{kind=link}

Key Take Away

- Paying off credit cards or personal loans with double-digit APR usually offers the best immediate “return.

- If your debt’s interest rate is lower than your expected investment return, consider investing instead of rushing to pay off that debt.

- Contribute at least enough to your 401(k) to get any employer match—don’t leave that on the table.

- Factor in peace of mind; it can outweigh purely mathematical considerations for some individuals.

- Keep 3–6 months of expenses in liquid savings to avoid slipping back into debt if emergencies arise.

- Reassess as interest rates and life circumstances change to align your finances with your goals.

Introduction

When it comes to personal finance, one of the most debated questions is whether you should prioritize investing any extra cash you have or paying off existing debt. Both strategies have significant implications for your financial health and long-term wealth-building potential. Making the right choice depends on interest rates, investment returns, risk tolerance, time horizon, and personal goals.

According to various data sources, Americans have different types of debt, from credit cards and student loans to mortgages and car loans. As per the Federal Reserve’s Survey of Consumer Finances, the median debt among U.S. families stood at around $55,300 in 2019 (the latest comprehensive dataset available). Meanwhile, investment opportunities such as stocks, bonds, mutual funds, and retirement accounts have historically shown varying returns, with the S&P 500 averaging about a 10% annual return over the long run (though it can fluctuate significantly from year to year).

Given these facts, there is no one-size-fits-all answer to whether you should invest or pay off debt first. This article will explore deciding which strategy is best for your situation, provide data-driven insights on interest rates vs. expected returns, and discuss practical scenarios to help you balance debt reduction and wealth creation.

1. Understanding the Basics: Debt vs. Investing

- Debt

Debt is any borrowed money you are obligated to repay, typically with interest. Typical forms of debt include credit card balances, mortgages, student loans, and auto loans. The interest rate on these loans directly affects how much you pay over time. For instance, a high-interest credit card at 20% APR can quickly balloon your balance, making it expensive to carry over any monthly outstanding amount. - Investing

Investing involves putting money into financial vehicles—such as stocks, bonds, mutual funds, or even real estate—with the expectation of earning returns over time. While the U.S. stock market, for example, has delivered long-term average returns of about 10% annually (S&P 500 historical average), actual returns vary year to year and carry inherent risks.

When deciding between paying off debt and investing, the basic principle is to compare the cost of your debt to the potential returns on your investments. However, behavioral factors, tax considerations, and liquidity needs also play critical roles.

2. High-Interest vs. Low-Interest Debt

Debt is not created equal. The decision often hinges on the type of debt you carry:

High-Interest Debt:

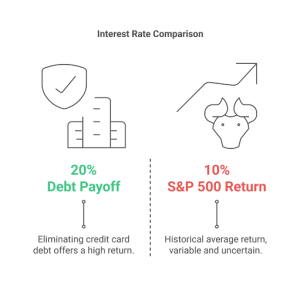

Credit cards and certain personal loans can charge double-digit interest rates. For example, data from the Federal Reserve indicates that the average credit card interest rate in the U.S. surpassed 20% APR in 2023. Paying down high-interest debt typically offers a guaranteed “return” equal to the interest rate you would otherwise pay. If you pay off a credit card charging 20%, it’s akin to earning a risk-free 20% on your money, which is extremely difficult to beat with most traditional investments.

Low-Interest Debt:

Mortgages, federal student loans, or auto loans often carry lower rates. For example, a 30-year fixed mortgage (depending on credit score, market conditions, etc.) could hover around 6–7% APR, while federal student loans might range from 4–6%. In these cases, understanding the payoff amount is crucial as the interest rate might be competitive with, or even lower than, potential long-term investment returns—especially if you have a diversified portfolio or contribute to a tax-advantaged retirement account.

3. The Mathematical Perspective

From a purely mathematical standpoint, the decision can be boiled down to an interest-rate comparison:

- If your debt interest rate is higher than your expected investment return, paying off debt first may yield a better net result.

- If the interest rate on your debt is lower than or comparable to your expected investment return, you might consider investing, especially in tax-advantaged accounts (e.g., 401(k), IRA).

For instance, if you pay 6% on your mortgage but can invest in a diversified portfolio that you expect (though not guaranteed) to return 8% annually, the difference (8% – 6% = 2%) could be your net benefit by investing. However, this is an oversimplification because investment returns are not guaranteed, and risk must be accounted for.

4. Risk Tolerance and Emotional Factors

Even if the math suggests investing, many people prefer the peace of mind of being debt-free. For instance, a 2022 Northwestern Mutual survey found that many Americans experience financial stress due to outstanding debts, affecting their mental well-being and confidence.

- Risk Tolerance: Some individuals have a high capacity for handling fluctuations in the stock market or other investments. Others are more risk-averse. If debt makes you anxious or disrupts your lifestyle, paying it off can provide a psychological return that surpasses purely financial metrics.

- Personal Goals: If you’re striving for financial independence, retiring early, or simplifying your finances, carrying unnecessary debt may be counterproductive. Conversely, leveraging low-interest debt to invest might be viable if you have a well-structured, long-term plan and comfortable cash flow.

