{kind=link}

Key Takeaways

- Medical expenses are the leading cause of bankruptcies in America, affecting even those with insurance due to high deductibles and out-of-network costs.

- Job loss creates financial vulnerability through immediate income reduction while fixed expenses continue, quickly depleting savings and forcing reliance on credit.

- Excessive debt, especially high-interest credit card balances, becomes unmanageable when minimum payments barely cover interest and leave no financial buffer.

- Before considering bankruptcy, explore alternatives like credit counseling, debt settlement, consolidation, or direct creditor negotiation.

- Understanding the difference between Chapter 7 (asset liquidation) and Chapter 13 (payment restructuring) bankruptcy is essential for making informed financial decisions.

When financial troubles strike, they rarely come with a warning. One day you’re managing your bills, and the next, you’re drowning in debt that seems impossible to escape. If you’re feeling overwhelmed by mounting expenses and diminishing options, you’re not alone. Thousands of Americans find themselves considering bankruptcy each year—a difficult decision that comes with significant consequences but can also provide a fresh start.

The Reality Behind Financial Breaking Points

For many Americans, bankruptcy isn’t the result of reckless spending or financial irresponsibility. Instead, it often stems from unexpected life events that quickly spiral beyond control. Understanding the common causes can help you recognize warning signs and potentially take preventive measures before reaching the point of no return.

The Top 3 Causes of Bankruptcy in the United States

1. Medical Expenses: The Silent Financial Killer

It happens in an instant—a sudden illness, an unexpected diagnosis, or an emergency hospitalization. Even with health insurance, the costs can be staggering. Deductibles, co-pays, and out-of-network charges add up quickly, creating a mountain of debt that can seem insurmountable.

According to a study by the American Journal of Public Health, medical issues contribute to more than 60% of personal bankruptcy filings in the United States. What makes medical debt particularly devastating is its unpredictable nature—few people budget for a health emergency that could cost tens or even hundreds of thousands of dollars.

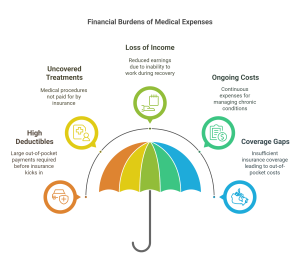

Why medical expenses lead to bankruptcy:

- High deductibles and co-pays that must be paid out-of-pocket

- Treatments not covered by insurance

- Loss of income during recovery periods

- Ongoing costs for chronic conditions

- Gaps in coverage or being underinsured

If you’re facing overwhelming medical bills, bankruptcy might seem like the only option. However, before filing, consider negotiating with healthcare providers—many offer financial assistance programs or payment plans that could make your debt manageable without taking the bankruptcy route.

2. Job Loss or Unemployment: When Your Income Disappears

The second most common cause of bankruptcy is job loss or significant reduction in income. When your primary source of financial stability vanishes, the effects can be devastating, especially if you’re living paycheck to paycheck like many Americans.

Job loss doesn’t just impact your ability to pay current bills—it can quickly drain whatever savings you have and force you to rely on credit cards or loans to cover basic necessities. This creates a dangerous cycle of debt that becomes increasingly difficult to escape.

How job loss leads to financial disaster:

- Immediate loss of income without adequate emergency savings

- Continuation of fixed expenses (mortgage/rent, car payments, utilities)

- Potential loss of health insurance, adding to vulnerability

- Psychological stressleadsg to poor financial decision-making

- Extended periods of unemployment deplete all financial resources

If you’ve recently lost your job, filing for bankruptcy shouldn’t be your first response. Unemployment benefits, severance packages, and temporary assistance programs might help bridge the gap while you search for new employment. Additionally, many creditors offer hardship programs for those experiencing temporary financial difficulties.

3. Excessive Debt: When the Minimum Payment Isn’t Enough

Credit cards, mortgages, auto loans, student loans—debt is a fact of life for most Americans. But when debt payments consume too much of your monthly income, any financial setback can trigger a crisis.

