{kind=link}

Key Takeaway :

Yes, debt reduction is a good idea, but the right approach depends on your financial situation. Reducing debt lowers financial stress, improves credit scores, and saves money on interest. High-interest debt, like credit cards, should be paid off quickly, while low-interest debt, such as mortgages, may not need immediate repayment.

Debt relief strategies include consolidation, credit counseling, management plans, settlement, and forgiveness. While some options impact credit scores, others help create manageable repayment plans. A balanced approach—paying off high-interest debt while saving and investing—ensures financial stability and long-term security. Choosing the right method depends on individual goals and circumstances.

Debt reduction can be a beneficial financial strategy, but whether it is the right choice depends on an individual’s financial situation. Reducing debt can lead to lower stress levels, improved credit scores, and greater financial flexibility. However, it is important to consider the following factors:

- Debt Type: High-interest debt, Such as credit card debt, should be reduced as quickly as possible. Low-interest debt, such as mortgages or student loans, may not need to be prioritized as aggressively.

- Financial Stability: Those with a steady income and an emergency fund may benefit more from a balanced approach to paying down debt and saving for retirement.

- Long-Term Goals: A strategic debt reduction plan can improve financial prospects if you aim for homeownership, investment opportunities, or retirement planning.

How Debt Relief Works

Debt relief is a strategy designed to help individuals reduce or eliminate their outstanding debts through various financial programs or negotiations. It can involve consolidating multiple debts into one manageable payment, negotiating with creditors for lower interest rates, or even settling debts for less than what is owed. The right debt consolidation app or program depends on your financial situation, credit score, and long-term goals.

One common dilemma people face when tackling debt is deciding between paying off debt vs saving for retirement or whether to pay off debt or invest. The right choice depends on factors like interest rates, employer retirement contributions, and financial stability. High-interest debt, such as credit cards, is usually best paid off first, while low-interest debt (e.g., mortgages) may allow more flexibility for investing.

Types of Debt Relief

1. Debt Consolidation

Debt consolidation combines multiple debts into one loan or credit account, often with a lower interest rate. This simplifies payments and can make debt Debt manageable. Common methods include:

- Personal loans – Using a loan to pay off multiple high-interest debts.

- Balance transfer credit cards – Transferring debt Debt card with a 0% introductory APR.

- Home equity loans or HELOCs – Using home equity to pay off debt.

2. Credit Counseling

Nonprofit credit counseling agencies help consumers understand their debt and create a personalized plan to repay it. They offer budgeting assistance and financial education and sometimes recommend debt management plans (DMPs).

3. Debt Management

A Debt Management Plan (DMP) is an agreement between you and your creditors, typically facilitated by a credit counseling agency. It often includes:

- Reduced interest rates

- Waived fees

- A structured repayment plan (usually 3–5 years)

Unlike debt settlement, a DMP requires you to pay the full amount owed under better terms.

4. Debt Settlement

Debt settlement companies negotiate with creditors to reduce the total amount owed, often by offering a lump sum payment. However, it can significantly impact your credit score and involve high fees. Typical providers include Freedom Financial and Resolve.

5. Debt Forgiveness

Debt forgiveness occurs when a lender agrees to cancel part or all of your debt. Debts are rare but may apply in cases such as:

- Student loan forgiveness programs

- Credit card or medical debt forgiveness (usually through settlements)

What to Know Before You Apply for Debt Relief

1. Watch Out for Scams

- Beware of companies that charge upfront fees before providing relief.

- Avoid promises of instant debt elimination—legitimate programs take time.

- Verify credentials with the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA).

2. Interest Rates

- Some programs lower interest rates (e.g., debt management plans).

- Others, like settlement programs, may not reduce interest and could lead to additional penalties.

Interest Rates

3. Fees

- Debt settlement fees range from 15% to 25% of the settled amount.

- Credit counseling agencies may charge small monthly fees.

- Debt consolidation loans may have origination fees.

4. Tax Implications

Forgiven debt De, but $600 is considered taxable income by the IRS unless you qualify for insolvency exemption.

5. Program Length

- Debt management plans: 3–5 years

- Debt settlement: 2–4 years

- Debt consolidation: Depends on the loan term (usually 2–7 years)

Our Picks for Debt Relief Options

Debt Settlement

- Freedom Financial (Website) – Helps negotiate settlements and reduce total debt Debt.

- Resolve (Website) – A digital platform that provides debt resolution tools and connects users with settlement solutions.

- National Debt Relief (Website) – Specializes negotiating with creditors to reduce overall debt amounts.

Debt Consolidation Balance Transfer

- U.S. Bank Visa® Platinum Card (Website): This card offers a long 0% intro APR period for balance transfers, helping reduce interest on existing credit card debt.

- Discover it® Balance Transfer (Website) – Provides a long introductory APR period with cashback rewards.

- Citi® Diamond Preferred® Card (Website) – One of the most extended 0% APR balance transfer offers.

Credit Counseling

- GreenPath Financial Wellness (Website) – A nonprofit that provides financial counseling, budgeting advice, and debt management plans.

