{kind=link}

Though a burden to many, debt can be conquered with discipline and the aid of modern technology; no longer must one rely solely on manual calculations or tedious tracking; instead, a host of digital tools now stands ready to assist in the quest for financial liberation. In this treatise, we shall explore the most effective debt payoff applications, their strengths, and the additional strategies that can hasten the path to financial independence when combined with these tools.

The Most Effective Debt Payoff Applications

1. Bright Money

.webp)

Key Features:

- APR: Varies based on user profile

- Loan Purpose: Debt consolidation, credit card payoff

- Loan Amounts: Custom per user

- Terms: AI-driven debt repayment strategies

- Credit Needed: No strict credit score requirement

- Origination Fee: None

- Early Payoff Penalty: None

- Late Fee: Depends on the lender

✅ Pros:

- AI-driven financial coaching

- Helps automate and optimize debt payments

- No minimum credit score requirement

- Offers credit-building strategies

- Personalized repayment plans

❌ Cons:

- Subscription-based service (some features require a paid plan)

- Limited to credit card debt management

- No direct lending options

- AI suggestions may not fit all financial situations

- No in-person customer service

2. Debt Payoff Assistant

Key Features:

- APR: Custom per user

- Loan Purpose: Debt tracking and repayment

- Loan Amounts: Unlimited (user-defined)

- Terms: Snowball and avalanche repayment methods

- Credit Needed: N/A

- Origination Fee: None

- Early Payoff Penalty: None

- Late Fee: N/A

✅ Pros:

- Free mobile app

- Supports multiple debt payoff methods

- Simple interface for beginners

- No impact on credit score

- No hidden fees

❌ Cons:

- No direct loan consolidation services

- No automation features

- No financial coaching or AI insights

- Limited tracking for complex financial situations

- Available only for iOS users

3. Vertex42

Key Features:

- APR: N/A

- Loan Purpose: Debt planning via spreadsheets

- Loan Amounts: User-defined

- Terms: Manual calculations based on debt models

- Credit Needed: N/A

- Origination Fee: None

- Early Payoff Penalty: None

- Late Fee: None

✅ Pros:

- Free Excel and Google Sheets templates

- Customizable debt repayment tracking

- No subscription or hidden fees

- Ideal for detailed financial planning

- Works offline

❌ Cons:

- Requires manual data entry

- No automation or AI assistance

- No mobile app

- Not user-friendly for beginners

- No direct debt payoff solutions

4.Unbury.me

Key Features:

- APR: User-defined

- Loan Purpose: Debt repayment planning

- Loan Amounts: Custom per user

- Terms: Snowball and avalanche payoff strategies

- Credit Needed: N/A

- Origination Fee: None

- Early Payoff Penalty: None

- Late Fee: None

✅ Pros:

- Free online calculator

- Simple and easy-to-use

- No sign-up required

- Supports multiple payoff strategies

- Helps visualize debt repayment progress

❌ Cons:

- No mobile app

- No automation or reminders

- No financial coaching or AI insights

- Lacks additional budgeting tools

- No customer support

5.Undebt.it

Key Features:

- APR: Custom per user

- Loan Purpose: Debt management and payoff

- Loan Amounts: User-defined

- Terms: Snowball, avalanche, and custom strategies

- Credit Needed: N/A

- Origination Fee: None

- Early Payoff Penalty: None

- Late Fee: None

✅ Pros:

- Supports multiple debt payoff methods

- Customizable repayment plans

- Free version available

- Tracks progress over time

- Option to sync with bank accounts

❌ Cons:

- Paid features are required for full access

- No mobile app

- No direct debt consolidation options

- It can be complex for beginners

- Limited customer service

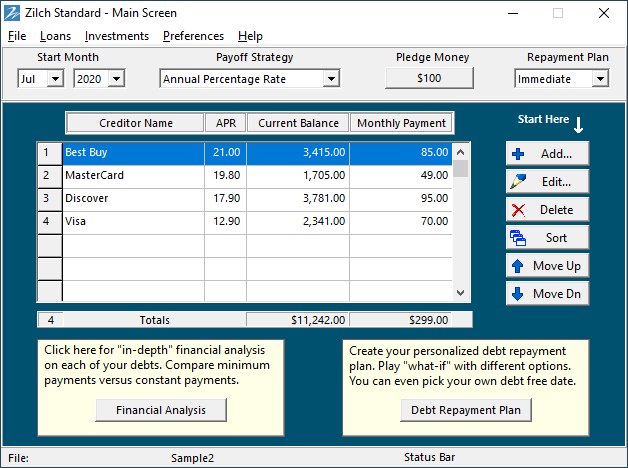

6.ZilchWorks

Key Features:

