{kind=link}

KeyTake Away

- Personal loans consolidate multiple high-interest debts into one manageable monthly payment, reducing the hassle of juggling various due dates and interest rates, which streamlines financial planning.

- Borrowers benefit from lower interest rates and predictable payments, allowing them to save money on interest while effectively building a clear roadmap towards debt freedom.

- Financial advisors and counselors guide individuals through the loan selection process, assisting in comparing rates, fees, and terms from different lenders for consistently improved outcomes.

- Critical considerations include verifying eligibility, addressing underlying spending habits, ensuring no new debt accumulation, and making consolidation a disciplined step towards long-term financial wellness steadily.

Are you juggling multiple credit card payments every month? Struggling to keep track of various interest rates and due dates? A personal loan for debt consolidation might be the financial lifeline you’ve been searching for.

The Debt Juggling Act: Why Americans Are Turning to Consolidation

Let’s face it—managing multiple debt payments can feel like trying to keep a dozen plates spinning at once. One missed payment, and the whole system comes crashing down, potentially damaging your credit score in the process.

That’s why more Americans are turning to personal loans for debt consolidation as a strategic financial move. These loans aren’t just another debt—they’re a tool for simplifying your financial life while potentially saving you thousands in interest payments.

What Exactly Is a Personal Loan for Debt Consolidation?

A personal loan for debt consolidation allows you to combine multiple high-interest debts (like credit cards, medical bills, or store cards) into a single loan with one monthly payment. Rather than tracking five different due dates and interest rates, you’ll have just one payment to remember.

Here’s what makes these loans particularly attractive:

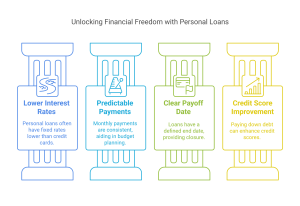

- Fixed interest rates that are typically lower than credit card rates

- Predictable monthly payments that make budgeting easier

- Clear payoff date so you can see the light at the end of the debt tunnel

- Potential credit score improvement as you pay down revolving debt

Is Debt Consolidation Right for You?

Meet Donna, a 45-year-old healthcare administrator who found herself with $22,000 spread across four credit cards after unexpected medical expenses and helping her daughter through college. With interest rates between 18-24%, she was paying nearly $600 monthly—mostly toward interest.

“I felt like I was on a financial treadmill,” Donna shares. “Every month, I’d make payments, but the balances barely moved because of the high interest.”

After researching her options, Donna secured a personal loan with a 10.5% interest rate and a 48-month term. Her new payment: $563 per month—slightly less than before, but now with a definite end date and more of each payment going toward the principal.

This scenario might sound familiar if you’re in a similar situation to our “Debt Consolidation Donna” persona—a mid-career professional looking to streamline finances and reduce interest burdens.

How to Determine if Consolidation Makes Financial Sense

Before applying for a personal loan to pay off credit card debt, ask yourself these questions:

- Will I actually save money? Calculate whether the new interest rate will reduce your overall interest expense.

- Can I commit to no new debt? Consolidation only works if you address the root causes of debt accumulation.

- Do I qualify for a competitive rate? Your credit score will largely determine the interest rate you’re offered.

What Credit Score Do You Need for Debt Consolidation?

According to data from the Federal Reserve, your credit score significantly impacts the rates you’ll be offered:

| Credit Score Range | Typical Interest Rate Range | Likelihood of Approval |

| Excellent (720+) | 7-12% | Very High |

| Good (690-719) | 10-15% | High |

| Fair (630-689) | 15-20% | Moderate |

| Poor (below 630) | 20-36% of denial | Low |

If you identify with our “Credit Cautious Chloe” persona—someone who’s experienced credit setbacks but is proactively rebuilding—you might need to shop around more extensively or consider a co-signer if your score falls in the lower ranges.

Finding the Best Personal Loans for Debt Consolidation

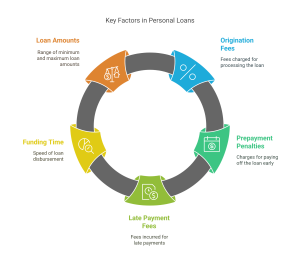

For individuals like “Frugal Frank” who are committed to securing the best financial deal, thorough comparison shopping is essential when exploring personal loans for debt consolidation. It is important to look beyond the headline interest rates and evaluate the complete cost structure and flexibility of each loan option. One of the most critical factors is the origination fee, which typically ranges from 1% to 8% of the loan amount. This fee can be deducted from the disbursement or added to the overall loan balance, meaning it can substantially increase your effective cost of borrowing.

