns.

- Private Lending Companies: Firms specializing in offering alternative loans.

- Peer-to-Peer (P2P) Lenders: Online platforms connecting borrowers with private investors.

Private lenders often offer more flexibility in loan terms and approval criteria than banks, making them an attractive option for borrowers with unique financial situations. Some borrowers prefer working with a personal loan broker to connect them with the best lending options.

Pros of Private Money Lending

- Fast Approval: Private lenders often approve loans faster than traditional banks.

- Flexible Terms: Borrowers can negotiate repayment schedules and loan structures.

- Access to Capital: Suitable for individuals or businesses that struggle to secure traditional loans.

- Asset-Based Lending: Lenders focus more on collateral than credit history.

Cons of Private Money Lending

- Higher Interest Rates: Private loans typically have higher interest rates than traditional bank loans.

- Less Regulatory Protection: Borrowers may have fewer protections than traditional bank loans.

- Risk of Predatory Lending: Some private lenders may impose unfavorable terms.

- Shorter Repayment Terms: Many private loans require faster repayment schedules, making them function similarly to short-term personal loans.

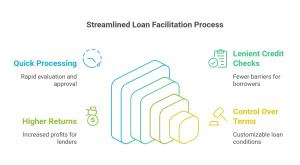

Benefits of Private Lending

- Quick Loan Processing: Private lenders often process loans much faster than traditional banks. Since private lending is less regulated and doesn’t require as much paperwork, borrowers can receive funds in days rather than weeks or months. This is particularly beneficial for real estate investors or businesses that need immediate financing to seize opportunities.

- Less Stringent Credit Requirements: Traditional banks often require a high credit score and a solid financial history. Private lenders, on the other hand, tend to focus more on collateral and the borrower’s ability to repay the loan. Private lending is an excellent option for those with lower credit scores or unconventional income sources.

- Higher Returns for Lenders: Private lenders can benefit from significantly higher interest rates than traditional savings accounts or low-risk investments. This makes private lending an attractive alternative for investors looking to generate passive income while having more control over their investment decisions.

- More Control Over Loan Terms: Unlike traditional bank loans that follow strict guidelines, private lending allows lenders and borrowers to negotiate loan terms. This flexibility can include customized repayment schedules, interest rates, and collateral requirements, making it a mutually beneficial arrangement for both parties.

Risks of Private Lending

- Borrower Default: Higher risk of non-payment compared to traditional lending.

- Liquidity Issues: Private loans are less liquid than other investments.

- Regulatory Challenges: Compliance with state and federal lending laws is required.

- Market Fluctuations: Economic downturns may increase borrower default rates.

When to Choose Private Lending

- If You Need Funds Quickly: Private loans typically have faster approval rates than traditional bank loans. According to industry data, private lenders can approve and disburse loans within 24 to 72 hours, whereas banks often take weeks. For example, real estate investors frequently use private loans to secure properties quickly before competitors.

- If You Have Poor Credit or Non-Traditional Income: Traditional banks rely heavily on credit scores and financial history to approve loans, often requiring a credit score above 650-700 for favorable terms. In contrast, private lenders focus more on collateral and repayment ability, making them ideal for self-employed individuals or those with lower credit scores. A 2023 survey found that over 40% of private loans were granted to borrowers with credit scores below 650.

Types of Private Lender Loans

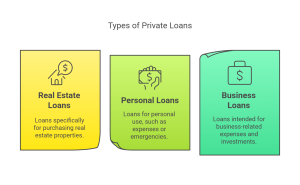

1. Real Estate Private Loans

Usage:

- Fix-and-flip projects: Short-term financing for property renovations.

- Bridge loans: Temporary financing until long-term funding is secured.

- Commercial real estate loans: Capital for acquiring or improving commercial properties.

2. Personal Private Loans

Usage:

- Loans between family members or friends.

- Funds for weddings, medical emergencies, or personal projects.

Unique Aspects:

- More informal agreements.

- Potential risks of straining personal relationships if repayment issues arise.

3. Business Private Loans

Usage:

- Startup funding for entrepreneurs who lack a business credit history.

- Business expansion projects require quick access to capital.

When They Are Better Than Traditional Loans:

- When banks reject loan applications due to limited credit history.

- When businesses need faster approvals than banks can provide.