- APR: N/A

- Loan Purpose: Debt elimination strategy planning

- Loan Amounts: User-defined

- Terms: Snowball debt payoff strategy

- Credit Needed: N/A

- Origination Fee: None

- Early Payoff Penalty: None

- Late Fee: None

✅ Pros:

- Simple and easy-to-use software

- One-time payment, no subscription fees

- Focuses on debt elimination strategies

- Works offline

- No credit check is required

❌ Cons:

- No mobile app

- No financial coaching

- Not suitable for complex financial planning

- Lacks automation

- No bank syncing feature

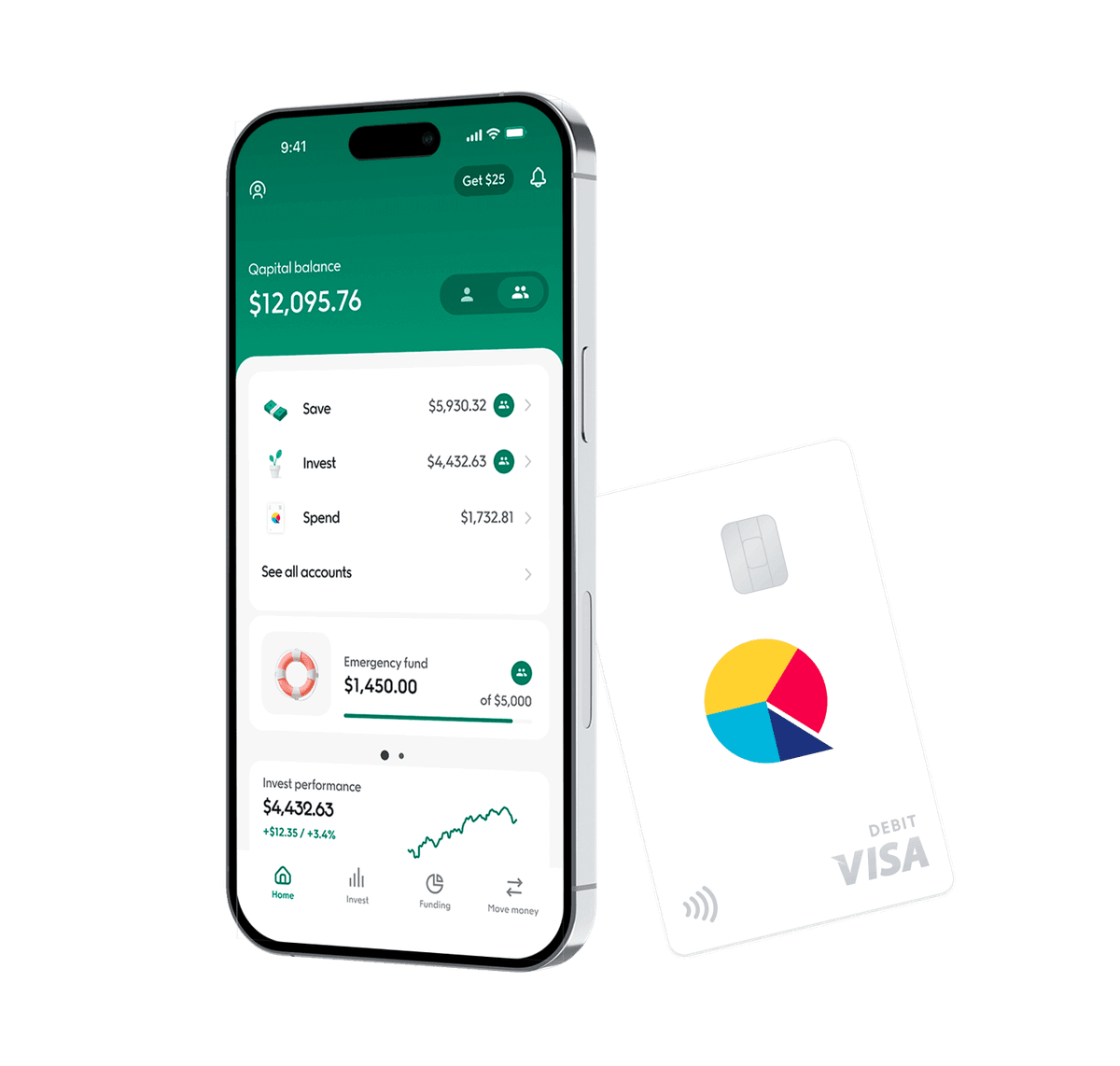

7. Qapital

Key Features:

- APR: N/A

- Loan Purpose: Debt saving and budgeting

- Loan Amounts: User-defined

- Terms: Automated savings rules

- Credit Needed: N/A

- Origination Fee: None

- Early Payoff Penalty: None

- Late Fee: None

✅ Pros:

- Automates savings for debt repayment

- Customizable savings rules

- Financial goal tracking

- It helps improve money habits

- Offers investment options

❌ Cons:

- Monthly subscription required

- No direct debt payoff strategies

- No free version

- No loan consolidation options

- Requires linking bank accounts

8. Debt Payoff Planner

Key Features:

- APR: User-defined

- Loan Purpose: Debt repayment planning

- Loan Amounts: User-defined

- Terms: Snowball and avalanche methods

- Credit Needed: N/A

- Origination Fee: None

- Early Payoff Penalty: None

- Late Fee: None

✅ Pros:

- Free and easy-to-use mobile app

- Supports multiple debt payoff methods

- Helps track progress

- No impact on credit score

- Simple interface

❌ Cons:

- No financial coaching

- No automation features

- No direct debt consolidation options

- Limited customization for unique financial situations

- Limited to mobile users

Further Methods to Expedite Debt Repayment

Though these digital tools provide invaluable assistance, true financial emancipation requires a multi-faceted approach. Let us now examine additional methods that, when employed alongside these applications, will accelerate one’s escape from debt.

- The Augmentation of Payments

One of the most effective means of hastening debt repayment is to exceed the minimum monthly obligation. By contributing additional funds—whether derived from bonuses, tax refunds, or a reallocation of existing resources—the debtor reduces overall interest and expedites their journey toward financial sovereignty. - The Elimination of Superfluous Expenditures

