{kind=link}

Managing debt effectively is crucial for financial stability. If you are overwhelmed with multiple debts, understanding how to deal with debt can help you regain control of your finances. This guide explores debt relief strategies, who should consider them, and key factors to weigh before making a decision.

What Is Debt Relief?

Debt relief refers to various strategies designed to reduce or restructure outstanding debt, making repayment more manageable. These methods aim to lower total debt, consolidate multiple obligations, or modify repayment terms to ease financial burden. Common forms of debt relief include nonprofit debt consolidation, credit counseling, debt management plans (DMPs), and debt settlement.

Debt relief can provide temporary or permanent financial relief, but it is essential to understand the implications before proceeding. Some methods may impact credit scores or involve fees that can add to financial strain if not approached carefully. Be wary of relief advisory agency scams and ensure you are working with reputable professionals.

Debt relief can provide temporary or permanent financial relief, but it is essential to understand the implications before proceeding. Some methods may impact credit scores or involve fees that can add to financial strain if not approached carefully. Be wary of relief advisory agency scams and ensure you work with reputable professionals.

Dealing with Debt Problems: A Professional Guide

Managing debt effectively is crucial for maintaining financial stability. Whether you are struggling with mounting bills or simply want to take control of your finances, a structured approach can make a significant difference. This guide outlines five essential steps to help you deal with debt professionally and systematically.

Step One: Make a List of Everything You Owe

The first step in managing your debt is to gain a clear understanding of your financial obligations. Create a comprehensive list of all your outstanding debts, including:

- Credit card balances

- Personal loans

- Mortgages

- Overdue utility bills

- Student loans

- Any other financial commitments

Record the creditor’s name, the outstanding balance, interest rates, and the due dates for each debt. Having a complete overview of your liabilities will help you make informed decisions about repayment priorities.

Step Two: Prioritize Your Debts

Not all debts are equal; some require immediate attention to prevent severe consequences. Categorize your debts into two groups:

- Priority Debts: These include mortgage or rent payments, utility bills, tax obligations, and any secured loans. Failure to pay these could result in serious repercussions such as eviction, legal action, or utility disconnections.

- Non-priority debts typically include credit cards, store cards, and unsecured loans. While these still need to be paid, they do not carry immediate legal consequences.

By ranking your debts based on urgency and importance, you can allocate your resources more effectively and avoid financial pitfalls.

Step Three: Prioritize Your Debts

A well-structured budget is essential for managing debt. Follow these steps to create a realistic financial plan:

- Calculate Your Income: Include all sources of income, such as salary, bonuses, rental income, and government benefits.

- List Your Essential Expenses: Rent or mortgage, utilities, groceries, transportation, and insurance.

- Determine Your Disposable Income: Subtract your essential expenses from your income to see how much is available for debt repayment.

- Allocate Funds for Debt Repayment: Prioritize payments for priority debts while making minimum payments on non-priority debts.

- Identify Areas to Cut Costs: Look for non-essential expenses that can be reduced or eliminated to free up more funds for debt repayment.

A personal budget clarifies where your money goes and ensures you stay on track with repayments.

Step Four: Seek Independent Advice

Professional advice can provide valuable insights and options if you are struggling to manage your debt. Consider consulting:

- Financial Advisors: Professionals who can offer tailored financial plans and strategies.

- Debt Charities and Nonprofits: Organizations such as the National Debtline or StepChangNonprofitsfree and confidential advice.

- Legal Experts: Consulting a financial attorney may be necessary if you are facing legal action.

Seeking independent advice can help you explore alternative repayment plans, debt consolidation, or even negotiation options with creditors.

Ignoring debt problems will only worsen the situation. Instead, proactively engage with your creditors to discuss your financial difficulties. Many creditors are willing to negotiate new repayment terms, offer lower interest rates, or provide temporary relief options.

When speaking with creditors:

- Be honest about your financial situation.

- Propose a realistic repayment plan based on your budget.

- Request a temporary freeze on interest or late fees if necessary.

- Keep a record of all communications for future reference.

