{kind=link}

KeyTake Away

- Bankruptcy offers legal protection from creditors and halts most collection actions, allowing for liquidation (Chapter 7) or reorganization (Chapter 13).

- The Means Test decides Chapter 7 eligibility by comparing six-month average income to state medians, and subtracting certain allowable expenses.

- Bankruptcy filings are public records but typically require specific searches; certain professions, particularly those needing security clearances and credit checks, may scrutinize financial history.

- Though a filing remains on credit reports for years, disciplined budgeting, punctual payments, and responsible credit usage can rebuild financial stability over time, opening the door to improved loan terms, renewed financial confidence, and greater security.

Declaring bankruptcy can be a daunting prospect, yet it remains a valid way for individuals to manage overwhelming debt under the protection of the legal system. Once you file, a court-ordered automatic stay halts most collection efforts, giving you time to review your finances and allowing creditors to receive repayment in an orderly manner—if funds are available. While bankruptcy may drastically affect your credit score and financial standing, it can also offer the fresh start many people desperately need. This guide explores how bankruptcies work, what to consider before filing, types of personal bankruptcy, the filing steps, how to rebuild your credit, and the implications for your privacy and employment.

How Bankruptcies Work

When you declare bankruptcy, you ask a federal bankruptcy court to intervene between you and your creditors. This intervention, called filing a bankruptcy petition, triggers an automatic stay stopping creditor actions like wage garnishments and repossessions. A court-appointed trustee manages the process—either asset liquidation in Chapter 7 or repayment in Chapter 13.

Before Filing for Bankruptcy Before deciding on bankruptcy, assess your income, debts, and repayment capacity. Consider credit counseling—a required step in many jurisdictions—and alternatives like debt management plans, consolidation, or creditor negotiation.

Before Filing for Bankruptcy

Before deciding on bankruptcy, it is important to conduct an honest assessment of your financial situation. Calculate your monthly income, tally all debts, and compare the total to what you can realistically repay. Many people seek out credit counseling before filing, as some jurisdictions even require an approved counseling course. This service provides an overview of your finances, identifies potential alternatives, and ensures you fully understand the implications of bankruptcy.

Alternatives worth exploring include debt management plans, debt consolidation, and negotiations with creditors. Under a debt management plan, for example, you make one monthly payment to a credit counseling agency, which then distributes the money to creditors, often at reduced interest rates. Although these strategies can be time-consuming, they may preserve your credit score more effectively and help you avoid the legal complexities of bankruptcy.

Types of Personal Bankruptcy

Below is an expanded overview of the two main types of personal bankruptcy—Chapter 7 (liquidation) and Chapter 13 (reorganization). This will provide more context on eligibility requirements, the filing process, possible outcomes, and how each option can affect your finances and assets.

Chapter 7 Bankruptcy (Liquidation)

- Overview:

- Often called “liquidation bankruptcy,” Chapter 7 is typically used by individuals (and businesses) with limited disposable income.

- Its primary aim is to give filers a fresh start by discharging most unsecured debts, such as credit card bills, medical expenses, and personal loans.

- Qualification and Means Test:

- To qualify, most people must pass what is called a “means test,” which compares their household income to the median income in their state. If your income is below the median—or if, after certain allowable expenses, you have little to no disposable income—you are more likely to be eligible.

- Some higher-income earners may not be able to file under Chapter 7 and might need to consider Chapter 13 instead.

- Role of the Trustee and Asset Liquidation:

- After filing, the court appoints a trustee responsible for reviewing your finances and assets.

- The trustee has the power to sell (or “liquidate”) certain non-exempt property to pay off part of your debt. Exemptions vary by state, but often include essential items like a primary home (up to a certain equity limit), a modest car, clothing, and other basic household goods.

- Non-exempt assets might include items such as a second vehicle, high-value collectibles, or substantial bank account balances above exemption limits.

- Discharge of Debts:

- Typically, most unsecured debts are wiped out in Chapter 7. Exceptions may include certain taxes, student loans (except in rare hardship cases), alimony, and child support obligations.

- Once the process is complete (often taking three to six months), creditors can no longer pursue you for those discharged debts.

- Credit Impact and Future Financial Life:

- A Chapter 7 bankruptcy filing stays on your credit report for up to 10 years.

- While it may lower your credit score initially, many people are able to begin rebuilding credit by using secured credit cards, small credit-builder loans, or on-time rent and utility payments reported to the credit bureaus.