A thorough examination of one’s financial habits often reveals opportunities for reduction. Luxuries once deemed essential—frequent dining, subscriptions, unnecessary purchases—may, upon closer inspection, prove expendable. Redirecting such funds toward debt repayment serves not only to hasten one’s freedom but to instill discipline and financial prudence. - The Strategy of Refinancing and Consolidation

Should the weight of high-interest debt prove insurmountable, one may seek refuge in refinancing or debt consolidation. By securing a lower interest rate or merging multiple obligations into a singular, manageable payment, the burden is lightened, allowing for a more structured and efficient path toward resolution. - The Application of the Snowball and Avalanche Methods

Among the most effective repayment strategies are two renowned approaches:

The Snowball Method, wherein smaller debts are vanquished first, providing psychological victories that fortify resolve.

The Avalanche Method, which prioritizes high-interest debts, ensuring minimal financial waste and maximal efficiency.

Each method, though distinct in philosophy, serves the same ultimate goal: financial freedom. Learn more about choosing the best budgeting tactic for paying off debt. - The Pursuit of Additional Income

For those willing to accelerate their progress, the acquisition of supplementary income may prove invaluable. Freelance endeavors, side ventures, or part-time engagements can provide the necessary funds to decimate debt at an unprecedented rate, hastening the transition from debtor to financial sovereign.

Debt Repayment and the Restoration of Credit: The Path to Financial Sovereignty

To be free from debt is not merely to escape financial obligation but to take command of one’s financial destiny. The weight of debt extends beyond the present, casting a long shadow over future opportunities, increasing borrowing costs, and restricting financial freedom. True liberation comes not only from settling debts but from transforming one’s financial habits. By utilizing strategic tools, such as a credit card payment tracker, individuals can monitor their progress, ensure timely payments, and maintain control over their financial commitments. The process of debt repayment is more than just relief—it is the cornerstone upon which creditworthiness is restored and long-term financial independence is built.