5. Tax Considerations

Taxes can tilt the scales when deciding whether to invest or pay off debt. Some debts and investments come with tax implications:

- Mortgage Interest Deduction

If you itemize deductions, you can often deduct the interest on mortgages (up to certain limits) for primary residences. This effectively lowers the actual cost of the mortgage interest, making it less “expensive” to carry. - Retirement Account Advantages

Contributions to 401(k) or traditional IRA accounts may reduce your taxable income, providing an immediate tax benefit. Additionally, the money grows tax-deferred, and if your employer offers a 401(k) match, it’s free. Passing on an employer match to pay off low-interest debt might not be the best financial move. - Student Loan Interest Deduction

If you meet the income requirements, you might be able to deduct up to $2,500 in student loan interest. Although this might not fully offset the interest cost, it is still a factor to consider.

6. Liquidity and Emergency Funds

Another crucial element is liquidity—the ability to access cash in emergencies or unforeseen circumstances. If you pour all your money into paying off debt, you might have limited funds available if you lose your job or face unexpected medical bills. On the other hand, investing without addressing debt can also be risky if the debt payments become overwhelming.

- Emergency Fund Priority: Most financial experts recommend having an emergency fund covering 3-6 months of expenses in a liquid, low-risk account (e.g., a high-yield savings account). This ensures you don’t need to rely on credit cards or withdraw from long-term investments in a crisis.

- Opportunity Cost: By not maintaining enough liquidity, you might resort to high-interest debt if you face a financial shortfall. Balancing debt reduction, investing, and keeping an emergency fund is often the sweet spot.

7. Practical Scenarios

Scenario 1: High-Interest Credit Card Debt

Interest Rate: ~20% or higher

Decision: Pay off debt first

Reasoning: Given that the S&P 500’s historical average return is about 10% annually (and can be lower or negative in bad years), a guaranteed 20% “return” by eliminating credit card debt is generally unbeatable.Scenario 2: Moderate-Interest Student Loans

Interest Rate: ~4–7%

Decision: It depends

Reasoning: If you can invest in a tax-advantaged 401(k) with an employer match, you might opt to at least capture the match. Any excess could then be diverted toward paying down student loans. The emotional aspect—along with your projected returns and job stability—will weigh heavily here.Scenario 3: Low-Interest Mortgage

Interest Rate: ~3–5% (for those who refinanced in prior years) or ~6–7% with newer rates

Decision: Often investing can be more lucrative

Reasoning: If your mortgage interest is relatively low, it might make sense to invest in your IRA or 401(k). However, if your mortgage rate is creeping up (say 6–7%), paying off extra principal might be more attractive—especially if you’re close to retirement and want fewer monthly obligations.Scenario 4: Balancing Debt Payoff & Investing

Interest Rate: Mixed (credit cards, car loans, small personal loan, etc.)

Decision: Use a hybrid approach

Reasoning: You might choose to aggressively target high-interest debts while still contributing at least a minimal amount to retirement plans, especially if an employer match is on the table. A helpful visual approach is shown in this debt payoff diagram.

High-Interest Credit Card Debt

Scenario 2: Moderate-Interest Student Loans

- Interest Rate: ~4-7%

- Decision: It depends

- Reasoning: If you can invest in a tax-advantaged 401(k) with an employer match, you might opt to at least capture the game. Any excess could then be diverted toward paying down student loans. The emotional aspect—along with your projected returns and job stability—will weigh heavily here.

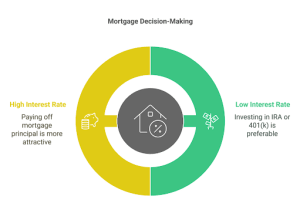

Scenario 3: Low-Interest Mortgage

- Interest Rate: ~3-5% (for those who refinanced in prior years) or ~6-7% with newer rates

- Decision: Often, investing can be more lucrative

- Reasoning: If your mortgage interest is relatively low, investing in your IRA or 401(k) might make sense. However, if your mortgage rate is creeping up (say 6-7%), paying off extra principal might be more attractive—especially if you’re close to retirement and want fewer monthly obligations.

Low-Interest Mortgage

Scenario 4: Balancing Debt Payoff & Investing

- Interest Rate: Mixed (credit cards, car loans, small personal loans, etc.)

- Decision: Use a hybrid approach

- Reasoning: You might aggressively target high-interest debts while contributing at least a minimal amount to retirement plans, especially if an employer match is available.

8. The “Snowball” and “Avalanche” Methods

Two popular strategies for paying off multiple debts simultaneously are:

Debt Snowball

Focus on paying off the smallest balance first to gain momentum and psychological wins. Once the smallest debt is cleared, add that payment amount to the next smallest debt, and so on.Debt Avalanche

Focus on the highest interest rate first for a mathematically optimal approach. Once that debt is cleared, move on to the next highest interest rate.

Both methods can be integrated with an investment plan. For instance, you can follow the avalanche method to tackle high-interest cards while still contributing a set percentage to your 401(k). Once the highest interest debt is eliminated, you can increase your investment contributions. Learn more about this choice in paying off debt vs saving for retirement.

