{kind=link}

Are you juggling multiple credit card payments each month, watching interest pile up faster than you can pay it down? If you’ve ever stared at a stack of bills wondering how you got here—and more importantly, how to get out—you’re not alone. Credit card debt consolidation might be the lifeline you’ve been searching for.

What Is Credit Card Debt Consolidation and Why Consider It?

At its core, credit card debt consolidation is a strategic financial move that combines multiple credit card balances into a single loan. Instead of making several payments to different creditors each month (often at sky-high interest rates), you make one payment, typically at a lower interest rate.

For many Americans, this simplification isn’t just convenient—it’s necessary for financial survival. According to recent statistics, the average U.S. household carrying credit card debt owes approximately $16,000 across multiple accounts.

“I was drowning in payments to five different cards with interest rates ranging from 18% to 26%. After consolidating, I have one payment at 9% interest. The relief is incredible.” — Sarah T., Chicago.

How Credit Card Debt Consolidation Works

The process is straightforward, though your specific path depends on your financial situation:

- Assess your debt situation – Gather all credit card statements and note balances, interest rates, and minimum payments

- Research consolidation options – Explore personal loans, balance transfer cards, or home equity options

- Apply for your chosen consolidation method

- Use the new funding to pay off existing credit card balances

- Make regular payments on your new consolidated loan

The key is finding a consolidation option with better terms than your current credit cards, which leads us to explore available options.

Consolidation Options: Finding Your Best Path Forward

Personal Loans for Debt Consolidation

Personal loans are among the most common tools for credit card consolidation. These unsecured loans typically offer fixed interest rates and predictable monthly payments over a set period (usually 2-5 years).

Pros:

- Fixed interest rates (typically lower than credit cards)

- Clear payoff date

- No collateral required

- Predictable monthly payments

Cons:

- May require good credit for the best rates

- Potential origination fees

- Higher rates than secured loans

Balance Transfer Credit Cards

If you have good credit, a balance transfer card with a low or 0% introductory APR can be an excellent short-term solution.

Pros:

- Potential for 0% interest during promotional period (typically 12-21 months)

- Simple application process

- No collateral required

Cons:

- Balance transfer fees (typically 3-5% of the transferred amount)

- High interest rates after the promotional period ends

- Requires disciplined repayment during the promotional period

- May not have high enough limits to consolidate all debt

Home Equity Loans or Lines of Credit

For homeowners with equity, these options offer some of the lowest interest rates available.

Pros:

- Lowest interest rates among consolidation options

- Potential tax-deductibility of interest

- Longer repayment terms are available

Cons:

- Your home serves as collateral

- Closing costs and fees

- Longer application process

Debt Management Plans

Working with a nonprofit credit counseling agency, you can establish a debt management plan where the agency negotiates with creditors on your behalf.

Pros:

- Professional guidance throughout the process

- Potentially reduced interest rates without requiring excellent credit

- Single monthly payment to the counseling agency

Cons:

- It may require closing credit accounts

- Monthly administration fees

- Typically, it takes 3-5 years to complete

Is Credit Card Debt Consolidation Right for You?

Credit card consolidation isn’t one-size-fits-all. Consider these factors when determining if it’s appropriate for your situation:

| Factor | Signs Consolidation May Help | Signs to Consider Other Options |

| Debt Amount | $5,000+ in credit card debt | Very small or overwhelming debt |

| Credit Score | 650+ for best options | Below 580 may limit options |

| Income | Stable income sufficient to cover payments | Unstable income or already stretched too thin |

| Spending Habits | Has addressed spending issues | Still actively accruing debt |

| Interest Rates | Currently paying high rates (15%+) | Already have favorable rates |

How Consolidation Affects Your Credit Score

Many people worry about the impact of debt consolidation on their credit scores. The truth is, consolidation can ultimately help your score if managed properly:

Short-term effects: You may see a slight dip in your score due to:

- New credit inquiries

- Opening a new account

- Changes to credit utilization

Long-term benefits:

- Lower credit utilization ratio as balances decrease

- More on-time payments (easier with one payment vs. many)

- Eventually, debt reduction and improved debt-to-income ratio

According to the Federal Reserve Bank of New York, consumers who consolidated credit card debt saw an average credit score improvement of 10-30 points within six months after consolidation, assuming consistent payments were made.

