{kind=link}

Introduction

The collection calls won’t stop. Your mailbox fills with past-due notices faster than you can open them. The knot in your stomach tightens each time you check your bank balance. If this sounds familiar, you’re not alone. Millions of Americans are drowning in debt, wondering if bankruptcy is the only life raft available.

But here’s the truth: bankruptcy doesn’t have to be your only option. While it might seem like the quickest escape from overwhelming debt, there are several effective alternatives that can help you regain financial control without the long-term consequences of filing bankruptcy.

As someone who’s helped countless individuals navigate their way out of debt, I’ve seen firsthand how the right approach can transform financial distress into stability—all while protecting your credit score and assets.

Understanding Your Debt Relief Options

Before diving into specific strategies, it’s important to understand the full spectrum of debt relief options available to you. Each comes with its own advantages, timelines, and impact on your financial future.

Debt Consolidation: Simplify Your Payments

Debt Consolidation: Simplify Your Payments Debt consolidation involves combining multiple debts into a single loan, typically with a lower interest rate. This approach creates one manageable monthly payment instead of juggling multiple due dates and varying interest rates.

How it works: You take out a new loan (often a personal loan, home equity loan, or balance transfer credit card) and use it to pay off your existing debts. Then, you make payments on this single loan.

Best for: People with good enough credit to qualify for a lower interest rate than they’re currently paying.

Debt Management Plans: Professional Negotiation

A debt management plan (DMP) is a structured repayment program arranged by a nonprofit credit counseling agency.

How it works: The agency works with your creditors to reduce interest rates and waive fees. You make one monthly payment to the agency, which then distributes funds to your creditors.

Best for: Those who need lower payments and interest rates but don’t qualify for a consolidation loan.

Debt Settlement: Negotiate a Lower Balance

Debt settlement involves negotiating with creditors to accept less than the full amount you owe.

How it works: Either you or a debt settlement company negotiates with creditors to settle debts for less than you owe. Often, this requires having a lump sum available to offer asa settlement.

Best for: People with serious financial hardship who can’t afford to repay the full amount but want to avoid bankruptcy.

Important note: This option can significantly impact your credit score and may have tax implications, as forgiven debt over $600 is generally considered taxable income.

DIY Debt Payoff Strategies

Sometimes, the most effective approach is to tackle your debt independently through strategic repayment methods.

The Avalanche Method

Pay minimum payments on all debts while putting extra money toward the debt with the highest interest rate first. Once that’s paid off, move to the next highest interest-rate debt.

Best for: Saving the most money on interest over time.

The Snowball Method

Focus on paying off your smallest debt first (regardless of interest rate), then roll that payment into the next smallest debt, creating momentum as you go.

Best for: Those who need psychological wins to stay motivated.

Comparison of Debt Relief Options

| Strategy | Timeline | Credit Score Impact | Best For |

| Debt Consolidation | 2-5 years | Minimal initial dip; improves with on-time payments | Good-to-excellent credit; multiple high-interest debts |

| Debt Management Plan | 3-5 years | Minimal negative impact; improves with program completion | Fair credit; the need for lower interest/payments |

| Debt Settlement | 2-4 years | Significant negative impact (50-150 points) | Severe financial hardship; unable to afford full repayment |

| DIY Debt Payoff | Varies | Positive impact with consistent payments | Self-disciplined individuals with stable income |

Step-by-Step Guide to Becoming Debt-Free

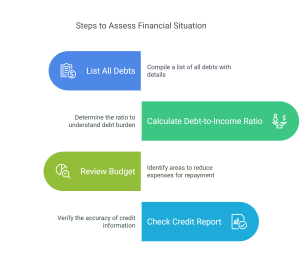

Step 1: Assess Your Financial Situation

List all your debts, calculate your debt-to-income ratio, review your budget, and check your credit report.

- List all your debts: For each debt, note the creditor, balance, interest rate, minimum payment, and due date.

- Calculate your debt-to-income ratio: Divide your total monthly debt payments by your gross monthly income.

- Review your budget: Identify expenses you can reduce to free up money for debt repayment.

- Check your credit report: Request free reports from AnnualCreditReport.com to ensure all information is accurate.

Step 2: Consider Credit Counseling

A session with a nonprofit credit counselor can provide valuable guidance and help you understand your options.

The National Foundation for Credit Counseling and the Financial Counseling Association of America are reputable organizations that can connect you with certified counselors.

During your session, the counselor will:

- Review your financial situation

- Suggest appropriate debt relief options

- Help create a personalized action plan

Most agencies offer free initial consultations, making this a low-risk step to take.

Step 3: Negotiate Directly with Creditors

Many people don’t realize that creditors are often willing to work with you—they’d rather get some payment than none at all.

Try these negotiation tactics:

- Request hardship programs if you’ve experienced job loss, medical issues, or other financial setbacks

- Ask for interest rate reductions

- Propose a lump-sum settlement if you have savings available

- Request a payment plan with affordable monthly amounts

Pro tip: Always get any agreement in writing before making payments under a negotiated arrangement.

Step 4: Implement Your Chosen Strategy

Whether it’s debt consolidation, a DMP, settlement, or DIY, commit fully. Use bonuses, sell items, and reduce expenses to accelerate.

For DIY debt payoff, consider using these strategies to accelerate your progress:

- Allocate windfalls (tax refunds, bonuses, gifts) to debt repayment

- Take on a temporary side hustle dedicated solely to debt payoff

- Sell unused items and put the proceeds toward your debt

- Cut unnecessary expenses and redirect the savings to debt payments

Step 5: Rebuild Your Financial Foundation

As you work on eliminating your debt, simultaneously focus on building financial habits that will prevent future problems.