The Process of Obtaining a Private Lender Loan in the United States

1. Finding a Private Lender

Where to Look

- Networking: Local real estate investment groups, financial advisors, and regional investor meetups often host networking events or maintain member directories. For a starting point, check out the National Real Estate Investors Association (NREIA) or explore real estate–focused meetups on Meetup.com.

- Online Platforms: Several reputable peer-to-peer and private lending sites connect borrowers with individual or institutional investors. Examples include:

- LendingClub – Offers personal loans, business loans, and patient financing solutions.

- Prosper – Known for its quick personal loan approvals.

- PeerStreet – Focuses on real estate–backed loans and crowdfunding opportunities.

2. The Application Process

How It Differs From Traditional Lending

- Fewer Requirements: Private lenders may emphasize your credit score or detailed financial history less, which can benefit borrowers with lower credit or unique circumstances.

- Faster Approvals: Private lenders can often approve loans in days instead of weeks compared to banks or credit unions.

- Asset-Based Focus: Many private lenders place more on collateral (e.g., real estate or valuable assets) than personal financial metrics. Some lenders even provide “soft credit check” options, letting you see potential rates and terms without impacting your credit score.

3. Negotiating Loan Terms

Key Considerations

- Interest Rates: Expect higher rates than traditional bank loans, as private lenders often accept more significant risk.

- Repayment Schedule: Many private or hard money loans have shorter terms—sometimes a year or less—potentially requiring a balloon payment at the end.

- Collateral Requirements: Most private lenders will require real estate or another significant asset as security to protect their investment.

4. Legal and Compliance Aspects

Ensuring all agreements comply with federal and state lending laws, which may vary across the United States, is crucial. Always:

- Use a legally binding contract drafted or reviewed by an attorney.

- Confirm you meet state-specific regulations—consult resources like your state’s attorney general website or review guidelines via the Consumer Financial Protection Bureau (CFPB).

Top 10 Private Lending Platforms

LendingClub

- Personal Loans Up To: $40,000

- Loan Terms Vary From 36 to 60 months

- Users Benefit: Easy online application, competitive interest rates, and transparent fees.

- Link: Visit LendingClub

Prosper

- Personal Loans Up To: $50,000

- Loan Terms Vary From:36 to 60 months

- Users Benefit: Fast approval times and a straightforward application process.

- Link: Visit Prosper

Upstart

- Personal Loans Up To: $50,000

- Loan Terms Vary From 6 to 60 months

- Users Benefit: AI-driven underwriting can help applicants with limited credit history secure lower rates.

- Link: Visit Upstart

SoFi

- Personal Loans Up To: $100,000

- Loan Terms Vary From:2 to 84 months

- Users Benefit: Competitive rates and member perks like career coaching and financial advice.

- Link: Visit SoFi

FundFundraise

- esvestmentmounts Start From: $10

- Typical Holding Period: 3 to 5 years (though timelines can vary)

- Users Benefit: An easy way to diversify into real estate with low minimum investments.

- Link: Visit Fundrise

PeerStreet

- Investment Amounts Start From: $1,000

- Loan Terms Vary From 6 to 36 months (varies by property)

- Users Benefit: Access to curated, real estate-backed loans with detailed underwriting.

- Link: Visit PeerStreet

Kabbage (American Express Business Line of Credit)

- Small Business Lines of Credit Up To:$250,000

- Loan Terms Vary From: to 18 months

- Users Benefit: Quick funding, easy online application, and flexible repayment for entrepreneurs.

- Link: Visit Kabbage

Funding Circle

- Small Business Loans Up To: $500,000

- Loan Terms Vary from months to 5 years

- Users Benefit: Competitive rates, transparent fee structure, and a simple application process.

- Link: Visit Funding Circle

BlueVine

- Lines of Credit Up To: $250,000

- Loan Terms Vary From: 6 o to2 months

- Users Benefit: Fast approvals, straightforward terms, and flexible financing for small businesses.

- Link: Visit BlueVine

Groundfloor

- Investment Amounts Start From: $10

- Loan Terms Vary From: 6 tto12 months

- Users Benefit: Short-term real estate investments with low minimum thresholds.

- Link: Visit Groundfloor

Conclusion

Private lender loans provide flexible financing for real estate, personal, and business needs. However, finding a reputable lender requires due diligence, as understanding the legal and regulatory frameworks is crucial for both borrowers and lenders. Future trends suggest increasing fintech integration and growth in private lending options. Private lending can be a valuable alternative for those who struggle with traditional financing. It’s crucial to weigh the risks and benefits before committing.