{kind=link}

Key Takeaways:

- Credit unions offer superior debt consolidation options compared to traditional banks, with lower interest rates (6-18% APR vs. 12-25% APR), minimal fees, and personalized service because they’re member-owned nonprofits rather than shareholder-focused corporations.

- Top national options include Navy Federal, PenFed, First Tech Federal, and Alliant Credit Union, all offering loans up to $50,000 with competitive rates, though local community credit unions may provide even more personalized service and specialized programs.

- Beyond lower rates, credit union debt consolidation provides valuable benefits, including potential credit score improvement, financial education resources, relationship banking advantages, and the certainty of a fixed payoff date.

The Weight of Multiple Debts: You’re Not Alone

Do you check your mailbox with a sense of dread? Are you juggling multiple payment due dates each month? Does it feel like you’re making payments but your debt isn’t getting any smaller?

I get it. Last year, I watched my friend Sarah—a dedicated elementary school teacher—struggle with exactly this problem. Despite her responsible spending habits, a medical emergency followed by an unexpected car repair forced her to rely on credit cards with sky-high interest rates. By the time she came to me for advice, she was managing five different payments each month, all with different due dates and interest rates hovering around 22%.

“I feel like I’m drowning,” she told me over coffee one Saturday morning. “I make good money, but it’s all going to minimum payments.”

Sarah’s story isn’t unique. In fact, the average American household carries $8,942 in credit card debt alone, according to recent data from the Federal Reserve. When you add medical bills, personal loans, and other forms of debt, it’s no wonder many hardworking professionals feel overwhelmed.

But there’s good news: credit unions across the United States are offering a lifeline through debt consolidation loans with terms that put community members—not profits—first.

What Makes Credit Unions Different for Debt Consolidation?

Before we dive into specific credit unions, let’s understand why these member-owned financial cooperatives might be your best bet for debt consolidation.

Unlike traditional banks that answer to shareholders demanding ever-increasing profits, credit unions are nonprofit organizations owned by their members. This fundamental difference shapes everything from their interest rates to their customer service philosophy.

Credit Unions vs. Banks: The Debt Consolidation Comparison

| Feature | Credit Unions | Traditional Banks |

| Average Interest Rate on Debt Consolidation Loans | 6%-18% APR | 12%-25% APR |

| Application Fees | Often minimal or none | Typically $75-$100 |

| Prepayment Penalties | Rarely | Common |

| Approval Flexibility | Can consider factors beyond the credit score | More rigid qualification criteria |

| Customer Service | Personalized, community-focused | Often impersonal, call-center based |

| Profit Structure | Returns benefits to members | Prioritizes shareholder returns |

“Working with a credit union felt like having a financial partner rather than just another account number,” Sarah told me after finding her solution. “The loan officer actually remembered my name when I called with questions.”

Top Credit Unions for Debt Consolidation in 2025

While membership requirements vary, most Americans can find at least one credit union they’re eligible to join. Here are some standout options for debt consolidation:

1. Navy Federal Credit Union

Don’t let the name fool you—while Navy Federal primarily serves military members and their families, their membership eligibility extends to Department of Defense civilian employees and contractors as well.

Highlights:

- Debt consolidation loans up to $50,000

- APRs starting around 7.99%

- No application fees

- Flexible terms from 36 to 60 months

[Insert image of Navy Federal Credit Union branch or logo]

2. PenFed (Pentagon Federal) Credit Union

PenFed has opened its membership to everyone, making it one of the most accessible nationwide credit unions.

Highlights:

- Competitive rates starting at 6.99% APR

- Loan amounts from $500 to $50,000

- No origination fees

- Quick online application process

3. First Tech Federal Credit Union

First Tech offers membership to employees of select tech companies, state residents of Oregon, and members of the Financial Fitness Association (which anyone can join for a small fee).

Highlights:

- Personal loans up to $50,000

- Terms up to 84 months

- No prepayment penalties

- Relationship discounts for existing members

4. Alliant Credit Union

Anyone can join Alliant by becoming a member of Foster Care to Success (Alliant covers the $5 membership fee).

Highlights:

- Debt consolidation loans from $1,000 to $50,000

- APRs as low as 6.24% for excellent credit

- Same-day funding available

- No origination fees

5. Local Community Credit Unions

Don’t overlook smaller, local credit unions. They often offer the most personalized service and may have special programs for community members facing financial challenges.