The Profound Impact of Debt Repayment on Credit Health

The repayment of debt is akin to the restoration of a once-mighty citadel. Every timely payment, every reduction in balance, and every strategic financial decision contributes to the reconstruction of one’s financial standing. The benefits of this restoration are manifold, touching upon all aspects of financial life.

1. The Power of Reduced Credit Utilization

One of the most significant indicators of financial health is credit utilization, which measures the percentage of one’s available credit that is actively in use. A high credit utilization ratio signals risk to lenders, suggesting that an individual is overly reliant on borrowed funds. However, as debts are repaid, the utilization ratio declines, demonstrating financial discipline and stability.

How Credit Utilization Affects Your Credit Score:

- Credit utilization accounts for 30 percent of a FICO score, making it one of the most influential factors.

- A utilization rate below 30 percent is generally recommended for maintaining strong credit, but below 10 percent is optimal.

- Lower balances signal to creditors that an individual is not financially overextended, increasing their attractiveness as a borrower.

By systematically repaying debts and keeping balances low, one strengthens their financial reputation, ensuring that future credit—should it be needed—is offered on favorable terms.

2. Strengthening Credit Through Improved Payment History

If there is one element of credit restoration that reigns supreme, it is payment history. Accounting for 35 percent of a FICO credit score, payment history is the most heavily weighted factor in credit scoring models. A single missed payment can lower a score by 100 points or more, while consistent on-time payments steadily elevate it.

Steps to Strengthen Payment History:

- Automate payments to ensure bills are paid on time, avoiding costly penalties and credit damage.

- Prioritize debt obligations with the highest interest rates or those closest to delinquency.

- Maintain long-term consistency—a sustained period of on-time payments gradually erases the impact of past missteps.

By ensuring debts are repaid on schedule, one demonstrates reliability and responsibility, restoring their standing in the financial world and earning the trust of creditors.

3. Unlocking Superior Financial Opportunities

With a robust credit profile comes the gateway to greater financial autonomy. Those burdened by poor credit face a financial landscape riddled with high-interest rates, unfavorable loan terms, and restricted access to capital. However, those who have successfully restored their credit through debt repayment apps find themselves positioned to reap significant rewards.

Benefits of a Strong Credit Profile:

- Lower interest rates: A higher credit score translates to reduced borrowing costs, whether for a mortgage, auto loan, or personal credit line.

- Increased loan approval rates: Lenders are more inclined to approve applicants with a history of responsible credit management.

- Better credit card offers: High-limit, low-interest, and rewards-based credit cards become available, providing financial flexibility.

- Improved employment and housing prospects: Many employers and landlords conduct credit checks—strong credit can influence hiring decisions and rental approvals.

- Negotiating power: A stellar credit score provides leverage to negotiate better loan terms and credit card perks.

Benefits of a Strong Credit Profile:

- Lower interest rates: A higher credit score translates to reduced borrowing costs, whether for a mortgage, auto loan, or personal credit line.

- Increased loan approval rates: Lenders are more inclined to approve applicants with a history of responsible credit management.

- Better credit card offers: High-limit, low-interest, and rewards-based credit cards become available, providing financial flexibility.

- Improved employment and housing prospects: Many employers and landlords conduct credit checks—strong credit can influence hiring decisions and rental approvals.

- Negotiating power: A stellar credit score provides leverage to negotiate better loan terms and credit card perks.

Debt repayment is not merely about closing old accounts; it is about opening doors to a financial future marked by lower costs, greater freedom, and increased wealth-building potential.

Final Thoughts

The quest for a debt-free existence is not one of ease, but of discipline, strategy, and persistence. These digital tools, when employed wisely, serve as powerful allies in this journey. Whether one seeks automation, structured planning, or a blend of both, there exists an app to align with every strategy.

Through the consistent application of these resources, coupled with sound financial habits, one shall ascend from the depths of debt and embrace a future unshackled by financial constraints.

Which among these tools shall you choose? Have you embarked upon your own debt-free journey? Share your insights and experiences in the comments below.

Which among these tools shall you choose? Have you embarked upon your own debt-free journey? Share your insights and experiences in the comments below.