{kind=link}

Key Takeaways

- Yes, if you need better financial control, want to prevent Overspending, and aim to develop disciplined saving habits.

- No, if you have irregular income, fluctuating expenses, or require more flexibility in budgeting.

- Prevents Overspending: Helps manage daily expenses and avoid unnecessary purchases.

- Encourages Financial Discipline: Builds mindful spending habits for long-term stability.

- May Lack Flexibility: Not ideal for fluctuating expenses or unexpected costs.

- Best with a Flexible Approach: A weekly or monthly budget might work better for some individuals.

- Personalized Budgeting is Key: Choose what aligns with your lifestyle and financial goals.

Introduction

Budgeting is a fundamental aspect of financial planning that helps individuals manage their money efficiently. Among the various budgeting methods, setting a daily budget is a strategy many people adopt to control spending and ensure financial stability. But should you limit yourself to a daily budget?

A daily budget involves allocating a fixed amount of money for everyday expenses. While this method can help curb overspending and encourage mindful spending habits, it also comes with potential limitations. This article explores the benefits, drawbacks, and best practices of using a daily budget so that you can determine if it aligns with your financial goals.

A daily budget involves allocating a fixed amount of money for everyday expenses. While this method can help curb overspending and encourage mindful spending habits, it has potential limitations. This article explores the benefits, drawbacks, and best practices of using a daily budget so that you can determine if it aligns with your financial goals.

What Is a Daily Budget?

A daily budget refers to a set amount of money you allocate for spending each day. It is derived by:

- Calculating your total monthly income.

- Subtracting fixed expenses such as rent, utilities, loan payments, and subscriptions.

- Setting aside money for savings and investments.

- Dividing the remaining balance by the number of days in the month.

For instance, if your monthly discretionary income (after fixed expenses) is $1,500, your daily budget would be around $50. This method ensures controlled spending while allowing flexibility for essential expenses.

Why Do People Use a Daily Budget?

People opt for a daily budget to gain better financial control, avoid unnecessary spending, and maintain a disciplined approach to money management. It provides structure, helping individuals track their expenses more effectively.

Pros of Limiting Yourself to a Daily Budget

1. Prevents Overspending

A daily budget helps restrict unnecessary expenditures and ensures that your spending stays within a reasonable limit. It reduces the risk of splurging on non-essential items and encourages mindful purchases.

2. Enhances Financial Discipline

You develop strong financial habits and avoid impulsive spending by setting a specific spending limit daily. This discipline can help you achieve long-term economic stability and savings.

3. Helps Manage Debt Efficiently

A structured daily budget ensures that your money is allocated wisely, reducing the need for credit cards and loans. Over time, this can lead to debt reduction and better financial health. For added support, consider using a credit card payment tracker to monitor repayment progress.

4. Encourages Savings Growth

Since a daily budget prevents unnecessary expenses, it naturally promotes saving. Even small, consistent savings contribute to significant financial growth over time.

5. Reduces Financial Stress

Knowing exactly how much you can spend daily eliminates anxiety related to Overspending or financial uncertainty. A clear budget creates peace of mind and financial confidence.

Cons of Limiting Yourself to a Daily Budget

1. Lack of Flexibility

One of the most significant drawbacks of a daily budget is its rigidity. Some days require more spending than others, and a strict daily cap may not account for unexpected expenses, leading to frustration.

2. Can Be Difficult to Maintain

Tracking daily expenses requires constant monitoring and discipline, which can be exhausting—many struggle to stick to a strict budget due to changing financial needs.

3. May Not Work for Every Lifestyle

A daily budget is not suitable for everyone, especially for those with irregular income or fluctuating expenses. Certain careers or lifestyles require variable spending patterns that do not align with a fixed daily cap. Learn more about how to deal with debt in flexible ways if this applies to you.

4. Can Lead to Unnecessary Restrictions

A daily budget might sometimes create an overly restrictive mindset, making people feel guilty about spending even when necessary. This can reduce enjoyment and create a negative relationship with money.

How to Effectively Use a Daily Budget

To maximize the benefits of a daily budget while minimizing its drawbacks, consider these best practices:

1. Establish a Realistic Daily Limit

Set a budget that aligns with your spending needs rather than choosing an arbitrary number. Consider both fixed and variable expenses to determine a practical limit.

2. Use a Weekly or Monthly Perspective

Instead of rigidly following a daily budget, think in terms of weekly or monthly allowances. This allows for flexibility—spending less on some days while having more room for necessary expenses on others. Here’s what is the best budgeting tactic for paying off debt that might work better for some situations.

3. Track Expenses Regularly

Use budgeting apps or spreadsheets to monitor daily spending patterns. This helps you identify trends and make necessary adjustments.

4. Prioritize Essential Expenses

Ensure that your budget covers necessary expenses, such as groceries, transportation, and bills, before allocating money for non-essentials.

5. Adjust Your Budget When Needed

A daily budget should not be completely rigid. Adjust it based on changing circumstances, relief advisory agencies such as income fluctuations, unexpected costs, or lifestyle changes.

How to Stick to a Budget: Detailed Strategies for Financial Success

Budgeting is essential for financial stability, but sticking to a budget can be challenging. Consistency is key in choosing a daily, weekly, or monthly budget. Here are some practical strategies for effectively sticking to your budget and maintaining financial discipline.