9. Balancing Emotions and Numbers

It’s worth emphasizing the psychological element. Personal finance is not solely about maximizing returns in an ideal mathematical universe. Life is unpredictable, and financial decisions often involve emotions, confidence, and peace of mind.

- Pros of Paying Off Debt: Emotional relief, reduced monthly bills, potential credit score improvement.

- The pros of Investing include the opportunity for compound growth, the ability to take advantage of tax benefits, and the ability to build wealth for the long term.

You might even choose a split approach: invest enough to get your 401(k) employer match (or meet an IRA contribution), then allocate remaining funds to pay off debt more quickly. This approach ensures you don’t miss out on valuable long-term compounding while reducing your debt load.

10. Considering Your Time Horizon

Your investment timeline significantly impacts the final decision:

- Short-Time Horizon (Under 5 Years): If you plan to buy a home, start a business, or make a large purchase soon, you’ll likely prefer less debt and more liquid savings. Investing in volatile assets like stocks may be risky if you need the money soon.

- Long-Time Horizon (10-20+ Years): A longer horizon can help you overcome market fluctuations, potentially making investing more attractive. At the same time, paying off extremely high-interest debt remains a top priority.

11. Retirement Considerations

Failing to invest adequately in retirement can have long-term ramifications. Even if you carry debt, not saving for retirement can be detrimental. Your future Social Security benefits might not be enough to maintain your lifestyle. If your employer offers a matching contribution, you receive an immediate 100% return on the matched portion (up to a limit).

- Minimum Retirement Contributions: If possible, contribute at least enough to capture any employer match. Afterward, analyze your debt situation to decide how much additional money should go toward paying off balances.

- Roth vs. Traditional: Roth IRAs or Roth 401(k)s can be beneficial if you expect to be in a higher tax bracket in retirement, while traditional plans offer an immediate tax benefit.

12. Real-World Example

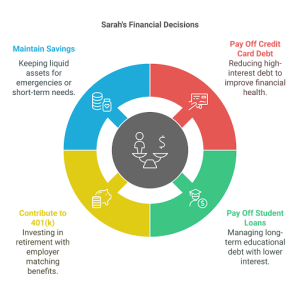

Let’s consider a hypothetical example: Sarah, age 30, earns $60,000 annually and has the following financial obligations and opportunities:

- $5,000 credit card debt at 19% APR

- $20,000 in student loans at 5.5% APR

- Employer 401(k) with a 4% match

- No mortgage (rents an apartment)

- $2,000 in a savings account

Step-by-Step Thought Process:

- Emergency Fund: Sarah should aim to have at least $5,000 to $10,000 in liquid savings to cover 3-6 months of expenses. Currently, she only has $2,000.

- Debt Prioritization: Her credit card interest rate is 19%, which is high. Paying it off is equivalent to a 19% risk-free return. The student loan interest rate is moderate, at 5.5%.

- Employer Match: By contributing 4% of her salary ($2,400 yearly), she gets another $2,400 in free money. Missing out on this match would be a significant opportunity cost.

- Plan:

- Contribute 4% to the 401(k) to capture the full employer match.

- Funnel any available extra cash to eliminate the credit card debt quickly.

- Build the emergency fund to at least $5,000.

- Gradually pay off the student loans while increasing her retirement contribution beyond 4% as debts decrease.

In this scenario, the combination strategy helps Sarah reduce high-interest debt, avoid future credit card reliance by bolstering her emergency fund, and still invest enough to utilize employer matching.

13. Monitoring and Adjusting Your Strategy

A one-time decision isn’t enough. Financial conditions—interest rates, job security, and living situation—change over time. Likewise, the market environment for investments evolves. Review your strategy at least once or twice a year or whenever there’s a significant life event:

- Interest Rate Shifts: If your adjustable-rate debt changes significantly, recalculate your best move.

- Life Changes: Marriage, divorce, having children, or changing careers can affect your risk tolerance and budget.

- Market Performance: While you shouldn’t chase returns, significant market changes might prompt you to rebalance your portfolio or reevaluate how aggressively you pay off debt.

14. Professional Guidance

Consulting with a financial planner or advisor can provide a tailored assessment based on your unique situation. Advisors can incorporate factors such as tax brackets, future earnings potential, paying off debt vs. saving for retirement, and insurance needs into a holistic plan. Sometimes, an hour or two of professional advice can save thousands of dollars or help you gain clarity and confidence.

Conclusion

It’s worth emphasizing the psychological element. Personal finance is not solely about maximizing returns in an ideal mathematical universe. Life is unpredictable, and financial decisions often involve emotions, confidence, and peace of mind.

Pros of Paying Off Debt: Emotional relief, reduced monthly bills, potential credit score improvement.

Pros of Investing: Opportunity for compound growth, taking advantage of tax benefits, building wealth for the long term.

You might even choose a split approach: invest enough to get your 401(k) employer match (or meet an IRA contribution), then allocate remaining funds to pay off debt more quickly. This approach ensures you don’t miss out on valuable long-term compounding while still reducing your debt load.