Effective communication can prevent legal actions, reduce financial stress, and create a manageable repayment plan.

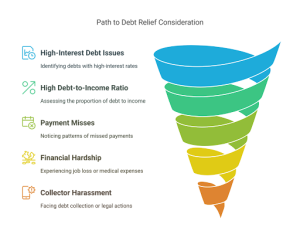

Who Should Consider Debt Relief?

Debt relief is not suitable for everyone, but it can be a viable solution for individuals facing significant financial hardship. You should consider debt relief if:

- You have high-interest debt and struggle to make minimum payments. If your interest rates are exceptionally high, your balance may grow even as you make payments, making it difficult to gain financial traction.

- Your total unsecured debt exceeds 40% of your annual income. A high debt-to-income ratio can indicate financial distress and make qualifying for loans for high credit utilization or credit lines difficult.

- You frequently miss payments or rely on credit cards to cover basic expenses. This could indicate that your income is insufficient to sustain your lifestyle and that your debt is becoming unmanageable.

- You are experiencing a financial hardship such as job loss, medical bills, or a reduced income. Unexpected financial setbacks can make keeping up with debt payments challenging, requiring a structured approach to relief.

- You are being harassed by debt collectors or facing legal action due to unpaid debts. If your debt has reached the point of collection or legal threats, taking immediate action through debt relief programs can help prevent further financial damage.

- You need a financial advisor for debt guidance to understand your options and develop a sustainable repayment plan.

If you identify with any of the above situations, exploring debt relief options can be a crucial step toward regaining financial stability.

4 Common Debt Relief Options

1. Debt Consolidation

Debt consolidation involves combining multiple debts into a single loan with a lower interest rate. This simplifies repayment by reducing multiple payments to one fixed monthly amount. For tools and support, check out our consolidate debt app recommendations to streamline your approach.

Pros:

- Lower interest rates reduce the total cost of debt.

- Simplified repayment process with a single monthly payment.

- Can improve credit score over time with consistent payments.

Cons:

- Requires good credit to qualify for favorable rates.

- Extended repayment periods may lead to higher total interest payments.

- Risk of accumulating new debt if spending habits are not controlled.

Debt consolidation is ideal for individuals with multiple high-interest debts who can qualify for a low-interest consolidation loan.

2. Credit Counseling

Credit counseling services provide professional guidance on managing debt and improving financial habits. A certified credit counselor reviews your financial situation and offers personalized advice on budgeting, repayment strategies, and debt relief options.

Pros:

- Provides expert financial guidance.

- Helps create a structured debt repayment plan.

- Often includes free or low-cost educational resources.

Cons:

- Does not reduce the amount of debt owed.

- Limited effectiveness for individuals with severe financial hardship.

Credit counseling suits individuals seeking professional financial advice and structured repayment plans.

3. Debt Management Plans (DMPs)

A Debt Management Plan (DMP) is a structured repayment program facilitated by credit counseling agencies. These plans negotiate lower interest rates and consolidate payments into one manageable monthly amount.

Pros:

- Simplifies repayment with one monthly payment.

- Reduces interest rates and fees.

- Helps avoid bankruptcy.

Cons:

- Requires strict adherence to a repayment schedule.

- Some creditors may not participate in DMPs.

- It may impact credit scores in the short term.

DMPs suit individuals who can commit to a structured repayment plan and want to reduce interest costs.

4. Debt Settlement

Debt settlement involves negotiating with creditors to pay a lump sum less than the total owed. While it can significantly reduce debt, it can also have adverse financial consequences.

Pros:

- Can reduce total debt owed.

- It avoids bankruptcy in severe cases.

Cons:

- May significantly lower credit scores.

- Settled debt may be taxable as income.

- Risk of being scammed by unethical settlement companies such as debt helpers scam.

Debt settlement is best for individuals with substantial financial hardship who cannot repay their entire debt.

Consolidate Debt App

Debt consolidation combines multiple debts into a single loan with a lower interest rate, simplifying payments. Options include:

Debt consolidation loans: Offered by banks and credit unions.