Step-by-Step Guide to Successful Debt Consolidation

1. Get Organized

Before applying for any consolidation option, gather:

- Current statements for all credit cards

- Your credit score and report

- Income documentation

- Budget breakdown showing you can afford the new payment

2. Compare Options

Research various consolidation offers, paying attention to:

- Interest rates (both introductory and long-term)

- Fees (origination, balance transfer, closing costs)

- Repayment terms

- Monthly payment amounts

- Total cost over the life of the loan

3. Apply Strategically

- Apply for your top choice first

- Wait to close old accounts until your new account is approved and funded

- Read all terms carefully before agreeing

4. Set Up for Success

- Establish automatic payments for your new loan

- Create a budget that prevents accumulating new debt

- Consider seeking credit counseling for ongoing support

5. Monitor and Adjust

- Track your progress regularly

- Consider making extra payments when possible

- Avoid using newly paid-off credit cards

Common Pitfalls to Avoid

Even with the best intentions, debt consolidation can go wrong. Watch out for these common mistakes:

- Continuing to use credit cards after consolidation This is the number one reason consolidation fails. Once consolidated, resist the temptation to rack up new balances.

- Choosing the wrong consolidation method: Don’t be blinded by a low introductory rate if the long-term costs are high.

- Not addressing spending habits Consolidation treats the symptom, not the cause. Without lifestyle changes, you’ll likely end up back in debt.

- Working with predatory lenders Some “debt relief” companies charge excessive fees and may damage your credit further. Always research lenders through the Consumer Financial Protection Bureau.

- Closing all old credit accounts This can hurt your credit utilization ratio and credit history length. Consider keeping older accounts open with zero balances.

When to Consider Alternatives to Debt Consolidation

While consolidation works for many, it’s not always the best solution. Consider these alternatives if:

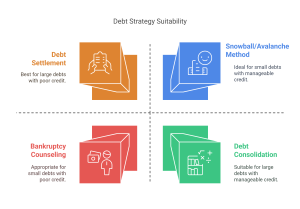

- Your debt is too small: For debt under $5,000, a dedicated debt payoff strategy like the snowball or avalanche method might be more efficient.

- Your credit won’t qualify you: Poor credit might mean consolidation offers won’t save you money.

- You’re overwhelmed by the total amount: If consolidation payments would still be unmanageable, debt settlement or bankruptcy counseling might be necessary.

- The debt is already in collections: Different strategies apply for debts that have progressed to collections

Expert Advice: Maintain Your Financial Freedom

Financial counselors emphasize that consolidation is just one step in your financial journey. To maintain your progress:

- Build an emergency fund to avoid relying on credit cards for unexpected expenses

- Track your spending using budgeting apps or spreadsheets

- Consider the “cash envelope” system for categories where you tend to overspend

- Set regular financial check-ins with yourself or your partner

- Celebrate milestones in your debt payoff journey

Taking the First Step

If credit card debt consolidation sounds right for your situation, begin by:

- Checking your credit score through a free service like Credit Karma

- Researching lenders through marketplaces like Bankrate or NerdWallet

- Contacting a nonprofit credit counseling agency like the National Foundation for Credit Counseling

Remember that taking control of your debt isn’t just about the numbers—it’s about creating peace of mind and building a secure financial future.

Your Questions Answered: Credit Card Debt Consolidation FAQs

Q: Will consolidating my credit card debt hurt my credit score? A: Initially, you might see a small dip due to credit inquiries and new accounts. However, over time, your score will likely improve as you make consistent payments and reduce your overall debt.

Q: How much debt is too much to consolidate? A: There’s no one-size-fits-all answer, but consolidation works best when you can secure a loan with a monthly payment you can consistently afford. Most experts recommend that your debt-to-income ratio stay below 40% for consolidation to be effective.

Q: Can I consolidate other types of debt with my credit cards? A: Yes, many consolidation loans allow you to include other unsecured debts like medical bills or personal loans. However, including secured debts like auto loans usually isn’t recommended.

Q: What if I’m denied a consolidation loan? A: If rejected, request details about why. Work on improving those factors (usually credit score or income verification), consider a co-signer, or explore debt management plans through credit counseling agencies.

Q: Should I close my credit cards after consolidating the balances? A: Generally, it’s better to keep accounts open to maintain your credit history length and available credit (which helps your utilization ratio). However, if keeping them open tempts you to spend, consider closing newer cards and keeping older ones.

Ready to Take Control of Your Financial Future?

Credit card debt consolidation isn’t magic—it’s a strategic tool that, when used wisely, can transform financial stress into confidence. By combining multiple high-interest debts into one manageable payment, you’re not just simplifying your finances; you’re taking a critical step toward financial freedom.

Remember, the most successful debt consolidation stories begin with an honest assessment and end with changed financial habits. You don’t have to figure it all out alone—consider working with a credit counselor who can provide personalized guidance for your situation.

What step will you take today toward breaking free from credit card debt? Share your thoughts or questions in the comments below!

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Please consult with a qualified financial professional before making significant financial decisions.