Chapter 13 Bankruptcy (Reorganization)

- Overview:

- Chapter 13 is often chosen by individuals who have a reliable stream of income and want to retain valuable assets—such as a home—from foreclosure.

- Instead of liquidating property, you propose a court-approved repayment plan that generally spans three to five years.

- Repayment Plan Structure:

- Under this plan, you make monthly payments to a trustee who then distributes funds to creditors based on the plan’s terms.

- The amount you pay each month depends on your income, expenses, and types of debt. Priority debts (e.g., certain taxes, alimony, child support) must typically be paid in full, while unsecured debts can receive partial payment.

- Protecting Your Home and Other Assets:

- Chapter 13 can allow you to catch up on past-due mortgage or car payments. As long as you stay current with the plan’s payments, you can prevent or stop foreclosure or repossession.

- This is one of the main reasons people choose Chapter 13 over Chapter 7—especially when they have significant home equity or other property they want to keep.

- Discharge of Remaining Unsecured Debts:

- After successfully completing the repayment plan, any remaining eligible unsecured debts may be discharged.

- This means you won’t owe anything further on credit card balances, medical bills, or certain other unsecured obligations included in the plan (though some debts, like recent taxes, student loans, and support obligations, remain non-dischargeable).

- Timeline and Credit Impact:

- A Chapter 13 bankruptcy remains on your credit report for up to 7 years from the filing date—typically a shorter duration than Chapter 7.

- During the repayment period, you must make all required payments on time. Missing payments can lead to dismissal of the case or conversion to a Chapter 7, depending on the situation.

- As with Chapter 7, rebuilding credit is possible. Many individuals find that successfully completing a Chapter 13 repayment plan demonstrates responsible financial behavior, which can help in future loan applications.

Choosing the Right Option

- When Chapter 7 Makes Sense: If you have limited income or your income is primarily consumed by living expenses, you may not be able to fund a repayment plan. Chapter 7 offers a fresh start relatively quickly, albeit with the risk of losing non-exempt assets.

- When Chapter 13 Makes Sense: If you have sufficient and stable income, want to keep assets (like your home), and need time to catch up on arrears, Chapter 13’s structured repayment plan could be the better option.

Deciding between Chapter 7 and Chapter 13 often comes down to your financial goals, your asset situation, and your ability to meet a repayment plan. Consulting with a qualified bankruptcy attorney or financial counselor can help you evaluate your circumstances and choose the best path forward.

Table 1: Comparison of Chapter 7 and Chapter 13

| Criteria | Chapter 7 | Chapter 13 |

| Income Requirement | Must pass the Means Test | Must have regular income |

| Process Duration | Around 3–6 months | 3–5 years (repayment plan) |

| Asset Handling | Certain non-exempt assets sold | Typically retain most assets |

| Discharge of Debt | Most unsecured debts fully discharged | Remaining eligible debts discharged upon plan completion |

| Impact on Credit | Stays on record for up to 10 years | Stays on record for up to 7 years |

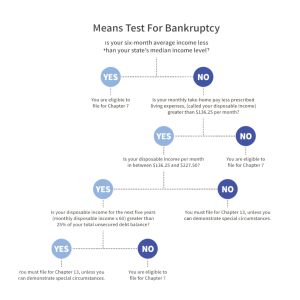

Means Test for Chapter 7

The Means Test determines whether your income is sufficiently low to qualify for Chapter 7. First, your average monthly income (usually measured over six months) is compared to the median income for a similarly sized household in your state. If your income is below the median, you generally qualify immediately. If it is above, you proceed to a second step where you subtract allowable expenses—such as housing, utilities, and necessary transportation costs—to calculate your disposable income. A lower disposable income indicates Chapter 7 eligibility; a higher figure might necessitate Chapter 13 instead.

Steps in Filing for Bankruptcy

Filing for bankruptcy typically involves several key steps:

- Gather Financial Records: Compile bank statements, tax returns, pay stubs, and all debt information.

- Complete Mandatory Counseling: Provide a certificate of completion from an approved credit counseling provider.

- Submit the Bankruptcy Petition: File the necessary documents and pay the applicable fees to the bankruptcy court.

- Automatic Stay Begins: Creditors must cease collection activities immediately upon filing.

- Trustee and 341 Meeting: A trustee is appointed to handle your case, and you attend a Meeting of Creditors to discuss your situation.

