{kind=link}

Are you juggling multiple credit card bills with sky-high interest rates? Do you dread checking the mail because of collection notices? If financial stress is keeping you up at night, you’re not alone. Millions of Americans struggle with debt management, but there’s good news: professional help is available.

The Debt Dilemma: When You Need More Than DIY Solutions

Picture this: Sarah, a working mom of two, found herself drowning in $32,000 of credit card debt spread across six different cards. Between managing her household, working full-time, and trying to save for her children’s education, she simply couldn’t keep track of multiple payment due dates, varying interest rates, and mounting late fees.

“I was making payments, but it felt like throwing money into a black hole,” Sarah recalled. “The balances barely moved because most of my payments were going toward interest.”

Sound familiar? When DIY debt management strategies fall short, it might be time to consider professional help through credit counseling or debt consolidation.

Credit Counseling vs. Debt Consolidation: What’s the Difference?

Understanding the distinction between these two services is crucial for making an informed decision about your financial future.

Credit Counseling: Education and Guidance

Credit counseling typically involves working with a certified professional at a nonprofit agency who will:

- Review your financial situation comprehensively

- Help you create a realistic budget

- Provide educational resources on personal finance

- Potentially negotiate with creditors on your behalf

- Possibly set up a Debt Management Plan (DMP)

The focus here is on education and long-term financial wellness, not just debt elimination.

Debt Consolidation: Simplifying Your Debt

Debt consolidation, on the other hand, involves combining multiple debts into a single payment, usually through:

- A new consolidation loan (often at a lower interest rate)

- Balance transfer to a new credit card with promotional rates

- A structured program that makes payments to your creditors

The primary goal is simplification and potentially reducing interest costs.

| Feature | Credit Counseling | Debt Consolidation |

| Primary Focus | Financial education and budget planning | Combining multiple debts into one payment |

| Typical Provider | Nonprofit agencies | Banks, credit unions, online lenders, specialized firms |

| Cost | Low or no fees for consultation; monthly fees for DMPs ($25-$75) | Loan origination fees (1-8%), possible closing costs, interest charges |

| Credit Score Impact | Minor initial impact; positive long-term if consistent with payments | Initial dip from credit inquiry; positive long-term if payments made consistently |

| Best For | Those needing financial education and budget help | Those with good credit seeking simplification and lower interest rates |

| Time Frame | DMPs typically take 3-5 years | Loan terms are usually 2-7 years |

When to Consider Credit Counseling

Credit counseling might be right for you if:

- You’re overwhelmed by managing multiple payments

- You need help creating a sustainable budget

- You want educational resources on personal finance

- You’re looking for a structured plan with accountability

- Do you prefer working with a nonprofit organization

The National Foundation for Credit Counseling (NFCC) is a reputable resource for finding accredited nonprofit credit counseling agencies.

What Does the Credit Counseling Process Look Like?

- Initial Consultation: A free or low-cost session to review your finances

- Budget Analysis: Identifying where your money goes and potential improvements

- Action Plan Development: Creating a personalized strategy based on your situation

- Possible DMP Setup: If appropriate, establishing a Debt Management Plan

- Ongoing Support: Regular check-ins and educational resources

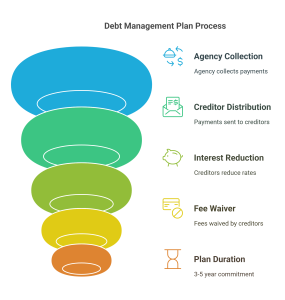

Inside a Debt Management Plan (DMP)

A DMP is a structured repayment program where:

- You make one monthly payment to the counseling agency

- The agency distributes payments to your creditors

- Creditors often reduce interest rates and waive fees

- The plan typically lasts 3-5 years

- Your credit cards are usually closed during the program

Important note: According to the Consumer Financial Protection Bureau (CFPB), enrolling in a DMP might appear on your credit report, but making consistent payments can improve your credit score over time.

