{kind=link}

Are you juggling multiple debt payments each month, watching interest pile up faster than you can pay it down? You’re not alone. Millions of Americans wake up every day feeling the weight of financial stress on their shoulders. But here’s the good news: debt consolidation programs might be the lifeline you’ve been searching for.

What Exactly is a Debt Consolidation Program?

Simply put, a debt consolidation program combines multiple debts into one monthly payment, typically at a lower interest rate. Instead of keeping track of various due dates and interest rates, you make a single payment – often with better terms than your original debts.

Think of it like organizing a messy closet. Rather than having clothes scattered everywhere, you’re neatly arranging everything in one place. Your finances deserve the same treatment!

How Debt Consolidation Works in Real Life

Let’s break this down with a real-world scenario:

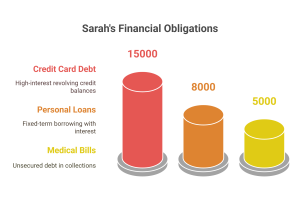

Sarah, a 30-year-old marketing professional, has:

- $15,000 in credit card debt (19% APR)

- $8,000 in personal loans (14% APR)

- $5,000 in medical bills (no interest but in collections)

She’s making minimum payments but barely making a dent in her principal balance. After consulting with a financial counselor, Sarah decided to apply for a debt consolidation loan through her credit union.

She qualified for a $28,000 loan at 8% APR for 5 years. Now, instead of juggling multiple payments and sky-high interest rates, Sarah makes one affordable monthly payment. Plus, she’ll save thousands in interest over the life of the loan.

Types of Debt Consolidation Programs: Finding Your Perfect Match

Not all debt consolidation programs are created equal. Let’s explore your options:

| Program Type | Best For | Pros | Cons |

| Debt Consolidation Loans | People with good credit | Lower interest rates, fixed payment schedule | Requires a decent credit score |

| Balance Transfer Credit Cards | Credit card debt | 0% intro APR periods | Transfer fees, temporary low rates |

| Home Equity Loans | Homeowners with equity | Low interest rates, tax-deductible interest | Risk of foreclosure if you default |

| Debt Management Plans | Those needing counseling | Professional guidance, possible fee waivers | It may require closing credit accounts |

| Personal Loans | Varied debt types | No collateral required, quick funding | Potentially higher interest than secured options |

Who Should Consider Debt Consolidation?

For The Struggling Young Professional

If you’re between 25-35, building your career while battling student loans and credit card debt from those lean early years, debt consolidation can be your strategic move.

Your Goals:

- Simplify your financial life when you’re already juggling career demands

- Lower those monthly payments to breathe easier

- Build your credit score for future milestones (home ownership, anyone?)

Jake, a 28-year-old software developer, found himself with $45,000 in student loans and $12,000 in credit card debt after moving to a high-cost city for work. “I was making good money but still living paycheck to paycheck because of my debt,” he explains. “Consolidating gave me one payment to focus on and saved me about $300 monthly in interest charges.”

For Family-Oriented Homeowners

When you’re juggling mortgage payments, childcare costs, and perhaps saving for college tuition, debt consolidation can free up cash flow for your family’s needs.

Your Goals:

- Consolidate various credit lines into a manageable system

- Reduce your overall debt burden to support your family’s needs

- Potentially use your home equity responsibly to secure better terms

“After our second child was born, we realized our credit card debt from medical bills and home repairs was holding us back from saving for their education,” shares Michael, a 42-year-old accountant. “Using a home equity loan to consolidate saved us $450 monthly and put our family budget back on track.”

For Pre-Retirement Savers

If retirement is on the horizon (ages 50-65), eliminating high-interest debt becomes urgent to maximize your nest egg.

Your Goals:

- Quickly reduce high-interest debts that eat into retirement savings

- Gain tight control over monthly expenditures

- Achieve debt-free retirement

Barbara, 58, consolidated $32,000 in various debts through a personal loan with a 3-year term. “I was determined to enter retirement debt-free,” she says. “The consolidation loan gave me a clear end date, and I’ll make my final payment six months before my planned retirement.”

For Credit-Challenged Consumers

If financial hardships have impacted your credit score, specialized debt consolidation programs can help rebuild your financial foundation.

Your Goals:

- Rebuild creditworthiness through structured repayment.

- Resolve debts with collection agencies

- Prevent bankruptcy or further financial distress

Navigating Common Questions About Debt Consolidation

Will Debt Consolidation Hurt My Credit Score?

This is one of the most common concerns we hear. The short answer: temporarily, perhaps slightly, but in the long run, it often helps.

