{kind=link}

What Is the Best Budgeting Tactic for Paying Off Debt?

You’re staring at your credit card statements, loan notifications, and that growing pile of bills. Trust me, we’ve all been there. Debt can feel like quicksand – the harder you try to escape, the deeper you sink. But here’s the truth: the right budgeting tactic can transform your financial situation faster than you might think.

The Debt-Crushing Toolkit: Finding Your Perfect Match

The “best” budgeting tactic isn’t universal – it’s the one that works with your income, psychology, and specific debt situation. Let’s break down your options so you can find your financial wingman.

The Debt Snowball Method: Small Wins, Big Momentum

The debt snowball isn’t just popular because Dave Ramsey talks about it – it’s because it hacks your brain’s reward system.

Here’s how it works: You list all your debts from smallest balance to largest. Pay minimum payments on everything except the smallest debt, which gets every extra dollar you can throw at it. Once that’s gone, roll that payment into attacking the next debt on your list.

Why it works: You’ll knock out smaller debts quickly, creating wins that keep you motivated. Those quick victories feed your determination when tackling bigger balances.

Perfect for: Anyone who needs psychological wins to stay in the game. If you’ve tried budgeting before and quit because it felt like nothing was happening, this method gives you those “hell yeah” moments that keep you going.

The Debt Avalanche Method: Math-Driven Debt Destruction

If you’re the spreadsheet type who values efficiency over everything, the avalanche method is your cheat code to savings.

The approach: Arrange your debts by interest rate, highest to lowest. Minimum payments everywhere except that high-interest beast, which gets all your extra cash. Once it’s dead, move to the next highest rate.

Why it works: You’ll save more money overall and get out of debt faster mathematically. The numbers don’t lie – this approach minimizes interest payments.

Perfect for: The financially disciplined who don’t need quick wins to stay motivated. You’re playing the long game and want the most efficient path to freedom.

The Balance Transfer Strategy: The Interest Rate Hack

Credit card debt crushing your soul? A balance transfer might be your secret weapon.

The method: Transfer high-interest debt to a new card offering a low or 0% introductory APR. Then attack that balance aggressively during the promotional period.

Why it works: Every dollar goes toward principal instead of feeding the interest monster. Some cards offer 12–18 months interest-free, giving you a clear runway to make serious progress.

Perfect for: Those with good credit and primarily high-interest credit card debt. It’s not a solution on its own but a powerful tool within your larger strategy. Consider a consolidate debt app to manage it effectively.

Why it works: Every dollar goes toward principal instead of feeding the interest monster. Some cards offer 12-18 months interest-free, giving you a clear runway to make serious progress.

Perfect for: Those with good credit and primarily high-interest credit card debt. It’s not a solution on its own but a powerful tool within your larger strategy.

The Side Hustle Accelerator: Income Boosting

Sometimes the issue isn’t your spending plan – it’s your income.

The approach: Take on a temporary side gig with the sole purpose of debt elimination. Every dollar earned goes straight to debt payoff, supercharging your primary budgeting method.

Why it works: You’re not just rearranging financial deck chairs – you’re bringing additional firepower to the battle. Even an extra $400-500 monthly can slash years off your debt timeline.

Perfect for: Anyone with available time and energy who wants to speed up their debt-free timeline. Especially powerful when combined with snowball or avalanche methods.

Creating Your Custom Debt-Crushing Budget

Now that you understand the major strategies, let’s build a framework that makes them sustainable.

Step 1: Map Your Debt Landscape

You can’t navigate without knowing the terrain. Create a complete debt inventory:

| Debt Type | Total Balance | Interest Rate | Minimum Payment |

| Credit Card A | $4,300 | 19.99% | $129 |

| Student Loan | $18,500 | 5.8% | $210 |

| Car Loan | $9,800 | 6.9% | $375 |

| Personal Loan | $2,100 | 11.5% | $106 |

This gives you clear targets and helps determine whether snowball (focus on the Personal Loan first) or avalanche (attack Credit Card A first) makes more sense for your situation. For visualization, refer to a debt payoff diagram.

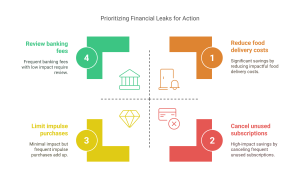

Step 2: Find Your “Dead Money”

Most budgets leak cash without you noticing. Track your spending for 30 days, categorize everything, then look for these common cash drains:

- Subscription services you rarely use

- Food delivery markups and fees

- Impulse purchases under $20 (they add up)

- Banking fees and financial service charges

- Auto-renewed memberships

Redirecting even $200 monthly from these categories to debt payment accelerates your progress dramatically.