When to Consider Debt Consolidation

Debt consolidation might be your best option if:

- You have good credit (typically a score of 670+)

- You qualify for interest rates lower than your current debts

- You’re disciplined enough to avoid accumulating new debt

- You prefer to manage your debt repayment independently

- You want to maintain access to credit

Types of Debt Consolidation Solutions

- Personal Consolidation Loans: Unsecured loans from banks, credit unions, or online lenders specifically for debt consolidation

- Home Equity Loans or Lines of Credit: Using your home’s equity to secure a lower interest rate (but putting your home at risk)

- Balance Transfer Credit Cards: Moving balances to a card with a low introductory rate

- Debt Consolidation Programs: Services that negotiate and manage payments on your behalf

Pro tip: Before choosing a debt consolidation loan, use a loan calculator to ensure the total cost (including fees) actually saves you money compared to your current situation.

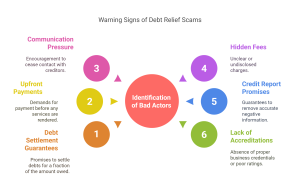

Red Flags: How to Spot Predatory Services

Unfortunately, the debt relief industry attracts some bad actors. Watch out for these warning signs:

- Guarantees to settle your debt for “pennies on the dollar.”

- Demands for upfront payment before any services are provided

- Pressure to stop communicating with your creditors

- Unclear or hidden fees

- Promises to remove accurate negative information from your credit report

- No accreditations or poor ratings with the Better Business Bureau

As the Federal Trade Commission (FTC) advises, if an offer sounds too good to be true, it probably is.

Finding Reputable Help: Your Checklist

When researching credit counseling agencies or debt consolidation firms:

- Verify credentials: Look for certifications from organizations like the NFCC

- Check reviews: Read consumer reviews and check the Better Business Bureau rating

- Understand all fees: Get a clear breakdown of any costs involved

- Confirm nonprofit status: For credit counseling, nonprofit agencies often provide more consumer-friendly services

- Get everything in writing: Don’t rely on verbal promises

- Ask about educational resources: Quality providers offer financial education, not just debt solutions

How Your Credit Score Factors In

Your credit score plays a crucial role in determining which debt relief options are available to you:

- Excellent credit (740+): Best rates on consolidation loans and balance transfers

- Good credit (670-739): Decent consolidation options, potentially at competitive rates

- Fair credit (580-669): Limited consolidation options, higher interest rates

- Poor credit (below 580): May benefit more from credit counseling and DMPs

Remember: Even if your credit score isn’t ideal right now, consistent payments through either approach can help improve it over time.

Beyond the Numbers: The Emotional Side of Debt Relief

Financial stress takes a significant toll on mental health. In fact, a survey by the American Psychological Association found that money is consistently among the top sources of stress for Americans.

When evaluating debt-relief options, consider not just the financial benefits but also:

- Peace of mind from having a structured plan

- Reduced anxiety from fewer monthly payments to track

- Confidence that comes with professional guidance

- Relief from collection calls and notices

- The psychological boost of seeing progress toward debt freedom

Making Your Decision: Key Questions to Ask

Before committing to any service, ask:

- How will this affect my credit score in the short and long term?

- What is the total cost of the program, including all fees?

- How long will it take to become debt-free with this approach?

- What happens if I miss a payment or need to exit the program?

- Which types of debt can be included?

- Are there educational resources to help prevent future debt problems?

Taking the First Step

Reaching out for help with debt can feel intimidating, but it’s a powerful first step toward financial freedom. Remember:

- Most reputable credit counseling agencies offer free initial consultations

- You’re not obligated to enroll in any program after a consultation

- The sooner you address your debt challenges, the more options you’ll have

- Millions of Americans have successfully used these services to overcome debt

Your Action Plan

- Gather your financial information: Collect statements from all your debts, including balances, interest rates, and minimum payments.

- Research providers: Use resources like the NFCC website to find accredited counselors in your area

- Schedule a consultation: Take advantage of free initial sessions to learn about your options.s

- Compare recommendations: If possible, consult with multiple providers to compare advice.

- Make an informed choice: Select the approach that best fits your situation and goal.s

Remember, seeking help with debt management isn’t a sign of failure—it’s a smart strategy for taking control of your financial future.

Ready to Break Free From Debt Stress?

The path to financial freedom starts with a single step. Whether you choose credit counseling or debt consolidation, the important thing is to begin moving forward with a plan.

Have you had experience with credit counseling or debt consolidation? Share your story in the comments below to help others on their journey to financial wellness.