{kind=link}

Key Takeaway

- Capital One charges off unpaid accounts after 180 days, marking them as losses but leaving you responsible for the debt.

- Expect in-house collection efforts, including phone calls, letters, and potential lawsuits, which can lead to wage garnishments or asset liens.

- Settling old balances involves lump-sum payments or structured plans. Always confirm agreements in writing to avoid disputes and hidden fees.

- An emergency fund covering three to six months of expenses helps prevent serious new debt if unexpected financial costs arise.

- Seek nonprofit clearing credit counseling for unbiased guidance, personalized repayment strategies, and timely support, ensuring you regain control of your finances.

When a credit card payment slips past due, the clock starts ticking. For millions of Americans, that ticking morphs into a relentless drumbeat as debts age—and companies like Capital One deploy strategies to recover what’s owed. But what exactly does Capital One do on old credit card debts? And how can you shield yourself from financial fallout while building a safety net (like an emergency fund)? Let’s break it down.

The 180-Day Tipping Point: When Debt Becomes a Charge-Off

Capital One, like most lenders, follows a strict timeline. If your account reaches 180 days past due, they’ll typically charge it off—a technical term meaning they’ve closed the account and labeled it a loss. But here’s the catch: You still owe the debt. Charge-offs appear on your credit report, cratering your score and inviting aggressive collection tactics.

According to Capital One’s official guidelines, charged-off accounts are sent to internal collections teams. Unlike some banks that outsource to third-party collectors, Capital One often handles this process in-house, giving them tighter control over recovery efforts.

How Capital One Pursues Old Debts: Lawsuits, Settlements, and Subprime Strategies

Capital One has a reputation for assertive debt recovery. A ProPublica investigation revealed that the company files more lawsuits against borrowers than other major banks. This stems partly from their focus on subprime lending—issuing credit to those with lower credit scores. While this expands access to credit, it also increases default risks.

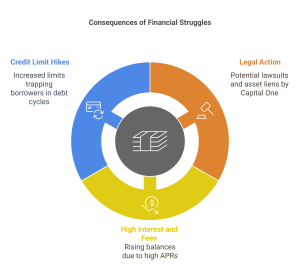

Key Tactics in Their Playbook:

- Legal Action: Capital One may sue to garnish wages or place liens on assets.

- Interest and Fees: APRs as high as 27% can inflate balances even after charge-offs.

- Credit Limit Hikes: Ironically, they might increase your limit while you’re struggling, a tactic criticized for trapping borrowers in debt cycles.

A 2024 Economic Liberties report highlights how Capital One’s data-driven models target vulnerable demographics, maximizing profits through interest and fees.

What This Means for You: Risks and Realities

If you’re dealing with old Capital One debt, expect persistent outreach: calls, letters, and potentially court summons. Ignoring it won’t make it disappear. Here’s what’s at stake:

- Credit Score Damage: Charge-offs linger on reports for 7 years, affecting loan approvals and interest rates.

- Collections Lawsuits: Capital One’s legal filings can lead to wage garnishment.

- Debt Inflation: High APRs mean even small balances can balloon.

Your Escape Plan: Navigating Debt Relief Options

Facing old debt? You’ve got options. Here’s how to regain control:

| Strategy | How It Works | Best For |

| Negotiate a Settlement | Capital One may accept a lump-sum payment (often 30–60% of the balance). | Those with some savings. |

| Debt Management Plan | Work with a nonprofit credit counselor to reduce rates and consolidate payments. | Borrowers with multiple debts. |

| Bankruptcy | A last-resort option to discharge debts (Chapter 7 or 13). | Severe, unmanageable debt. |

Pro Tip: Always get settlement agreements in writing. Capital One’s debt relief page outlines official pathways, but third-party credit counselors can offer neutral guidance.

Why an Emergency Fund Matters More Than Ever

Here’s where the secondary keyword fits in: how much should you have in an emergency fund? The answer: 3–6 months of expenses. Why? Because liquid savings can prevent reliance on credit cards during crises—a buffer against future debt.

Without an emergency fund: A $1,000 car repair might go on a credit card, risking another debt spiral.

With savings: You cover the cost upfront, sidestepping interest and stress.

Building this fund takes time, but even $500 can mitigate minor emergencies. Automate small weekly transfers to start.

Final Thoughts: Knowledge Is Power

Capital One’s approach to old debts is shaped by profit motives and risk algorithms. While their tactics are legal, they’re not always consumer-friendly. Protect yourself by:

- Responding to lawsuits: Show up in court or negotiate beforehand.

- Checking your credit report: Dispute inaccuracies dragging your score down.

- Prioritizing savings: An emergency fund is your first line of defense.

Got old debt hanging over you? Act now—settle, negotiate, or seek counseling. And if you’re debt-free, start stashing cash for life’s curveballs. Your future self will thank you.

Still unsure where to start? Explore nonprofit resources like the National Foundation for Credit Counseling for free advice.