1. Set Realistic Budget Limits

A budget only works if it is realistic and achievable. Many people set overly strict budgets, leading to frustration and failure.

How to Set a Realistic Budget:

- Analyze Your Spending Patterns: Review the last three months of expenses to determine how much you typically spend.

- Categorize Expenses: Divide spending into fixed expenses (rent, utilities, loans) and variable expenses (food, entertainment, shopping).

- Set an Achievable Goal: If you usually spend $800 on groceries, cutting it to $300 is unrealistic. Instead, reduce it gradually.

- Leave Room for Flexibility: Unexpected expenses arise, so allow some breathing space in your budget.

2. Track Expenses Regularly

Keeping track of expenses helps identify where your money goes and prevents Overspending.

Effective Ways to Track Expenses:

- Use Budgeting Apps: Apps like Mint, YNAB, and PocketGuard automate tracking.

- Maintain a Spreadsheet: A simple Excel or Google Sheet can record income and expenses.

- Keep a Spending Journal: Writing down every purchase increases awareness and accountability.

- Review Weekly: Set a time to analyze your expenses and adjust if needed.

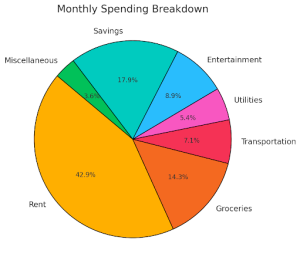

Graph: Monthly Spending Breakdown

This graph shows how people typically allocate their monthly budgets to rent, groceries, transportation, and entertainment categories.

3. Prioritize Essential Expenses

Before spending on wants, ensure that all needs are covered.

How to Prioritize Expenses:

- List All Essentials: Housing, utilities, insurance, groceries, transportation, and debt payments.

- Use the 50/30/20 Rule: Allocate 50% for needs, 30% for wants, and 20% for savings or debt repayment.

- Cut Non-Essential Spending: If your budget is tight, limit dining out, subscriptions, and impulse shopping.

4. Use the Envelope System

A cash-based system that prevents Overspending by allocating cash to different spending categories.

How to Implement the Envelope System:

- Withdraw cash at the beginning of the month.

- Label envelopes for categories (groceries, transportation, entertainment, etc.).

- Only spend what’s in the what. Once the money is gone, you can no longer pay in that category.

- Adjust as needed. Transfer from less-used categories if necessary.

This method is highly effective for controlling discretionary spending.

5. Plan for Unexpected Costs

Financial emergencies can derail your budget, so always plan for them in advance.

How to Prepare for Unexpected Expenses:

- Create an Emergency Fund: Save at least 3-6 months’ money in a separate account.

- Set Up an Emergency Category: Allocate 5-10% of your budget for unplanned costs.

- Avoid Relying on Credit Cards: Using credit for emergencies can lead to debt accumulation.

6. Review and Adjust Periodically

A budget isn’t static—it doesn’t evolve as your income and expenses change.

How to Regularly Review Your Budget:

- Conduct Monthly Reviews: Assess spending patterns and make necessary changes.

- Adjust for Life Changes: Salary increases, unexpected expenses, and financial goals should be reflected.

- Refine Categories: If you consistently overspend in one area, adjust limits accordingly.

Review and Adjust Periodically

7. Practice Mindful Spending

Mindless spending is a budget killer. Being intentional about purchases prevents financial stress.

How to Develop Mindful Spending Habits:

- Ask, “Do I need” this?” before making a “purchase.

- Delay Impulse Purchases: Wait 24-48 hours before buying non-essentials.

- Compare Prices & Look for Discounts: Use price comparison tools to get the best deals.

- Unsubscribe from Marketing Emails: Reduces temptation to spend unnecessarily.

8. Set Savings Goals

Having clear financial goals motivates you to stick to your budget.

How to Set and Achieve Savings Goals:

- Define Specific Goals (e.g., save $5,000 for a vacation, pay off $10,000 in debt).

- Set a Timeline: Decide when you want to reach each goal.

- Automate Savings: Schedule automatic transfers to your savings account.

- Track Progress Monthly: Regularly review how close you are to meeting your goal.

Should You Limit Yourself to a Daily Budget?

A daily budget can be an effective financial tool for those who:

A daily budget can be an effective financial tool for those who:

Struggle with overspending and impulse purchases.

Want to develop strong financial discipline.

Are focused on debt repayment or aggressive savings goals.

Prefer a structured approach to managing money.

However, it may not be ideal for individuals with:

Irregular income or variable expenses.

A lifestyle that requires flexibility in spending.

The ability to manage finances effectively without strict daily limits. Some may instead consider if it’s smarter to pay off debt or invest based on financial priorities.

Final Verdict

While limiting yourself to a daily budget can be helpful, it is essential to strike a balance. Instead of rigidly following a set amount daily, consider a more flexible approach—such as a weekly or monthly budget—to accommodate changing expenses. The key is to find a budgeting method that works best for your financial situation and long-term goals.

Conclusion

A daily budget is a powerful tool for controlling expenses, promoting savings, and maintaining financial stability. However, its effectiveness depends on your lifestyle, nonprofit debt consolidation, financial habits, and spending needs. A daily budget can help build better financial discipline if used wisely, but a flexible and personalized approach is often the best way to manage money successfully.

By evaluating your financial goals, you can determine whether limiting yourself to a daily budget is the right strategy.