What Is a Payoff Amount?

A payoff amount is a document provided by a lender that outlines the total amount required to repay a loan fully as of a specific date. This includes the principal balance, accrued interest, and any additional fees applicable to close the loan account. Borrowers typically request a payoff amount when they intend to pay off debt, invest a loan early, refinance, or sell an asset tied to the loan, such as a home or vehicle.

A payoff amount differs from a loan balance, as it includes the principal and interest that has accrued up to the payoff date and any potential fees. Understanding the full scope of a payoff amount is crucial for borrowers looking to close their debt properly without any outstanding liabilities.

Payoff Meaning

The term payoff refers to the final payment to settle a loan or financial obligation fully. It signifies the completion of a borrower’s debt and ensures the loan is closed in the lender’s records. In economic terms, a payoff amount represents the total sum needed to satisfy the outstanding loan balance and any applicable charges.

Payoff Quote

A payoff quote is an estimate the lender provides that details the amount required to settle the loan. It is usually valid for a certain period and includes the outstanding principal, interest, and fees. Borrowers use a payoff quote to plan their loan repayment effectively.

Breakdown of a Payoff Quote

| Component | Description |

| Outstanding Principal | The remaining balance of the loan is yet to be repaid. |

| Accrued Interest | The interest accumulated on the loan since the last payment. |

| Fees & Charges | Any prepayment penalties, late fees, or administrative costs. |

| Total Payoff Amount | The sum of all components required to settle the debt fully. |

| Expiration Date | The date until which the payoff quote remains valid. |

By understanding the components of a payoff quote, borrowers can ensure they have the correct funds available and avoid any surprises when making their final payment.

{kind=link}

Difference Between Payoff Amount and Remaining Balance

Many borrowers confuse the payoff amount with the remaining balance on their loan. However, they are not the same:

Remaining Balance: This refers to the unpaid portion of the loan’s principal without factoring in accrued interest and additional fees.

Payoff Amount: This includes the remaining balance, plus any accrued interest, prepayment penalties, and other lender-imposed charges. The payoff amount is the actual total needed to fully settle the debt.

Related: Learn how to deal with debt to avoid confusion between terms like payoff amount and loan balance.

| Feature | Remaining Balance | Payoff Amount |

| Definition | The unpaid portion of the loan’s principal. | The total amount required to settle the loan entirely. |

| Includes Interest? | No, only principal balance. | Yes, accrued interest is included. |

| Includes Fees? | No additional fees. | Yes, it may include prepayment penalties and administrative charges. |

| Used For? | General tracking of the amount owed. | To determine the exact amount needed to close the loan. |

| Fluctuates Over Time? | No, unless principal payments are made. | Yes, as daily interest accrues. |

- Understanding this difference helps borrowers plan their final loan payments accurately.

How a Payoff Amount Works

When a borrower decides to pay off a loan before the scheduled term ends, they must request a payoff amount from their lender. The lender will provide a detailed breakdown of all the costs associated with the final loan repayment. This breakdown typically includes:

- Principal Balance: The remaining unpaid portion of the loan.

- Accrued Interest: The interest accumulated on the loan since the last payment.

- Prepayment Penalties (if applicable): Fees some lenders charge for paying off the loan early.

- Other Fees: Processing fees, administrative costs, or any additional charges that must be paid to close the loan.

The total payoff amount is usually valid only for a limited time since interest continues to accrue daily. Borrowers must ensure their payment reaches the lender by the specified expiration date in the payoff amount to avoid adjustments or additional charges.

Steps to Obtain a Payoff Amount

1. Contact the Lender

Borrowers must contact their loan servicer or lender to request the payoff amount. This request can usually be made through an online portal, over the phone, or via a written request. Specifying the intended payoff date is essential so the lender can calculate the exact amount.

2. Receive the Payoff Statement

After processing the request, the lender will issue a payoff statement with the amount required to satisfy the loan. This document includes the principal balance, accrued interest, and additional fees such as prepayment penalties or administrative charges. Due to daily interest accrual, the statement is typically valid for a short period.

3. Review the Details

Before making a payment, borrowers should carefully review the payoff statement to ensure all fees are accounted for correctly. If there are any discrepancies, it is essential to contact the lender immediately to clarify and make necessary adjustments.

4. Make the Payment

Once the borrower confirms the accuracy of the payoff amount, they can proceed with making the full payment. Lenders may have specific requirements regarding accepted payment methods, such as wire transfers, certified checks, or online payments. Ensuring that the payment is made within the validity period of the payoff statement prevents additional interest from accruing.

5. Confirm Loan Closure

After making the final payment, borrowers should request and verify confirmation from the lender that the loan has been fully settled. The lender should provide a written confirmation or a release of lien, especially for mortgages or auto loans. This ensures no further obligations or outstanding balances are related to the loan.

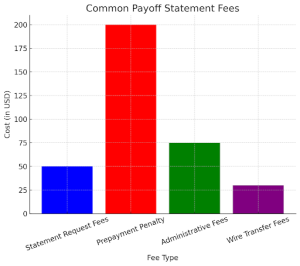

Payoff Statement Fees

Lenders may charge various fees associated with generating and processing a payoff statement. These fees can vary depending on the type of loan and the lender’s policies. Common fees include:

- Statement Request Fees: Some lenders charge a fee for issuing a formal payoff statement.

- Prepayment Penalty: Certain loans, such as mortgages or auto loans, may have prepayment penalties if paid before the agreed-upon term.

- Administrative Fees: Lenders may charge processing or administrative fees to generate the payoff statement.

- Wire Transfer Fees: If the borrower chooses to pay via wire transfer, banks or lenders may charge a fee for processing the transaction.

Understanding these fees beforehand can help borrowers make informed decisions and avoid unexpected costs.

Why Is a Payoff Amount Important?

Understanding and requesting a payoff amount is crucial for borrowers looking to manage their finances efficiently. Key reasons why obtaining a payoff amount is important include:

Avoiding Overpayments: Since a payoff amount includes all necessary fees and interest accrued, borrowers avoid overpaying or underpaying.

Preventing Additional Interest Charges: If a borrower mistakenly pays only the principal balance without accrued interest, the loan may not be fully settled, leading to additional charges.

Ensuring Smooth Loan Closure: A formal payoff amount helps avoid discrepancies and ensures that the loan is properly closed in the lender’s records.

Facilitating Refinancing or Property Sale: In cases of mortgage refinancing or home sales, obtaining a payoff statement is essential for a smooth transaction.

Budgeting for Final Payment: Borrowers can plan their finances effectively when they have a clear understanding of the total payoff amount.

Curious about related financial decisions? Explore whether to pay off debt or invest based on your unique goals.

Conclusion

A payoff amount is an essential document that provides borrowers with the exact total required to fully settle their loan. Whether it’s a mortgage, auto loan, student loan, or personal loan, understanding the details of a payoff statement ensures borrowers can efficiently close their debt without unexpected charges.

By carefully reviewing the payoff amount, considering all fees, and ensuring timely payment, borrowers can successfully manage their financial obligations and avoid unnecessary complications. Additionally, understanding the balance between paying off debt vs. saving for retirement helps individuals make informed financial decisions that align with their long-term goals.