When you apply for debt consolidation, lenders perform a hard inquiry on your credit report, which may cause a small, temporary dip in your score. However, as you make consistent payments on your new loan and reduce your overall credit utilization, your score typically improves over time.

According to data from the Consumer Financial Protection Bureau, consumers who successfully complete debt consolidation programs often see credit score improvements of 60-100 points by the program’s end.

What’s the Real Difference Between Debt Consolidation and Debt Settlement?

This distinction is crucial to understand:

- Debt Consolidation: You’re combining and fully repaying all your debts, just under better terms. Your creditors receive 100% of what you owe.

- Debt Settlement: You (or a company representing you) negotiate to pay less than the full amount owed, often in a lump sum. While this reduces your total debt, it can significantly damage your credit and may have tax implications.

Think of consolidation as refinancing your debt, while settlement is closer to negotiating a discount in exchange for immediate payment.

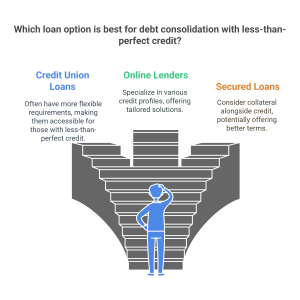

Can I Still Qualify With Less-Than-Perfect Credit?

Yes! While traditional bank loans might require good credit scores (typically 670+), there are options for those with fair or even poor credit:

- Credit union loans often have more flexible requirements

- Online lenders specialize in various credit profiles

- Secured loans (like home equity options) consider your collateral alongside credit

- Debt management plans through nonprofit credit counseling agencies don’t always require credit checks

Ryan, a construction worker with a credit score of 580 after a period of unemployment, found help through a nonprofit credit counseling agency. “The bank turned me down instantly, but the counseling agency worked with my creditors to lower my interest rates and create a payment plan I could actually manage.”

Choosing a Reputable Debt Consolidation Provider

With financial matters, who you work with matters enormously. Look for these green flags:

- Accreditation: Membership in the National Foundation for Credit Counseling (NFCC) or Financial Counseling Association of America (FCAA)

- Transparency: Clear explanation of all fees before you sign anything

- Realistic promises: Be wary of guarantees that sound too good to be true

- Educational resources: The best providers help you learn while helping you consolidate

The Protected Consumer: Understanding Your Rights

Debt consolidation programs in the United States are regulated by federal agencies, including the Federal Trade Commission (FTC) and Consumer Financial Protection Bureau (CFPB), plus state-level oversight. These regulations exist to protect you from predatory practices.

Key protections include:

- Limitations on upfront fees before services are delivered

- Required disclosures about program terms and costs

- Your right to cancel agreements within a specific timeframe

- Protection against deceptive marketing practices

If you’re facing aggressive debt collectors, remember that the Fair Debt Collection Practices Act (FDCPA) prohibits harassment, false statements, and unfair practices. Consolidation programs can often help get these collectors off your back by establishing structured repayment plans.

Creating Your Debt Consolidation Action Plan

Ready to take control of your finances? Here’s your step-by-step roadmap:

- Gather your debt information: List all debts with balances, interest rates, and minimum payments

- Check your credit report: Obtain free reports from annualcreditreport.com

- Calculate your debt-to-income ratio: Divide monthly debt payments by monthly income

- Research options that match your situation: Use the table above as guidance

- Get quotes from multiple providers: Compare interest rates, fees, and terms

- Make your choice and apply: Have documentation ready (proof of income, debt statements)

- Set up automatic payments: Never miss a due date

- Track your progress: Celebrate milestones as your debt decreases

Beyond Consolidation: Building Financial Stability

Debt consolidation is powerful, but it’s most effective when paired with improved financial habits:

- Create and stick to a realistic budget

- Build an emergency fund to avoid future debt for unexpected expenses

- Regularly review your credit report for errors and improvement opportunities

- Consider working with a financial counselor for ongoing guidance

Remember, debt consolidation gives you a fresh start – make the most of it by addressing the root causes of debt accumulation.

Your Next Step Toward Financial Freedom

Debt doesn’t have to define your future. With the right debt consolidation program, you can transform financial stress into financial progress. The key is taking that first step.

Whether you’re a young professional seeking simplified payments, a family looking to optimize your budget, someone preparing for retirement, or rebuilding after financial challenges, there’s a consolidation option designed for your situation.

Ready to breathe easier and build a stronger financial foundation? Start by gathering your debt information and researching options that align with your goals. Your future self will thank you for taking action today.

Have you used debt consolidation to improve your finances? Share your experience in the comments below or reach out for personalized guidance on your debt consolidation journey.