- Money Management International (MMI) (Website) – Offers financial education and credit counseling services.

- American Consumer Credit Counseling (ACCC) (Website) – A nonprofit organization that helps consumers develop a structured debt repayment plan.

Paying Off Debt vs Saving for Retirement – What’s the Right Choice?

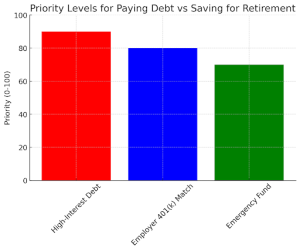

- Priority Levels for Paying Debt vs Saving for Retirement

- High-interest debt (e.g., credit cards) is the highest priority, meaning it should typically be paid off first.

- Employer 401(k) Match is a strong priority, as taking advantage of employer-matched contributions is essential “fr” e-money.

- E”emergency Fund is also a key factor, as having 3–6 months of savings ensures financial security.

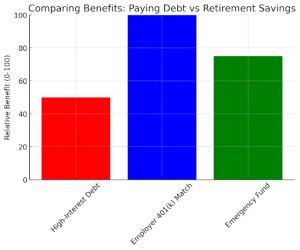

- Comparing Benefits: Paying Debt vs Retirement Savings

- Employer 401(k) Match offers the highest benefit because of the compound interest and employer contribution.

- Emergency Fund also ranks high, as it prevents future debt accumulation.

- High-interest debt debt is still a primary focus, as paying it off saves significant interest costs.

A balanced approach—paying down high-interest debt, contributing enough to get an employer’ s1 (k) match, and building an emergency fund—can be the best long-term financial strategy.

Should You Pay Off Debt or Invest?

The decision to pay off debt or invest depends on the expected returns of an investment versus the cost of your debt. Some key considerations:

If your debt carries an interest rate higher than potential investment returns, it’s often better to pay it off first.

If you have low-interest debt (e.g., student loans or mortgages), investing in index funds, retirement accounts, or stocks may provide better long-term growth.

If you lack an emergency fund, prioritizing savings before investing can prevent future debt accumulation.

Ultimately, the best approach depends on individual financial goals, risk tolerance, and debt burden. Consulting a financial advisor can help make an informed decision.

How Does Debt Relief Affect Your Credit?

Debt relief strategies can affect your credit score and overall financial health. Understanding these impacts can help you make informed decisions when choosing the best debt relief option.

Debt Consolidation

- It may slightly lower your credit score initially due to a hard credit inquiry.

- You can improve your credit over time with consistent, on-time payments.

- It helps reduce multiple payments into one, making it easier to manage.

Credit Counseling

- Typically, it does not hurt your credit score.

- Enrolling in a Debt Management Plan (DMP) may require closing some credit accounts, which can temporarily impact your score.

- It helps establish better financial habits and responsible credit use.

Debt Settlement

- It can significantly lower your credit score.

- Missed payments and settled accounts are reported as “pa”d for less than owed,” w,” which lenders consider unfavorable.

- Provides long-term financial relief by reducing the total amount owed.

Debt Forgiveness

- If negotiated through a settlement, it can negatively impact credit due to missed payments.

- It can provide significant financial relief by eliminating a portion of the debt. However, it has tax implications, as forgiven debt is considered taxable income.

Is Debt Reduction a Good Idea?

Yes, debt reduction is a good idea, but it depends on your financial situation and how you approach it. Here are the reasons why:

- Reduces Financial Stress—Excessive debt Can Be overwhelming. Reducing debt can lower stress levels and help you regain control over your finances.

- Saves Money on Interest—High-interest debt, Such as credit card debt, can be expensive over time. Debt reduction strategies like paying off high-interest balances first or negotiating lower rates can save money.

- Improves Financial Stability—Reducing debt frees up more money for essential expenses, savings, and investments, helping you achieve long-term financial security.

- Avoids Extreme Measures Like Bankruptcy—Reducing debt Through negotiation, settlement, or consolidation can prevent the need for more damaging options like bankruptcy, which has long-term credit consequences.

However, debt reduction can have drawbacks if done incorrectly, such as harming your credit score or leading to additional fees. Choosing a strategy that aligns with your financial goals and repayment ability is essential.

Choosing the Best Debt Relief Strategy

Before committing to a debt relief program, assessing how it will affect your financial standing is crucial. One of the primary considerations is the impact on your credit score. Some debt relief options, such as debt settlement or bankruptcy, can significantly lower your credit score, making it challenging to obtain new credit in the future. However, this damage is not always permanent, and with responsible financial behavior, it is possible to rebuild your credit over time. On the other hand, options like debt consolidation may have a lesser impact, especially if payments are made on time.

Another key factor is your financial goals. If your priority is to become debt-free as quickly as possible, you may need to consider more aggressive options, such as debt settlement or bankruptcy. However, if maintaining a good credit score is equally essential, alternatives like debt consolidation or credit counseling may be better. Understanding your long-term financial aspirations will help you determine which strategy best suits your needs while minimizing unnecessary economic hardship.