- Asset Liquidation or Payment Plan: In Chapter 7, non-exempt assets may be liquidated; in Chapter 13, you follow a court-approved repayment plan.

- Discharge: Once requirements are met, the court issues a discharge for eligible debts, effectively erasing your legal obligation to pay them.

Rebuilding Your Credit

Bankruptcy isn’t a permanent setback. Rebuild with consistent budgeting, on-time payments, secured cards, and credit repair steps after bankruptcy. Monitor credit reports and set realistic financial goals.

Some individuals opt for secured credit cards, which require a cash deposit but allow you to demonstrate consistent repayment behavior. Over time, these positive payment histories can help lift your credit score. Checking credit reports regularly to spot any errors or inaccuracies is also advisable. When combined with prudent financial planning and savings, these steps can accelerate your journey toward re-establishing a solid credit profile.

Are Bankruptcy Filings Publicly Available?

Many people worry that declaring bankruptcy will expose their private financial affairs to the world. Indeed, bankruptcy filings become part of the public record, meaning they can be accessed by anyone willing to search federal court records or use online portals such as the Public Access to Court Electronic Records (PACER) system. However, while technically public, these records are not broadcast widely and usually require some effort to locate.

Table 2: Privacy Concerns and Accessibility of Bankruptcy Filings

| Concern | Reality |

| Public Disclosure | Filings are public but not automatically circulated; they require intentional searches. |

| Personal Details | Documents list assets, debts, and some personal info, but sensitive data (e.g., SSN) is partially redacted. |

| Impact on Personal Reputation | Most people rarely check bankruptcy databases unless they have a specific reason to. |

If privacy is a high priority, be aware that any court proceeding—bankruptcy included—carries some level of public disclosure. Nonetheless, widespread visibility is uncommon unless you are in a particularly high-profile position or legal matter.

Will Bankruptcy Affect My Job or Future Employment?

Bankruptcy can raise concerns about professional repercussions. Employers rarely terminate employees solely due to a personal bankruptcy filing; however, certain professions, especially those requiring security clearances or handling large sums of money, may have stricter policies regarding financial history. Future employers might also review credit reports as part of a standard background check. Although a bankruptcy entry may raise questions, it does not necessarily bar you from employment, especially if you are transparent about your situation and demonstrate financial responsibility going forward.

In practice, companies differ widely in how they interpret bankruptcies during hiring. Some may regard the filing as a sign that you are taking responsible steps to manage debt, while others could see it as a risk factor. If you are concerned about your job, review your employment contract or speak with a legal professional to clarify your rights.

FAQs

- Can I Keep My Home If I File for Bankruptcy?

You may retain your home in Chapter 7 if the equity does not exceed state or federal exemption limits. In Chapter 13, you can catch up on missed mortgage payments through your repayment plan and typically avoid foreclosure. - Which Debts Are Ineligible for Discharge?

Generally, alimony, child support, recent tax debts, court fines, and most student loans cannot be discharged. Each jurisdiction has its own specific rules, so consult an attorney for detailed guidance. - How Long Does Bankruptcy Stay on My Credit Report?

Chapter 7 appears for up to 10 years, while Chapter 13 may remain for up to 7 years. Over time, consistent on-time payments can mitigate the impact of the filing. - Does Filing for Bankruptcy Stop Lawsuits and Wage Garnishments?

Yes. The automatic stay should halt most lawsuits, wage garnishments, and collection calls immediately after your case is filed. Creditors must seek court permission to resume collection efforts. - Can I File for Bankruptcy Again in the Future?

In most jurisdictions, you can file multiple bankruptcies, but waiting periods exist between discharges.

Yes, with time limits. Learn more about repeat filings.

The Bottom Line

Bankruptcy exists to offer individuals relief from crushing debt and a chance to rebuild their financial lives. While it has substantial consequences—such as a lasting mark on your credit report, public availability of your filing, and the possibility of extra scrutiny from certain employers—it can be an essential lifeline for those who have exhausted all other options. By thoroughly assessing your finances, exploring alternatives, and understanding how the process affects your privacy and professional standing, you can decide if filing for bankruptcy is the most constructive path forward.

Remember that life after bankruptcy can involve slow but steady credit repair through responsible spending, punctual bill payments, and continuous monitoring of your financial progress. When approached with careful planning and diligence, bankruptcy can serve as a turning point toward a more stable and secure financial future.