How to Know If a Credit Union Debt Consolidation Loan Is Right for You

Sarah’s situation made her an ideal candidate for debt consolidation, but is it right for you? Consider these factors:

Debt consolidation makes sense if:

- You’re juggling multiple high-interest debts

- You can secure a lower overall interest rate

- You prefer the simplicity of one monthly payment

- You’re committed to not accumulating new debt while paying off the consolidation loan

“I actually sat down with a loan officer who helped me crunch the numbers,” Sarah shared. “She showed me exactly how much I’d save each month and over the life of the loan. It was about $300 monthly and over $7,000 total—that’s a life-changing difference.”

The Debt Consolidation Application Process: What to Expect

Applying for a credit union debt consolidation loan is straightforward, but preparation is key. Here’s what you’ll need:

- Proof of income (pay stubs, tax returns, or bank statements)

- Employment verification (usually a letter from your employer)

- Current debt statements (credit card bills, medical bills, loan documents)

- Personal identification (driver’s license, passport)

- Credit report (most credit unions will pull this themselves)

While approval times vary, many credit unions can approve applications within 2-3 business days, with funding following shortly after.

The Hidden Benefits of Credit Union Debt Consolidation

Beyond the obvious advantages of lower interest rates and simplified payments, credit union debt consolidation loans offer several less obvious benefits:

1. Credit Score Improvement

While your score might initially dip due to the hard inquiry, many people see significant improvements within 6-12 months as they make consistent payments and reduce their credit utilization ratio.

2. Financial Education Resources

Many credit unions offer free financial counseling and educational resources to help members address the root causes of debt and build healthier financial habits.

3. Relationship Banking Benefits

As you establish a relationship with your credit union, you may qualify for better rates on future loans, including mortgages and auto loans.

4. Debt Payoff Date Certainty

Unlike minimum payments on credit cards that can stretch repayment over decades, a debt consolidation loan gives you a clear payoff date.

Common Questions About Credit Union Debt Consolidation

Can I consolidate all types of debt with a credit union loan?

Typically, unsecured debts like credit card balances, medical bills, and personal loans can be consolidated. Secured debts like mortgages usually cannot be included in this type of loan. However, some credit unions offer specialized programs that may help with secured debt—it’s worth asking about your specific situation.

Do I need to be a member of a credit union to apply for a debt consolidation loan?

Yes, you’ll need to become a member first but don’t let this deter you. Membership requirements are usually straightforward, such as living in a specific area, working for certain employers, or joining affiliated organizations. Many credit unions allow you to join and apply for a loan in the same visit.

How will a debt consolidation loan affect my credit score?

Initially, your credit score may see a slight dip due to the credit inquiry. However, consistently making payments on time can significantly improve your credit score over time. In Sarah’s case, her score increased by 68 points within eight months of consolidating her debt.

What if my credit isn’t perfect? Can I still get a debt consolidation loan?

Credit unions are often more flexible than traditional banks when it comes to credit requirements. Many will consider factors beyond your credit score, including your income stability, debt-to-income ratio, and overall financial picture. Some even offer special programs for members with damaged credit.

Taking the First Step Toward Financial Freedom

If you’re feeling overwhelmed by multiple debts—whether from credit cards, medical bills, or personal loans—a credit union debt consolidation loan could be your pathway to financial peace.

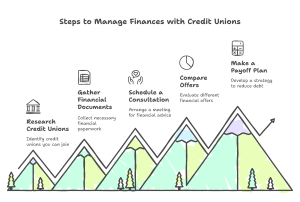

Here’s your action plan:

- Research credit unions you’re eligible to join (remember, there’s likely at least one that will welcome you)

- Gather your financial documents (income proof, debt statements)

- Schedule a consultation (many credit unions offer free financial counseling)

- Compare offers (look beyond the interest rate to fees and terms)

- Make a payoff plan (commit to not accumulating new debt)

Remember, the credit union difference isn’t just about better rates—it’s about working with a financial institution that genuinely wants to see you succeed.

Ready to take control of your debt? Comment below with your biggest question about debt consolidation, or share your own success story to inspire others on their financial journey!