Step 3: Build Your Debt-Focused Budget

A budget that prioritizes debt elimination looks different from a regular budget. The key allocation principle:

- Essential expenses (housing, basic food, utilities, transportation to work)

- Minimum debt payments

- Aggressive payment toward target debt

- Everything else

Notice what’s missing? Savings beyond a mini emergency fund of $1,000 can actually wait until high-interest debt is gone. Your 22% credit card is effectively earning you a 22% guaranteed return when you pay it down – far better than most investments. Consider the logic in paying off debt vs. saving for retirement.

Step 4: Protect Your Plan With Guardrails

Debt repayment fails when life happens. Build these protections:

- A small emergency fund ($1,000-2,000) to prevent new debt

- A “stuff happens” category in your budget ($50-100/month)

- A realistic “social/fun” allocation (extreme restriction leads to budget rebellion)

- Weekly check-ins to adjust course (10 minutes each Sunday night)

Breaking Down Specific Debt Types

Different debts require customized approaches. Let’s dig into the most common types:

Credit Card Debt: The Ultimate Priority

With average interest rates between 18–24%, credit cards are financial napalm. Your strategy:

- Stop the bleeding (put the cards on ice)

- Consider balance transfers for breathing room

- Pay more than the minimum – much more

- Contact creditors about hardship programs if you’re struggling

Student Loan Strategy: Playing the Long Game

Student loans typically have lower interest rates but high balances. Your approach:

- Explore income-driven repayment plans if struggling

- Consider refinancing if you have stable income and good credit

- Target private loans before federal (federal loans have more protections)

- Look into profession-based forgiveness programs

Remember that student loans are often “good debt” with reasonable rates – prioritize higher-interest debt first unless you’re pursuing Public Service Loan Forgiveness.

Mortgage Mastery: The Housing Hack

Mortgages typically have the lowest interest rates among major debt types. Strategy:

- Focus on higher-interest debt first

- Consider bi-weekly payments instead of monthly

- Round up payments to accelerate equity building

- Avoid refinancing that restarts your loan term (unless rate difference is substantial)

For most people, aggressive mortgage payoff makes sense only after other debt is eliminated.

Mental Game: Psychology of Successful Debt Elimination

The math of debt repayment is simple. The psychology is where most people struggle.

Changing Your Relationship With Debt

Successful debt slayers share these psychological traits:

- They see debt as a temporary state, not an identity

- They celebrate progress milestones (every $1,000 paid, etc.)

- They find free or low-cost substitutes for previous spending habits

- They’ve connected their debt payoff to concrete future goals

Try this: Write a “Debt-Free Vision” describing your first day without payments. How will you feel? What will you do with the freed-up cash flow? Keep this visible during tough moments.

Creating Accountability That Works

Your environment shapes your success. Build these accountability structures:

- A monthly financial date with yourself or your partner

- A visual progress tracker (debt thermometer on the fridge works wonders)

- A strategic accountability partner who asks about your progress

- Automated payments that happen before you can reconsider

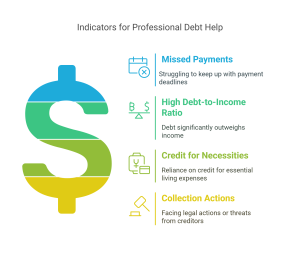

When to Consider Professional Help

DIY debt repayment isn’t always the answer. Consider professional guidance if:

- You’re missing payments despite your best efforts

- Your debt-to-income ratio exceeds 40%

- You’re using credit for basic necessities

- You’re facing collection actions or lawsuits

Financial counselors and nonprofit debt consolidation services can provide structured help when needed.

Budget Tactics for Different Income Situations

Your approach needs to match your financial reality.

Irregular Income: Taming the Cash Flow Roller Coaster

Freelancers, commission-based workers, and seasonal employees need modified approaches:

- Build a larger emergency fund (3 months minimum)

- Base your repayment plan on your minimum reliable monthly income

- Use “extra” months as debt acceleration opportunities

- Create a “floor” budget (bare essentials) and a “ceiling” budget (when income is strong)

The debt snowball can be particularly effective here, as completing smaller debts reduces your monthly obligation floor, creating more flexibility during lean periods.

Low-Income Strategies: Making Progress With Limited Resources

When every dollar is already allocated, try these approaches:

- Focus on increasing income (side hustles, job training, asking for raises)

- Target one small debt completely before moving on

- Look into hardship programs with creditors

- Consider legitimate nonprofit credit counseling

Even small victories – like paying off a $500 medical bill – create financial breathing room that can be leveraged into bigger wins.

The Final Word: Consistency Beats Perfection

The perfect debt repayment strategy executed inconsistently will lose to a decent strategy followed faithfully. Find the approach that works with your psychology and financial situation, then stick with it.

Remember: debt didn’t accumulate overnight, and it won’t disappear overnight. But with the right budgeting tactic and consistent effort, you’ll reach that debt-free finish line – probably sooner than you think.

What’s your biggest debt payoff challenge? Drop a comment below, and let’s tackle it together.

Take control of your finances with powerful debt strategies at Wealthopedia – your go-to guide for financial freedom!