High-interest debt, particularly credit card debt, can quickly spiral out of control. Making only minimum payments means you’re barely covering the interest, leaving the principal amount largely untouched. This creates a situation where you might be faithfully making payments for years while barely reducing what you owe.

How excessive debt becomes unmanageable:

- High interest rates that keep balances growing despite payments

- Multiple debt sources create overwhelming monthly obligations

- Debt-to-income ratio that leaves no room for emergencies

- Predatory lending practices with hidden fees and penalties

- Underwater mortgages, where you owe more than your home is worth

Chapter 7 vs. Chapter 13: Understanding Your Options

If you’re considering bankruptcy, it’s crucial to understand the difference between the two main types available to individuals:

| Feature | Chapter 7 Bankruptcy | Chapter 13 Bankruptcy |

| Process | Liquidation of non-exempt assets to pay creditors | Reorganization of debts into a 3-5 year repayment plan |

| Timeline | Typically completed in 3-6 months | Lasts 3-5 years |

| Credit Impact | Stays on credit report for 10 years | Stays on credit report for 7 years |

| Asset Protection | Some assets may be liquidated | Keep most assets if you maintain payments |

| Best For | Those with limited income and few assets | Those with regular income who want to keep their property |

| Debt Discharge | Most unsecured debtsare completely discharged | Partial repayment of debts based on income |

Warning Signs You Might Be Heading Toward Bankruptcy

Recognizing the early warning signs of financial distress can help you take corrective action before bankruptcy becomes your only option:

- You’re regularly using credit cards for basic necessities like groceries or utilities

- You’re only able to make minimum payments on your debts

- You’re receiving frequent calls from debt collectors

- You’re considering payday loans or cash advances to cover regular expenses

- You’re unsure of how much you actually owe in total

- You’ve been denied new credit or loans

- You’re dipping into retirement savings to pay current bills

Alternatives to Consider Before Filing for Bankruptcy

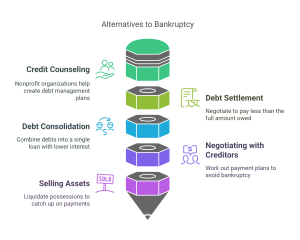

While bankruptcy provides legal protection and a fresh start, it’s not without significant consequences. Before filing, consider these alternatives:

- Credit counseling: Nonprofit organizations can help you create a debt management plan and negotiate with creditors

- Debt settlement: Negotiate with creditors to pay less than the full amount owed

- Debt consolidation: Combine multiple debts into a single loan with a lower interest rate

- Negotiating with creditors directly: Many creditors would rather work out a payment plan than get nothing through bankruptcy

- Selling assets: Liquidating non-essential possessions might help you catch up on critical payments

Protecting Your Financial Future After Hardship

Whether you’ve experienced medical emergencies, job loss, or overwhelming debt, rebuilding your financial health is possible. Here are some steps to consider:

- Build a 3–6 month emergency fund

- Get adequate health insurance

- Limit high-interest debt exposure

- Diversify income sources

- Maintain a flexible, up-to-date budget

- Learn from credit rebuilding resources

Final Thoughts: There Is Hope After Financial Hardship

Financial crises happen to good people with good intentions. If you’re facing overwhelming debt due to medical expenses, job loss, or excessive debt, remember that bankruptcy laws exist to provide a second chance. While the process isn’t easy, it can offer relief from crushing debt and the opportunity to rebuild your financial life.

Before making any decisions, consult with a qualified bankruptcy attorney who can evaluate your specific situation and help you understand all your options. Many offer free initial consultations, allowing you to get professional advice without further straining your finances.

Have you experienced financial hardship due to medical bills, job loss, or overwhelming debt? Share your story in the comments below—your experience might help someone else facing similar challenges.

Take control of your financial future today with trusted advice from Wealthopedia—your partner in navigating debt, credit, and recovery.