Additionally, borrowers should pay close attention to prepayment penalties. These fees are charged if you decide to pay off the loan early, potentially offsetting any savings from a lower rate. Evaluating the lender’s policy on late payment fees and grace periods is also vital, as some lenders offer a brief period of leniency while others impose strict penalties from the first day of delay.

Funding time is another essential consideration; some lenders provide near-instant approvals and funding within a few days, while others may take up to a week or more, affecting your ability to consolidate debt quickly. Finally, review the minimum and maximum loan amounts available. Even if a lender offers competitive rates, the loan size must align with your consolidation needs. By carefully comparing these elements, you can choose a personal loan that truly supports your journey toward financial stability and achieve lasting financial freedom today.

- Origination fees (typically 1-8% of the loan amount)

- Prepayment penalties (charges for paying off the loan early)

- Late payment fees and grace periods

- Funding time (how quickly you’ll receive the money)

- Minimum and maximum loan amount

Online lenders often offer more competitive rates and faster approval than traditional banks, but don’t dismiss your existing bank relationships—they may offer loyalty discounts.

The Consolidation Process: Step by Step

- Check your credit score to understand what rates you might qualify for

- Calculate your total debt across all accounts you want to consolidate

- Research lenders and compare rates (many offer prequalification with a soft credit check)

- Apply for the loan that offers the best terms for your situation

- Use the funds to pay off existing debts immediately

- Set up automatic payments for your new loan to avoid missed payments

- Consider closing unnecessary credit cards, but be aware this may temporarily impact your credit utilization ratio

Common Questions About Personal Loans for Debt Consolidation

Q: How long does it typically take to get approved for a personal loan?

A: The approval process varies widely by lender. Online platforms may provide decisions within minutes and funding within 1-3 business days, while traditional banks might take 5-7 business days for the entire process. If you need funds quickly, prioritize lenders known for fast processing.

Q: Can consolidating debt with a personal loan improve my credit score?

A: Yes, in several ways. First, paying off credit cards reduces your credit utilization ratio—a major factor in credit scoring. Second, adding an installment loan to your credit mix (if you primarily have revolving credit) can positively impact your score. Finally, making consistent, on-time payments demonstrates financial responsibility.

However, be aware that the initial application will trigger a hard inquiry, which might temporarily lower your score by a few points.

Q: Are there any fees involved with personal loans for debt consolidation?

A: Many lenders charge origination fees ranging from 1-8% of the loan amount. For example, on a $20,000 loan with a 5% origination fee, you’d pay $1,000 in fees—often deducted from the loan proceeds. Some lenders also charge prepayment penalties or late payment fees. Always read the fine print before signing.

Q: What alternatives exist to personal loans for debt consolidation?

A: Depending on your situation, consider:

- Balance transfer credit cards with 0% introductory APR (good for those who can pay off the debt during the promotional period)

- Home equity loans or lines of credit (if you own a home with sufficient equity)

- Debt management plans through nonprofit credit counseling agencies

- 401(k) loans (as a last resort due to potential tax implications and retirement impact)

Warning Signs: When Debt Consolidation Might Not Be Right

While personal loans for debt consolidation work well for many, they’re not a universal solution:

- If you haven’t addressed the spending habits that led to debt

- If the fees and interest on the new loan exceed what you’re currently paying

- If you’re likely to run up new credit card debt after consolidating

- If you’re just a few months away from paying off your existing debt

Remember, consolidation is a tool for managing debt—not a magical solution that makes debt disappear.

Taking the Next Step Toward Financial Freedom

If you’ve read this far, you’re already taking positive steps toward managing your debt more effectively. Personal loans for credit card debt can be a powerful strategy for regaining control of your finances, but they work best as part of a comprehensive approach to financial health.

Before you apply, take time to:

- Review your complete financial picture

- Set clear goals for debt repayment

- Create a realistic budget that prevents new debt accumulation

- Compare multiple lenders to find your best option

Ready to explore your personal loan options? Start by checking your credit score and researching reputable lenders who specialize in debt consolidation. Your future self will thank you for taking this important step toward financial freedom.

Have you used a personal loan for debt consolidation? Share your experience in the comments below!