Balance transfer credit cards: Transfer high-interest credit card debt to a card with a lower promotional interest rate.

Home equity loans or lines of credit: Using home equity to consolidate high-interest debts.

Carefully evaluate the terms, fees, and interest rates before consolidating your debt. You can even explore specialized debt consolidation apps that make the process more convenient.

| Company Name | URL | USP (Unique Selling Proposition) |

| Bright Money | Bright Money | AI-driven financial assistant that automates debt repayment and builds credit. |

| Debt Payoff Assistant | Debt Payoff Assistant | Simple and free mobile app for tracking and planning debt payments. |

| Vertex42 | Vertex42 | Provides Excel and Google Sheets templates for financial planning. |

| Unbury.me | Unbury.me | Free online debt calculator using snowball and avalanche repayment methods. |

| Undebt.it | Undebt.it | Customizable debt repayment plans with multiple payoff strategies. |

| ZilchWorks | ZilchWorks | One-time purchase software for debt elimination planning. |

| Qapital | Qapital | Automates savings for debt repayment and financial goals. |

| Debt Payoff Planner | Debt Payoff Planner | A mobile app designed to create and track personalized debt |

3 Things to Consider Before Choosing Debt Relief

1. Impact on Credit Score

Different debt relief methods have varying effects on credit scores. Debt consolidation and management plans may improve credit over time with disciplined payments, while debt settlement and bankruptcy can cause significant drops in credit scores. Assess how each option aligns with your long-term financial goals and ability to rebuild credit.

2. Costs and Fees

Debt relief programs often involve various costs, such as service fees, interest rates, and potential tax implications. Debt settlement companies may charge high fees, while consolidation loans may carry origination charges. Carefully review all associated costs to determine if the benefits outweigh the financial burden of each method.

3. Long-Term Financial Impact

Consider how the debt relief method will shape your long-term financial future. While some options provide immediate relief, they may lead to extended repayment terms, increased interest costs, or difficulty obtaining credit in the future. Should I limit myself to a daily budget? Developing disciplined spending habits can prevent future financial strain.

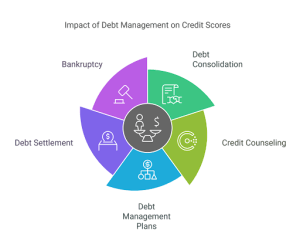

Does Debt Relief Affect Your Credit?

Yes, debt relief can impact your credit score in different ways:

- Debt Consolidation: Credit can be improved over time if payments are made consistently and on time. However, taking on a new loan may initially cause a slight dip in your credit score due to the hard inquiry from lenders.

- Credit Counseling has a minimal direct impact on credit scores, but enrolling in a credit counseling program may be noted on your credit report, which some lenders may consider when evaluating creditworthiness.

- Debt Management Plans Can temporarily lower credit scores, as creditors may close or adjust accounts. However, making timely payments under a DMP can ultimately improve credit health.

- Debt Settlement: This can significantly damage credit scores due to delinquent payments before settlements are reached.

- Bankruptcy: Has the most severe impact on credit, remaining on reports for 7-10 years and drastically reducing credit scores.

Relief Affects Your Credit

Take Charge of Your Finances

Debt relief can be a powerful tool for managing financial challenges, but it requires careful consideration. Evaluate your financial situation, research available options, and seek professional advice if needed.

If you are struggling with debt, consider speaking with a certified credit counselor or financial advisor to determine the best course of action for your situation. Additionally, stay informed about U.S. government debt interest, total national debt, and whether U.S. debt matters to understand broader financial impacts.

For specialized programs like Washington debt relief or veteran debt assistance reviews, explore government-backed and non-profit resources tailored to your needs.

How to avoid debt in the future? Making smart financial choices and planning ahead can help you achieve long-term financial security.

For specialized programs like Washington debt relief or veteran debt assistance reviews, explore government-backed and nonprofit resources tailored to your needs.

How to avoid debt? Making financial choices and planning can help you achieve long-term financial security.