Essential financial habits:

- Build an emergency fund (start with $1,000, then work toward 3-6 months of expenses)

- Track spending consistently

- Live below your means

- Save automatically through payroll deductions

- Review and adjust your budget monthly

Protecting Your Rights and Credit Score

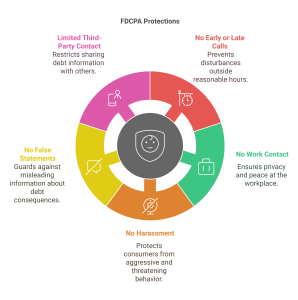

Understanding Your Legal Protections

Understanding Your Legal Protections The FDCPA ensures collectors follow rules. Violations can be reported to the CFPB.

Call before 8 a.m. or after 9 p.m.

- Contact you at work if you’ve told them not to

- Use harassing or threatening language

- Make false statements about the consequences of non-payment

- Contact third parties about your debt (except in limited circumstances)

If you experience violations, you can file a complaint with the Consumer Financial Protection Bureau.

Statutes of Limitations on Debt

Most consumer debts have a statute of limitations—a time limit after which creditors cannot sue you to collect. These limits vary by state and debt type:

- Credit card debt: 3-10 years

- Medical debt: 3-10 years

- Personal loans: 3-6 years

- Auto loans: 4-6 years

Important: Making a payment on an old debt can restart the statute of limitations clock in many states. Before paying on an old debt, consult with a consumer law attorney.

Minimizing Credit Score Damage

While most debt relief strategies (except for consistent on-time payments) will have some impact on your credit score, there are ways to minimize the damage:

- Continue making minimum payments while negotiating with creditors

- Ask creditors to report accounts as “paid as agreed” or “paid in full” rather than “settled” when you complete payments

- Build a positive credit history through secured credit cards or credit-builder loans

- Keep credit utilization below 30% on any remaining credit accounts

- Monitor your credit reports regularly and dispute inaccuracies

FAQ: Your Debt Relief Questions Answered

General Debt Relief Questions

Q: What are the best ways to get rid of debt without filing bankruptcy? A: The most effective approaches include debt consolidation loans, debt management plans (DMPs), debt settlement programs, credit counseling, direct negotiation with creditors, and strategic DIY repayment methods like the avalanche or snowball approach.

Q: Will debt consolidation hurt my credit score? A: Initially, you might see a small dip in your score due to the credit inquiry and opening a new account. However, over time, making consistent payments on your consolidation loan can significantly improve your score by establishing a payment history and reducing your credit utilization ratio.

Q: How does debt settlement differ from debt consolidation? A: Debt settlement involves negotiating with creditors to accept less than the full amount owed, while debt consolidation combines multiple debts into one loan, typically at a lower interest rate. Settlement can damage your credit score more severely but may be necessary in cases of severe financial hardship.

Q: How long will debt management take to become debt-free? A: Most debt management plans are designed to help you become debt-free within 3-5 years, depending on your total debt amount and what you can afford to pay monthly.

Credit Score Concerns

Q: How long does it take to improve my credit after debt consolidation? A: You’ll typically begin seeing improvements within 6-12 months of making consistent, on-time payments. Significant improvement usually occurs after 1-2 years of responsible credit management.

Q: Will negotiating with creditors hurt my credit score? A: It depends on how the creditor reports the resolution to credit bureaus. Accounts reported as “settled” or “settled for less than full amount” will negatively impact your score, though less severely than bankruptcy. Try to negotiate for “paid as agreed” reporting when possible.

Legal Questions

Q: Can creditors still sue me if I avoid bankruptcy? A: Yes, creditors retain the right to sue for unpaid debts within the statute of limitations. However, proactively communicating and negotiating with creditors often prevents legal action.

Q: Can creditors garnish my wages if I don’t file for bankruptcy? A: In most states, creditors can garnish your wages, but only after successfully suing you and obtaining a court judgment. Federal law limits garnishment to 25% of your disposable income in most cases.

Q: Is there a statute of limitations on debt in the U.S.? A: Yes. Depending on your state and the type of debt, the statute of limitations typically ranges from 3-10 years. After this period expires, creditors cannot legally sue you to collect, though they may still attempt collection.

Debt Repayment Strategy

Q: Which debt should I pay off first? A: Financial experts recommend either the avalanche method (highest interest rate first) to save the most money or the snowball method (smallest balance first) to build momentum through quick wins. Choose the approach that best matches your financial situation and personality.

Q: Can medical debt be negotiated down? A: Yes, medical debt is often among the most negotiable types of debt. Many healthcare providers offer hardship programs, interest-free payment plans, or significant discounts for cash payments.

Conclusion: Your Path Forward

Dealing with overwhelming debt can feel isolating, but remember—millions of Americans have stood where you are now and found their way to financial freedom without bankruptcy.

The journey requires commitment, patience, and sometimes tough choices, but the reward—financial peace of mind—is worth every sacrifice. Whether you choose debt consolidation, credit counseling, settlement, or a DIY approach, the important thing is to take that first step.

Begin by reaching out to a nonprofit credit counselor for a free consultation. This single action can provide clarity and direction, helping you understand which path is best for your unique situation.

Remember: This challenging chapter in your financial story doesn’t define your future. With the right strategy and consistent effort, you can write a new chapter—one of financial confidence, security, and freedom.

Start your journey with expert insights from Wealthopedia—your trusted source for financial freedom strategies

Disclaimer: This article provides general information and should not be construed as financial or legal advice. Consult with a qualified professional regarding your specific situation.